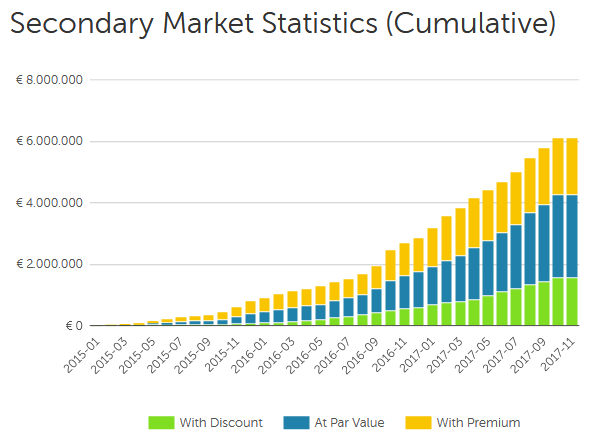

Latvian p2p lending marketplace Mintos announced today that all transactions on the secondary market are now free.

Exciting news! Starting from today, November 1, 2017, we have removed the 1% fee for selling loans on the secondary market of the Mintos marketplace. This means from now on, there are absolutely no fees for investing through Mintos.

“A secondary market with no fee will greatly benefit our investors. We expect the secondary market to become even more liquid now. This is especially good news for investors who want to pursue a long-term investment strategy and invest in loans with longer maturity. In the case investors will need the liquidity before the loan matures, they will be able to sell their investment with no extra fee added,†says Martins Sulte, CEO and co-founder of Mintos.

The monthly volume of traded loans on the secondary market is about 300,000 Euro per month.

Baltic Bondora stopped charging fees on its secondary market in November 2015.

With the majority of my p2p lending investments I hold the loans I invest in to maturity. Observing the market over the years I have observed patterns on the secondary markets that can be used to actively trade loan parts with the hope to increase achieved yields and I sometimes tried these.

I never specialized in this, so I never used fully automated bots, but did in some cases use some automation (Selenium or third party browser plug-ins). This article is not meant to be a how-to guide giving concrete instructions, that readers could just follow, but rather a list of things to consider and look for, should investors want to start testing strategies on the secondary markets themselves.

This article does not name or link any specific platforms, as I believe the same patterns and chances could evolve on new p2p lending marketplaces, and can be used there, you just need to look for them. Nevertheless all of the examples are real examples observed at the past by me.

Required market environment

The marketplace needs to have a secondary market that allows investors to buy and sell loans parts at premiums and discounts. Ideally without charging any transaction fees, but some strategies can absorb moderate fees. Furthermore it is advantageous if specific individual loans can be bought or sold rather than just random from the market or the investor’s portfolio.

The effect of premiums on yield

One central piece to understanding why trading (or flipping) strategies can be highly attractive is the effect of even small premiums pocketed on the portfolio yield. Take an investor that invests into a 100 (whatever currency) loan part and sells that part for 100.40 after holding it for 5 days. That is only a 0.4% premium, but the annualized yield is 33.8%. There is a big IF to that annualized yield number – it is only meaningful if the investor can seamlessly reinvest all his money in similar trades without any interruptions. So cash drag (effects of not invested cash) are very important.

The psychology

One would think that investors would always use rationale when investing into loans. However, I feel that a significant number of investors show one of these behaviors and the question an investor with a trading strategy should pose himself, is whether he can use that to his own advantage:

Scarcity If there is little left / available of a loan, investors fear of missing out

Unusual collector’s passion P2P Lending investors are told everywhere that diversification is vital (I tell them too). But especially on platforms with few loans, it seems that some investors strive to have a COMPLETE collection of loans in their portfolio and in pursuing that aim pay higher than average prices to acquire loans they ‘miss’ in their portfolio

Herd behavior Happens for example when investor (over)react scared by a news bit on a loan. In p2p lending that mostly effects the selling side rather than buying

Investors overvalue the realization of small gains Many investors are very happy to sell at small premiums –it just gives them a sense a positive achievement, not realizing that the market conditions for this specific loan part would have allowed selling at a higher premium

Blended by high numbers High nominal interest rates, and high YTM (yield to maturity) figures displayed by the platform overly attract investors

Two main strategy approaches

Investors can A) Invest on the primary market and then sell the loan later on the secondary market or B) Buy loan parts on the secondary market which they deem underpriced and then sell at a higher price. Be it buying at discount and selling at a lower discount, or already buying at premium and selling at an even higher premium.

While yields achievable in strategy B might be higher in percentage, this strategy is much harder to execute, as the competition will most likely use automated bots. Also the total market size for attractive loans will limit the scalability. I never tried strategy B on a larger scale myself. For example I was never found of buying already defaulted loans at a huge discount. Nevertheless I know of some investors that fare quite well buying defaulted loans and selling them at a lower discount, pocketing any payments and recovery that occur while they hold them as an additional bonus.

