In December 2013 I saw the pitch of a promising pre-launch UK p2p lending startup called Landbay pitching on the UK p2p equity platform Seedrs to the crowd. The pitch explained how they planned to do p2p lending secured by property in the UK. I liked the proposal and invested a small amount in Landbay shares.

Since then it has been very interesting journey. I watched how Landbay fared, saw them grow the marketplace substantially. There have been subsequent following rounds into which I invested again. Shares issued through Seedrs come with pre-emption rights, that means I am entitled (but not obliged) to invest in next rounds to avoid dilution of my share percentage.

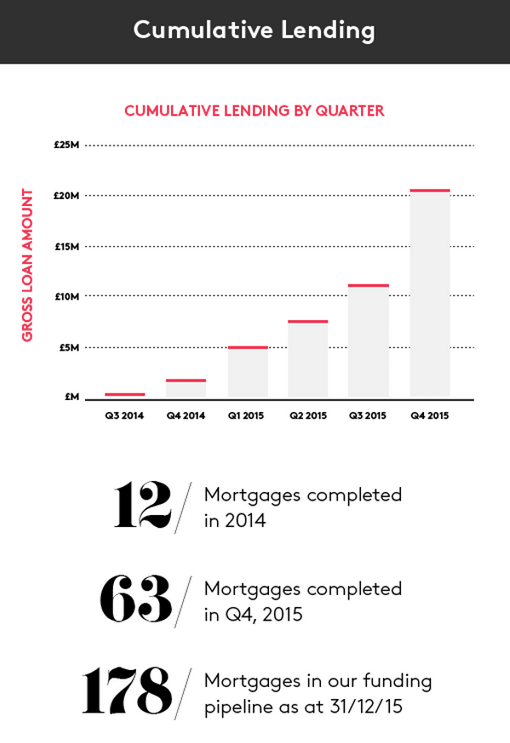

Currently Landbay is pitching to raise 1M GBP at a pre-money valuation of 10.3M GBP. You can see the current pitch here. The shares are priced at 85 GBP, that is the minimum investment amount (normally most Seedrs pitches come with a minimum investment of just 10 GBP). At the time of this writing the pitch is already filled 91%. Before it opened for public bidding recently, it was only accessible for existing shareholders like me to enable them to execute their pre-emption rights. I am not sure the pitch will allow overfunding.

Last week Landbay announced that they received an investment from Zoopla. Zoopla is a company that operates property sites uSwitch and Prime Location.  Zoopla announced full year results (ending September 20, 2015) showing a revenue increase of 34% as the top line number jumped to £107.6 million. Profit for the year increased 20% to £25.4 million.  The partnership with Landbay is designed to help scale their retail customer base as the P2P lender becomes a more established mortgage lender.While the precise amount of the investment into Landbay was not disclosed, Zoopla invested into a total of 4 companies and the total for that was 1M GBP. This deal will also trigger previous convertible rounds that Landbay did on Seedrs.

If you are interested in the pitch you don’t need to be a UK resident. Just sign up at Seedrs and follow the process. If you are outside of the UK, I recommend considering to use Transferwise or Currencyfair, when depositing money in order to reduce currency transfer fees significantly. If you are a UK resident, note that the pitch is EIS eligible.

This article is not an investment advice. Investing in startups bears significant risks, including total loss of investment.

CommuterClub delivers a new and innovative way to access public transport as a subscription service.

By bringing together a low cost loan with the existing annual ticket, CommuterClub can deliver the savings of an annual, in a far more convenient and attractive package as a monthly payment plan.

Our goal is to continue to bring new innovative products for commuters, delivering value for money and ease of use.

I really like the fact that your business model builds on long customer relationships. What do you do to achieve high customer satisfaction?

CommuterClub operates in a sector dominated by large slow moving monopolies who manage public transportation. Our proposition is to offer an alternative approach to commuters that begins with their needs. Our focus on a simple customer journey, great customer service and a simple product all deliver a fantastic outcome for consumers.

