![]()

![]() For decades buying houses, refurbishing them and selling them at a higher price and moving on to the next property seemed like a popular sport to Brits. Many of them see properties as investments and with house prices mostly moving up lots of them aimed to finance a property while they were young and then build a portfolio. With limited supply of new land with planning permissions this strategy worked well most of the times in the past, except when the market overheated and a real estate bubble popped.

For decades buying houses, refurbishing them and selling them at a higher price and moving on to the next property seemed like a popular sport to Brits. Many of them see properties as investments and with house prices mostly moving up lots of them aimed to finance a property while they were young and then build a portfolio. With limited supply of new land with planning permissions this strategy worked well most of the times in the past, except when the market overheated and a real estate bubble popped.

There are downsides to this do-it-yourself approach:

- Concentration of risk in one or few properties: if they underperperformed for what ever reason, the yield was sub-average

- A lot of money, time and work required. The investor had to do everything itself as a landlord

- Selection of new properties usually limited to a small region the investor lives in

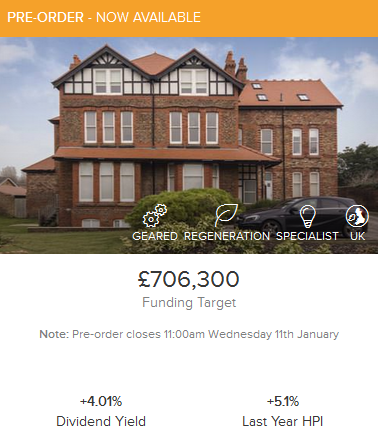

British platform Property Partner allows everyone to invest in British properties from a minimum of 50 GBP. Investors select a listing, invest into a SPV (special purpose vehicle company) that pools the investment in the property. The SPV collects rental income and pays dividends to investors monthly. A useful table of the past achieved rental income can be seen here. In the green marked cases the actual rents are higher than the original forecsts. Potentially investors can also gain, if the value of the property rises.

The time span of an investment is 5 years, however investors can try to sell their parts on the secondary market, which allows discounts and premiums any time.

The platform allows the investor to diversify across multiple properties easily. The fee is 2% for investment (in new listings or buying through the secondary market). For management, advertising and letting Property Partner charges 12.6% of gross rent.

So far Property Partner has funded 311 properties for 43.9 million GBP with 9.100 investors participating.

For new listing there is a pre-order period, where bids are collected. If the listing is oversubscribed then each investor is allocated a lower proportionate amount of shares.

For new listing there is a pre-order period, where bids are collected. If the listing is oversubscribed then each investor is allocated a lower proportionate amount of shares.

Each listing contains an investment case desctiption, property details, a floor plan, financials, a solicitor’s report and a surveyor’s report as well as the house price index (HPI) information for the area.

For the secondary market there is a ‘data view’ section which lists key indicators for the parts listed for sale.

Investors that do not want to pick listings can set up the auto-invest option which will automatically invest an amount the investor sets each month in 5 properties.

Investing from abroad

Property Partner allows foreigners (except for US residents) and corporations to invest. If you do not live in the UK but see the UK housing market as an investment opportunity Property Partner is a hassle free possibility to invest in british real estate. Non resident investors should consider using Transferwise or Currencyfair to avoid high bank fees and get a better currency exchange rate.

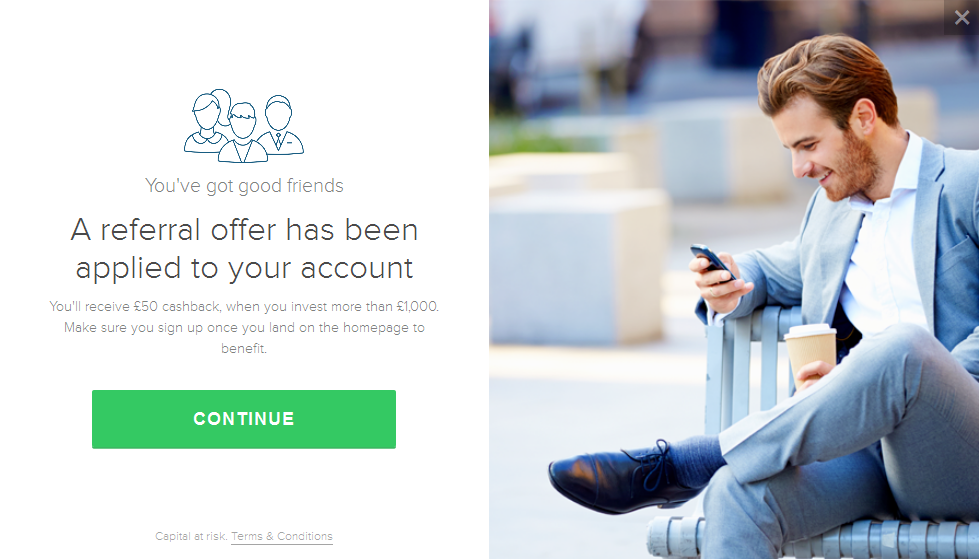

How to get 50 GBP cashback at sign-up

To get 50 GBP referral cashback, when you invest more than 1000 GBP sign up now via this link . To see available promotions by other platforms visit our cashback offer page.

Property Partner cashback confirmation at sign-up. To see it follow this link and sign up.

")