Following I will concentrate on strategy A) Invest on the primary market and then sell the loan later on the secondary market – as I have used this myself on several platforms over time.

One important point, is that market conditions change, usually good opportunities will stop working after a few months or weeks either because too many investors try to use them, or more general  the demand/supply ratio changes or the marketplace itself changes the rules how the market functions.

First an investor will want to look how loan information is presented on the primary and secondary market. Especially what sorting and filtering mechanisms there are on the secondary market. It is highly desirable that the loans the investor wants to sell later, will be listed on top of the list of all loans on the secondary market with either the defaulted sorting, or with an obvious choice of filtering (e.g. sort by descending YTM)

Understand the allocation mechanism on the primary market. How does the autoinvest feature work exactly? If there is no autoinvest, then are there chances to heighten the probability of investing in attractive new loans? Either through automation, or just because new loans are released at specific times?

When is interest paid? Does it accrue for each of the day held, or does the investor holding the loan at the date of the interest payment gets full interest credited. This is important, because if in the example at the start of the article the investor not only makes a 0.40 capital gain but also collects interest for the 5 days he held the part, it will have a huge impact on yield

Usually for this strategy longer duration loans are more attractive. This is simply because they will allow higher premiums without making the YTM value unattractive for the potential buyer

Usually smaller loans are more attractive. As there will be less supply it will be more liquid on the secondary market and more sought (see collector’s passion). No rule without exception. On one platform the biggest loans were the most attractive to be invested in on the primary market for the trading strategy. Why? Because this platform used dutch autions to set the interest rate and the bigger the loan the less the interest rate would go down. And of course loans with higher interest rates could later be sold at higher premiums

Usually the time span a trading investor wants to hold on to a loan part, will be as short as possible (days). However there might be patterns observed where it could be desirable to hold for longer time spans. For example if on a marketplace there are repeated alternations between lots of new loans and time without any new loan, it might make sense to hold the loan parts till there are no loans available on the primary market and only then offer them on the secondary market

Strategies that allow to hold parts only at a time when the status of a loan cannot change can be attractive. For example there was a time when it was possible to invest into very high interest, extremely high risk loans on the primary market of a specific platform and sell them at a premium BEFORE the first loan payment was due. Most parts sold within days, and the ones that did not sell at a premium, could be sold at par shortly before the date of the first loan repayment (this strategy worked due to a combination of factors: sorting by YTM, blended by high numbers (see above), and platform design – instant selling of loans offered at PAR).

So why is all this possible. Mostly due to market inefficiencies and lack of transparency and experience. The marketplaces are young, selecting and evaluating loan parts on the secondary market is not an easy task. And on many marketplaces investor demand outstrips loan supply . Usually the yields achievable with trading strategies go down as marketplaces grow (but the volume that can be used in these strategies might grow over time).

The most prominent question is, if an investor can scale strategies he uses to a level that is worth the time invested and the inherent risks.

The market situation on UK property marketplaces for bridge loans with high interest rates has turned drastically in the past 2 months. For a long time before there has usually been much more investor demand than could be soaked up by loan demand. That the situation has changed is most visible on the loans on offer (mostly through the secondary markets). There is currently nearly 8 million GBP on offer on Lendy (that was close to nil 8 weeks ago). At Moneything there is 2 million GBP on offer and at Fundingsecure 0.6 million GBP. Collateral recently raised the interest rate for new loans from 12 to 14%.

So what is causing this change? I will look at possible causes and measures the marketplaces could take to react.

Have property prices peaked? Building activity and property prices are influenced by the economy. This Guardian article says UK house prices fell three month in a row. Should investors think, the economic climate is cooling down, they might be more cautious as loans to property developers would be affected in a downturn.

Defaults are rising on Lendy Loans that are more than 180 days overdue are categorized as default loans on Lendy. There are now 19 loans in default, with the total loan amount in these loans adding up to 23 million GBP. While this does not mean that money will be lost – the loans are secured by the property, it makes investors cautious and hesitant, asking more questions about valuations and collection procedures.

Lenders might fear that the assets become increasingly illiquid Part of the attraction of Lendy and Moneything in the past (aside from the high interest rate) came from the fact that loans could be sold very fast, usually within hours for most loans that were not overdue. That has changed on Lendy and might be currently changing on Moneything. However with the queues for sales building up on Lendy it is too easy to just look at the nearly 8 million GBP on offer and deduct that it takes very long to sell loans. Not all loans are equally liquid. I sold 400 GBP of DFL025 recently. Despite over 35,000 GBP in the queue before me, my part sold within 3 days. A major factor with the longer selling times is that on Lendy, investors forego interest while the loan part is on sale. On Moneything it continues to accrue interest while on sale.