This is key in ensuring high customer satisfaction and providing a real alternative to the existing ticketing options.

The audience of this blog is highly interested in p2p lending. Can you please explain how your company ties into this industry and what role Ratesetter and potentially Zopa play for your financing?

CommuterClub works with RateSetter to fund all loans. As a business P2P was the key building block enabling us to deliver a low cost and flexible product to consumers, something that we would have found exceedingly difficult if we worked with incumbent banks.

We expect to continue to work with p2p going forward and to maintain our close relationship with RateSetter.

The pitch video

The timing of this round is a bit of a surprise to me since you indicated to shareholders recently ‘at our current trajectory we expect to be [able to] sustain growth from retained earnings’. Why did you decide to raise further capital now?

CommuterClub has made tremendous progress in diversifying the business expanding nationally in the UK, launching a B2B solution and also looking to cover other verticals like parking.

This expansion of our product set has also expanded our target market and we are now raising capital to fund our continued expansion and growth.

Name one fact that makes your pitch a better investment than any other pitch on Seedrs.

Real, proven traction backed by millions in loans and thousands of happy customers.

ING Bank partners with equity crowdfunding service Seedrs and reward based crowdfunding platform Kisskissbankbank to tackle the markets in Belgium and Luxembourg. Through this partnership, ambitious businesses will have a fast-track service for equity crowdfunding on Seedrs. The partnership will also raise the awareness of equity crowdfunding in the wider business community.

During consultations with businesses, ING Belgium representatives will assess which platform may be suitable and discuss how it works. Using the ING fast track procedure it only takes the entrepreneur a couple of clicks to submit an initial campaign enquiry for review. When Seedrs receives a project through this new route, it will be assessed within two days to determine if it’d be a good fit for Seedrs and equity crowdfunding. Continue reading →

This is a guest post by Dutch lawyer Coen Barneveld Binkhuysen (see full bio at the end of the article)

Crowdfunding is growing exponentially in the Netherlands. Although the Dutch market has not yet reached the astronomical levels of the United States and the United Kingdom, many people have heard about the phenomenon and are intrigued by this potential alternative investment opportunity. While the Dutch market speaks a lot about crowdfunding, it is less familiar with the term p2p-lending (it is commonly available though). As this article covers investments in loans, convertible subordinated loans and equity, I will use the general term crowdfunding instead of p2p-lending.

In the first 6 months of 2015, almost 50 million Euro was raised via crowdfunding, which is double the amount raised in 2014. There are over 80 crowdfunding platforms active in the Netherlands, which makes it difficult for potential investors to gain an overview of the viable available investment opportunities. This article provides a general overview of the most important platforms active in the Dutch market. Furthermore, I will discuss some relevant topics in relation to crowdfunding, such as: diversification options, costs, default risks, cash flow, types of investment and the added value of a properly managed crowdfunding platform.

Overview investment options

In general, crowdfunding platforms in the Netherlands offer the option to invest in loans, subordinated convertible loans and equity (besides donations and the purchase of products). Each of these different investment options has benefits and drawbacks in terms of cash flow, risk and the potential upside can vary significantly:

Loans provide a direct cash flow to the investor as loans are usually repaid in monthly instalments. Loans only have a limited potential upside, maximized at the offered interest rate. Due to the monthly repayments, the risk decreases every month. Most crowdfunding platforms determine the interest rate based on the envisaged risk. As far as I am aware, there are no platforms active in the Netherlands that provide the option to “bid” on loans in auctions.

