Infatuation with blogs, the rise of citizen newspapers (like Rue89) [FR], the rebirth of consumer associations (Que Choisir) [FR] or equally the expansion of BarCamps (BarCampBank was born in France) change deeply the relationship between French banks and their customers.

This new ecosystem gives more power to customers. The French Internet users have more technical solutions to run mortgage simulations or to compare the different offers on a loan.

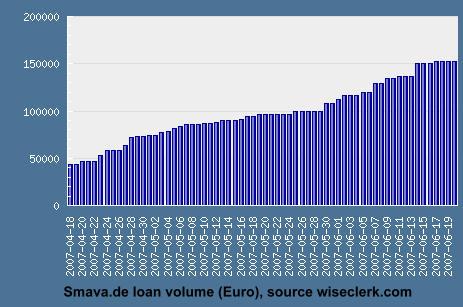

Outside of France, new online services have already appeared where online lenders and borrowers can meet. These cyberbanks or P2P Banks (peer-to-peer or people-to-people) grow their success on lower rates and quicker processes. Following Zopa in the UK and Prosper in the US, P2P Banks have expanded in Europe with Boober in the Netherlands, Smava in Germany.

The reason for this is quite simple: traditional banks give a credit only to people with an excellent solvency profile; cyberbanks on the contrary lend to borrowers with good, or even mediocre profiles. And the average default on repayment has been lower than the bank-industry, so far. How do they achieve this ? Emulating auction sites like eBay, the borrowers and lenders assign scores to each other. Thus each participant has a strong incentive to uphold his commitment in order to keep a good score and to continue being part of the system.

For the time being, the development of P2P financial services in France meets 4 main points of resistance:

1. Banking regulation

The "Code monétaire et financier" (General Principles of Bank Regulation) is straightforward: "anyone except a chartered bank can perform banking operations in a regular fashion".

Nevertheless, nothing prohibits lending from an individual to another individual. Private individuals can lend on a personal basis to relatives or friends. These friendly loans can for example take the shape of a "Tontine" (a Rotating Savings and Credit Association).

Conversely, a bank is entitled to perform an activity relating to credit between individuals. But it is difficult to foresee the context where a bank would desintermediate itself and forgo handsome commissions…

2. Fear of over-indebtedness

The State, consumer associations, and consumers themselves live in fear of over-indebtedness. If credit for real estate is well accepted, credit for consumption purposes is much less widespread.

It should be noted however that French people are generally much less in debt than other Europeans and their situation does not logically support this fear (only 40% of people under 35 use the advantage of a cash credit, against of 70% in the UK). Some observers even regret the low penetration of consumer credit in France on the ground that economic studies show that it has a positive impact on growth.

3. A credit rate market that is both regulated by the state AND ultra-competitive.

From a general standpoint, the French market is ultra-competitive and interest rates are generally lower (yes, believe it) than in other European countries (the mean rate for amortizable loans was at 6.54% during Q1 2007).

Nevertheless, interest rates compensating risks can not go over the usury rate limit, as defined [FR] by the State (for amortizable consumption loans: 8.93% effective rate for a sum over 1.524 euros). This usury rate is a strong impediment for banks that would like to lend to atypical borrowers: students with no banking history, independent workers or small entrepreneurs with irregular revenues.

Since they cannot lend at a higher interest rate, these banks are not ready to take those risks. According to a study from the French Senate, roughly 15% of the population fails to qualify for credit because of this regulation on the usury rate. Providing credit to this fringe of the population would be like going after the long tail of credit.

4. The absence of positive credit scoring

In France, only banks have access to a history of credit operations. The positive records (historic records of credit to be reimbursed by an individual) are illegal in France where only negative records (historical records on banking operation bans or payment incidents) can and must be used when according a credit. The latter are penalty records that can only be accessed by banks and those unfortunate enough to be referenced in these records!

It must also be considered that credit risks are idiosyncratic to each country (culturally and functionally different). It is then difficult for a foreign company to properly evaluate risk in the French context and offer a competitive – and profitable – product in a already over-served market. (Let's remember the failure of Egg in penetrating the French market).

Risks for the lenders under the current conditions are very significant and would justify a higher remuneration (impossible because of the regulation on usury rates), or that the new entrant company would use a statistical rating of credit risks (which would require either a commercial agreement with a French bank, or the development of a reputation scoring as yet unheard of in France).

Conclusion

Nevertheless, despite all these barriers, it is likely that such a service will come to life in France within the next 3 years (when the corresponding European directives have been written and agreed upon – e.g. the new SEPA regulation: Single Euro Payments Area); either introduced by national actors (existing banks or financial organizations); or by new entrants (possibly involving partnerships with banks).

Quite a conundrum, but an outcome bound to happen anyway !

Authors : Jean-Christophe Capelli [FR]; translation provided by Frederic Baud [EN]. (Jean-Christophe & Frederic are two of the BarCampBank [EN] co-founders).