UK investors are increasing their stake in tax sheltered IFISA products That is my favourite explanation. The shift in the above markets 2 months ago coincides with the launch of many IFISA offers on other UK marketplaces. Lendy, Monything and Collateral currently do not offer IFISAs. Check the database for best IFISA rates of other marketplaces. Fundingsecure has an IFISA. I am not currently investing on Fundingsecure, therefore I am not as closely monitoring the market developments on Fundingsecure as on Lendy or Moneything. But it seems that investor demand on Fundingsecure has not changed as much as on Lendy or Moneything. It is obvious that UK investors will prefer to invest in IFISA offers, at least until their yearly allowance of 20,000 GBP is reached.

Brexit and pound uncertainty pause international investors All of the above platforms are open for international investors. I currently run a survey among German speaking investors on my German p2p lending forum. 31% precent of respondents have already invested on UK marketplaces. But 5% want to reduce their level of investment because of the uncertainty of the pound development and for this reason 20% will not consider to start on UK marketplaces.

So what could marketplaces do and what measures are they already taking?

Attract more investors, increase marketing spend I believe this is already happening. Lendy revamped the referral program as of June 1st and Collateral announced it will launch one soon. Lendy will sponsor the ‘Lendy Cowes week’ sailing regatta. I have doubts this will be cost effective, but its hard to tell from the outside without access to hard figures. I know of other p2p lending platforms that sponsored golf events in the hope of targeting and attracting the right audience and discontinued that (for reasons unknown to me).

Launch an IFISA Actually I think this would most profoundly change the situation for Lendy. However for that Lendy first needs to get full FCA approval. Moneything has recently said it has put an IFISA higher on the priority list, but it is still not imminent but planned for later this year.

Find ‘different’ sources of capital This could be institutional money. Or a differently structed offer like the Lendy bond. But it is to early to tell how the Lendy bond is taken up.

Raise interest rates Collateral has taken this step. And Moneything offered 1 percent more on a very large loan. I don’t think Lendy will take this route as it recently moved from 12% interest for all loans to a broader range of 7 to 12% interest rates.

Change the model of the secondary market Lendy and Moneything currently have secondary operating at par value. The investor community seems split. While some applaud the simplicity and ease of use of this model, others argue to allow discounts (and possibly premiums). One argument for discounts and premiums is that it might better match demand and supply. Counterarguments are that p2p lending is not a high volume market and variable pricing would not be suitable and that premiums will attract traders. Also some feel that seeing discounts will furthermore undermine trust and deter new investors from signing up.

Show recovery results and better communication and transparency of collection efforts Obviously full recovery on defaults would be a most effective measure to increase confidence and trust of investors. However this will take time and I don’t think haste would do the results good. Therefore the only thing Lendy could do short-term is communicate more and in more detail.

What is your opinion, dear reader?

P.S.: On the continent at Estateguru with its 10-12.5% interest property loans there is no change of market conditions. Investor demand continues to outstrip loan supply.

Finbee is a small p2p lending marketplace for consumer loans in Lithuania (see earlier coverage). I have been using it as an investor for a little over a year now. My strategy on Finbee is different than on other marketplaces. I invest loans mainly with the purpose of trading in mind, that means on Finbee I don’t plan to hold the loan parts to maturity

Finbee secondary market basics

Loans can be offered at a discount, par or premium

Seller pays 1% fee upon successful transaction

Only loans with at least one repayment can be offered. This means I cannot sell loans directly after acquiring them on the primary market (no flipping). I have to hold each loan for at least 30 days.

Late loans and loans in arrears can be offered. Loans that are 60+ days overdue cannot be listed for sale.

Maximum listing duration is 20 days; thereafter seller can relist

Buyers can buy instantly at ‘buy now’ price or make a bid, hoping that no other buyer overbids them in the remaining listing duration (or pays buy now price)

Finbee parameter UI for selling loan parts on secondary market

How I select loans on the primary market

I mostly invest in ‘D’ loans (that is the most risky rating) with long loan durations (>36 months) and high interest rates. The average interest rate in my portfolio is 32%, the maximum 35%. My reasoning for this choice is that these loans allow high markups and still offer an attractive buyer yield (XIRR value). The longer the remaining loan term is, the lower will be the impact of the markup on the calculated yield for the buyer. I mostly buy 40 Euro loan parts, sometimes multiple in the same loan. I selected this amount because larger parts might not appeal to as many buyers, as some investors only invest small amounts.