Convertible subordinated loans (also called convertibles) are considered to entail more risk than normal loans as convertibles are subordinated to (normal) loans and other claims. Investors generally expect a higher return in exchange for a higher risk. Instead of offering a higher interest rate, companies issuing convertibles via crowdfunding offer the option to convert these loans into certificates of shares.[1] The option to convert may be restricted by certain conditions such as (i) a specific period in which conversion must take place and/or (ii) the condition that a sophisticated investor invests at least amount “X” during the term of the loan. For an investor it is important to identify any conversion conditions that may apply. If the loan is not converted into certificates of shares during its term, the investor will receive the principal plus interest payments at the end of the term of the loan. These investments might not be interesting for investors looking for a steady cash flow, but they can be interesting for those who want to have a shot at a serious return.

Equity is normally being offered in the form of certificates of shares (equal to the convertibles described above). Again, investing in equity does not create a steady cash flow for the investor. The terms and conditions related to the certificates of shares may (and normally will) restrict the option to sell them. Therefore, investors are expected to wait for the moment the entire company is being sold to an investor, which can take a long time. Investing in equity might only be interesting for investors looking for long-term investments. Then again, these investments do have the largest potential upside as the investor will profit from every increase in value once the company is being sold.

Balancing risks

Each investor takes, or at least should take, the risk of default into account, especially when investing in high-risk companies such as start-ups. Business cases of start-ups have not yet been properly tested and most do not, or hardly have, any financial buffers. Should the financed company go bankrupt, practice shows that only in rare cases (only part of) the loan can be recovered. Normally, preferred creditors such as banks and the tax authorities will receive the benefit of all assets left in the company and there is nothing left for others. Some platforms try to reduce the risk by requesting a personal guarantee of the entrepreneur, but this is of little use if the person does not have any assets.

The actual difference between investments in loans, convertibles and equity from a risk perspective is small. Investors having certificates of shares have a larger potential upside than the holders of loans. One could say that investors almost bear the same risk, but with different potential upsides. In my opinion the most important reasons to choose for normal loans are the fixed term and monthly repayments. If you are not in a hurry to make a profit and are going for the highest potential return, convertibles and equity might be a more interesting option.

Overview largest platforms in the Netherlands

After selecting the preferred investment instrument, it is important to select one or more of the available crowdfunding platforms. Without aiming to be complete, I list the largest and most active platforms active in the Netherlands below:

Geldvoorelkaar.nl is the national market leader and funded over 825 projects, with a total sum of over 66,000,000 Euro. The platform focusses on p2p-lending and only provides investors the opportunity to invest in loans. Interest rates range from 4% to 9% depending on the risk score determined by Geldvoorelkaar.nl. All loans are being repaid in monthly instalments as of the first month. By investing in projects via this platform, it is fairly easy to generate a decent cash flow. Up to now, 3.5% of my investments on the platform have defaulted. As the principal of one of the defaulted projects was almost fully paid back, my average ROI still accounts for about 6.5% per year. The other defaulted project was probably a case of bankruptcy fraud, which I expect to happen more often in the future. The platform opens several dozen new projects every week, which creates sufficient opportunities to diversify your portfolio and reinvest your money. An investor must pay a fee equal to 0.3% * loan duration (in years) * invested amount (which amount will be refunded if the project defaults).

Oneplanetcrowd claims to be Europe’s leading sustainable crowdfunding platform. Since launching in 2012 it raised over € 6 million in funding for more than 100 projects. Oneplanetcrowd operates in Germany and the Netherlands and is planning to open in other European countries soon. It provides investors the option to invest in loans and convertibles (apart from donations and presale options) and offers some of the most interesting investment opportunities, such as Snappcar and Wakawaka Power. Various projects offer the opportunity to co-invest with sophisticated venture capital firms as these firms invest simultaneously with the crowdfunding campaign. In my opinion, this is a huge advantage for investors as VCs tend to do a thorough due diligence before choosing to invest. The platform only allows companies with a sustainable philosophy to start a campaign on the platform. Their goal is to provide high quality investments with a decent return to investors. Although this is a good niche market, the strategy makes diversification opportunities fairly difficult. Investors do not pay a fee on Oneplanetcrowd.

