P2p lending site Smava.de for the first time reached more than 1 million Euro (approx. 1.4 million US$) loan volume funded in one month. One factor contributing to this is that Smava is in the top 10 rankings for German Google search results for the keywords kredit (engl. loan) and kredite (engl. loans) since the end of May. I find it interesting that there is not one single bank site in the top ten for these search results.

German p2p lending service Smava.de launched two year ago. Since the launch of Smava 1350 loans were funded for a total loan volume of about 7.9 million Euro (approx. 10.7 million US$).

Lender’s viewpoint

So far lenders on Smava did well. There are approx. 2500 lenders active on Smava. Despite the credit crisis, 99% of the lenders earned a profit in 2008 (total 210,861 Euro), while the 1% who did incur a loss, lost only 60 Euro.

So far ROI in the range from 5-10% have been realistic. As of today 75 loans have defaulted, which is (in percent) more then was originally predicted. The Anleger-Poolmechanism spreads the losses of a default across all loans of a credit grade, which prevents total losses of investments. Therefore when 3 in 100 loans in credit grade X default, the lenders invested in the defaulted loans still receive 97% of the principal, while for lenders in the current loans returns are lowered by 3%.

Technically and on the process level Smava functions as promised.

Borrower’s viewpoint

Provided the borrower has a credit grade of at least ‘H’ (95% of the German population have credit grades between ‘A’ and ‘H’ so about 5% are excluded) and he has a sufficient income, chances for obtaining a loan through Smava are good. About 60 percent of the listings were funded. In February 2009 Smava raised the fees for borrowers from 1% to 2-2.5%.

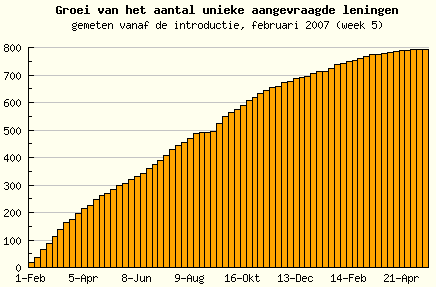

Marketplace development

Smava shows continuous growth, with the volume of new loans per month approaching 1 million Euro (see chart)

Despite extensive and positive press coverage Smava is still a niche market with less than 5000 active users. Looking at the distribution of lenders by amount invested, the top 50 Smava lenders funded about 1,690,000 Euro (or about 21% of total loan volume). Currently lenders are limited to a maximum of 100,000 Euro investment.

(Development of Smava average nominal interest rates for new loans; Source: smava loan statistic, Wiseclerk.com, 03-21-08)

I would estimate that the increased fees allow Smava to cover the variable costs. But to cover fixed operating expenses Smava needs to multiple its volume. First priority of Smava must be to accelerate growth.

Loanland launched last December as the first p2p lending company in the swedish market (see ‘Loanland launches peer to peer lending in Sweden‘). Since then about 5.7 million SEK (approx. 0.75 million US$) loan volume has been funded .

Ville Vesterinen has published more information about Loanland in the ArcticStartup blog:

The company is currently providing unsecured loans to the Swedish market. The Swedish market for unsecured loans to households amount to around 160 billion SEK (around 16 billion EUR or 20 billion USD) at present and with unsecured loans to SMEs the figure is about 500 billion SEK (around 50 billion EUR or 63 billion USD). The market has grown 15% annually during the last few years. … Loanland is using an open source platform that it has developed, automating most of the processes. The technology is based on Java, J2EE, MySQL, Tomcat, Spring and Hibernate. The platform and auction engine allows individual and automatic bidding, electronic signatures, integrated credit scoring and efficient payments.

The company … has already over 10 000 members and 5 000 registered borrowers and lenders. They have 6 million SEK (600K EUR or 750K USD) deposited out of which 95 percent is lend out as loans. Quite significant number considering that the startup operates currently only in Sweden.

Demand at Boober.nl is slowing. When I checked today only two loan listings were open. The following curve showing unique loan requests definitly shapes in the wrong direction. Boober lenders discus this development in this forum thread.

Since the launch 15 months ago, about 2.4 million Euro (about 3.8M US$) loan volume has been funded through Boober.

German Smava.de has funded about the same volume (2.3 million Euro) but after a slower start 14 months ago, lately the volume growth accelerated moderately.

MyC4 has successfully funded 1000 loans to entrepreneurs in Africa since launch in May 2007. So far none of the loans has defaulted and average interest rate for lenders is 11.7%. Tim Vang, one of the co-founders of the Danish startup told P2P-Banking.com that the MyC4 will release a new version in May with a new design and better interface. MyC4 also plans to provide loans in additional countries (currently Uganda, Kenya and Cote d'Ivoire).

MyC4's annual report 2007 is available on the Internet (English and Danish). While the company realised a loss of 2.8 million DKK (approx. 0.6 million US$) in 2007, it aims for break even in 2009.