Why I select different values for the reserve price and the buy now price

Since the XIRR that is displayed to the buyer depends solely on the buynow markup, it would seem logical to set same markup prices for the reserve price and the buy now price, doesn’t it. If in the example above I would set the price to 8.4% for both than I would get 8.4% markup if the sale takes place. With 8% and 8.4% values, I most likely get only 8% (at these markups there are very rarely multiple bidders competing). So why would I forego 0.4% gain? The reason is simple. With buynow the sale takes place instantly. But if I get the buyer to make a bid, the transaction takes place at the end of the listing duration, and all interest accrued during this duration is mine. Note that the buyer can NOT back out. He is commited and the sale will take place if he made a bid. In the above case the 20 days on a 39 Euro loan part at 32% mean I earn an extra 0,68 Euro (39€*32%/365 days*20 days) interest. So in effect if someone bid 8% on this loan my gain is 8%+1.74% accrued interest = 9.74% gain (which is much better than the 8.4% buy now). Of course I have to deduct the 1% seller fee.

BTW, I wondered how Finbee manages the sales with the accrued interest. When the buyer makes the bid, as said he cannot back out. But it is not clear if he will win (another buyer could overbid him) or how much interest will accrue for I as the seller have the right to accept the bid anytime early (which would only make sense if my cash is zero and I urgently want to bid on a new loan with a much better interest rate). But Finbee can’t wait until the time of sale because at that time, there could possibly be not sufficient cash in the buyer’s account. I couldn’t figure it out, therefore I asked Finbee. The answer is Finbee reserves the maximum possible price (principal+premium+maximum possible accrued interest) at time of the bid in the buyer account. Once the sale takes place, if the actual accrued interest is lower than the reserved maximum accrued interest, part of the amount is freed up. Continue reading →

P2P lending marketplace Prosper today informed investors via email, that it will close down the secondary market, effective October 27th. Prosper does not operate the secondary market itself, but uses FolioFn, operated and maintained by FOLIOfn Investments, Inc., a registered broker-dealer.

The announcement email reads:

A Message from Prosper and Folio Investing

Dear …,

We are writing to let you know that as of October 27, 2016, Prosper will no longer offer the Folio Investing Note Trader platform, the secondary market for Prosper Notes. Prosper has found over time that very few investors are using the secondary market and, as such, has made the decision to no longer offer this service. We apologize for any inconvenience that this causes. Prosper remains committed to its retail investor clients and to providing them a great experience.

Here’s what this means for you: The secondary market trading service will be available as normal until end of day (5:30 pm PST) October 19, 2016. After that time, any new orders to list Notes for sale will not have sufficient time to be completed and processed before the site becomes unavailable to users at the end of day (5:30 pm PST) on October 27, 2016.

Once the secondary market trading service is terminated, you will not be able to sell Notes that you own, and you will need to hold them to maturity.

If you have questions about your Notes or the wind-down of the Folio Investing Note Trader platform, please contact Prosper customer service at 877-611-8797.

Thank you.

Prosper and Folio Investing

Prosper has not disclosed usage numbers of the secondary market in the past, but volume traded is perceived to be low and this is also stated in the email. One speculation is that Prosper decided to close the secondary market to cut costs.

My feeling is that this will deliver a blow to the attractiveness of the Prosper marketplace for retail investors. Even if many investors have choosen not to use the marketplace (which several report does not have a very good user interface) the fact that there is a marketplace delivered some assurance that they could exit at least a larger portion of their portfolios should the need for liquidity arise. Also a one month notice seems to me rather short, given that loans can run up to 60 months and with the changed perception the prices could sink (lower markups, higher discounts) in the remaining month of trading as the number of investors wishing to use this last chance to sell will rise in my view, while the number of investors buying will at best stay stable. Continue reading →

‘Easy access’ investment will be available in a RateSetter ISA

RateSetter has improved customers’ access to their money by removing all early exit fees from its monthly investment market. This means that RateSetter’s 33,000 investors can now benefit from great rates of return combined with easy access to their money.

RateSetter’s monthly market has proven very popular with investors, delivering an average rate of 3.1% p.a. over the last five years. The latest rate can be found here.

As with all marketplace lending, the speed of access to money is dependent on liquidity. RateSetter has managed market liquidity for over five years, the result being that no investor has ever had to wait to withdraw their money from RateSetter. Early withdrawal fees remain in place for RateSetter’s one year, three year and five year investments. More information can be found here. RateSetter is looking at options to simplify the way fees are calculated to provide greater certainty to investors.

The announcement comes less than two months before the launch date for the Innovative Finance ISA (IF ISA) on 6 April and follows the release of information on RateSetter’s forthcoming IF ISA over a week ago. RateSetter has confirmed that customers will be able to invest in any of its markets within an IF ISA wrapper, and thus can benefit from easy access investments with tax-free returns. Continue reading →