KapitaalOpMaatand Collin Crowdfund are some of the main competitors of Geldvoorelkaar.nl as these platforms focus solely on loans with loan periods ranging from 6 up to 120 months and interest rates of 5.5% up to 9% depending on the calculated risk. Almost 6.5 million Euro and 13 million Euro have been funded via these platforms, respectively. Investors on KapitaalOpMaat pay a one-time transaction fee of 0.9% and a yearly fee of 0.85% on Collin Crowdfunding. Both platforms provide discounts to investors investing more than certain thresholds.

Bondorais a European platform offering the opportunity to invest in loans on a European level. Although this is by far the most sophisticated (international) platform available to Dutch investors, its presence is fairly unknown to most Dutch investors. Already more than 35 million Euro has been financed via Bondora. Investors are allowed to choose their own investments on the primary market, but most loans are filled in advance by a bot. Therefore, it will be necessary to invest automatically via the provided bot in order to obtain sufficient loans. This enables the investor to invest in literally thousands of loans differing in purpose, country and risk. All loans are repaid in monthly instalments on a virtual account. Bondora also offers the option to purchase/sell investments to other investors on its secondary market (with a premium/discount) against a fee of 1.5%. Investors do not pay any fees on the primary market. Although Bondora claims an average ROI of 18.75%, many investors complain about the large number of defaults. As the minimum investment is only 5 Euro, the threshold is low.

Symbid is one of the established Dutch crowdfunding platforms and focuses on equity (certificates of shares) and loans. Although Symbid seems to suggest that already more than 300 million Euro has been invested via their crowdfunding platform, the actual amount funded by the crowd is closer to 6 million Euro. One of the advantages of Symbid is that it offers the option to sell your equity to other investors on the platform. Continue reading →

Seedrs, one of the tow biggest equity crowdfunding platforms in the UK (and probably in the world), has announced that it will open a new campaign offering shares to the crowd on Friday. To bid in the pitch and become a shareholder, interested investors need to register at the Seedrs website first and then wait for the campaign to open on Friday.

Jeff Lynn, CEO of Seedrs said:

Last month Seedrs announced its £10 million Series A round led by Woodford Patient Capital Trust and Augmentum Capital. As we explained, we have set aside £2.5 million of that round for existing shareholders and new investors to invest through a campaign on the Seedrs platform. …

The campaign will go live to members of our Leedrs Club (the group of our most active investors) at 9:00 am this Friday, 21st August, and it will then go live to all investment-authorised members at 12:00 pm the same day. … Investments will be accepted on a first-come, first-served basis, and although you will have several days to make payment after investing, we would suggest [investors] transfer any funds [they] wish to invest sooner rather than later.

Please note that by the time the campaign opens on Friday, a significant proportion of the £2.5 million will already have been taken up by existing shareholders exercising their pre-emption rights. We expect, however, that there will still be a good bit of room for new investors, and it is our hope that we will be able to use this opportunity to expand our investor base meaningfully.

I expect that this offer will fill very quickly. The last comparable offer by Crowdcube, Seedrs main competitor, was filled within minutes.

UK platform Crowdcube today announced that it has raised 6M GBP of investment to further accelerate its growth. The investment is led by Numis, a UK stockbroker and corporate advisor. Tim Draper and London-based Draper Esprit have also joined this new funding round alongside existing backers Balderton Capital, one of Europe’s largest venture firms.

The investment will enable Crowdcube to accelerate growth, continue the expansion of its team, ramp up new product development including the creation of a new solution for companies going public, and invest further in its acclaimed marketing activities.

‘We’re on a mission to help more businesses raise the finance they need to grow, create jobs and deliver returns to investors. We’ve dominated the democratisation of seed-stage equity investment since we launched in 2011 and we’re determined to do the same for larger businesses. We want to put the Public back into IPO.’ commented Darren Westlake, CEO and co-founder of Crowdcube.

This round puts the Crowdcube at 51M GBP post investment. Continue reading →