In the chart below are the loan originations for April. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in April 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month

In March Lendinvest reported a surge in loan originations and had an exceptional month with more volume originated than Ratesetter or Funding Circle. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in March 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month

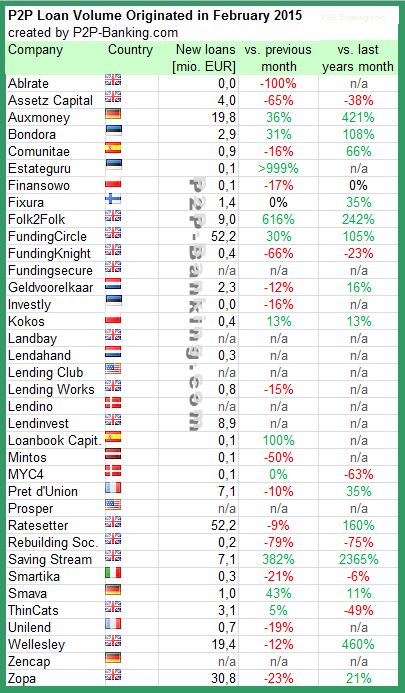

As February was a shorter month, loan originations fell compared to January with some exceptions. Ratesetter and Funding Circle are in a neck-and-neck race for largest volume figure this month. Prosper and Lending Club no longer publish origination data for the most recent month. I added two more services. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in February 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations.

Lending Club just announced the 4th quarter numbers in the investor conference call.

CEO Renauld Laplance stated: “We have continued to expand our reach through 2014 by doubling the size of the business again, while continuing to invest heavily in future growth and risk management. Our IPO in December was an important milestone in the life of the company, and everyone at Lending Club is excited about the next 5 to 10 years and committed to delivering more value and a great experience to our customers. 2015 is going to be another investment year, and we intend to continue growing originations and revenue at a fast, yet deliberate pace.”

Fourth Quarter 2014 Financial Highlights

Originations – Loan originations in the fourth quarter of 2014 were $1,415 million, compared to $698 million in the same period last year, an increase of 103% year-over-year. The Lending Club platform has facilitated loans totaling over $7.6 billion since inception.

Operating Revenue – Operating revenue in the fourth quarter of 2014 was $69.6 million, compared to $33.5 million in the same period last year, an increase of 108% year-over-year. Operating revenue as a percent of originations, known as our “revenue yield”, in the fourth quarter was 4.92%, up from 4.79% in the prior year.

Adjusted EBITDA(3)  – Adjusted EBITDA was $7.9 million in the fourth quarter of 2014, compared to $6.5 million in the same period last year.

Net Income/Loss– GAAP net loss was ($9.0) million for the fourth quarter of 2014, compared to a net income of $2.9 million in the same period last year. Lending Club’s GAAP net loss included $11.3 million of stock-based compensation expense during the fourth quarter of 2014.

Earnings (Loss) Per Share (EPS)Â – Basic and diluted loss per share was ($0.07) for the fourth quarter of 2014 compared to EPS of $0.00 in the same period last year.

Adjusted EPS(3)– Adjusted EPS was $0.01 for the fourth quarter of 2014 compared to $0.02 in the same period last year.

Cash and Cash Equivalents – As of December 31, 2014, cash and cash equivalents totaled $870 million, with no outstanding debt.

“We are entering 2015 with strong momentum on many fronts, and we intend to continue to execute on our strategy of fast yet disciplined growth,” said Carrie Dolan, CFO of Lending Club. “We will also continue to aggressively invest in product development, engineering, process automation, and the buildup of support and risk management functions to pave the way for our long term growth opportunity.”

Outlook

Based on the information available as of February 24, 2015, Lending Club provides the following outlook:

First Quarter 2015 Operating Revenues in the range of $74 million to $76 million. Adjusted EBITDA(3) in the range of $6 million to $9 million.

Fiscal Year 2015 Total Revenues in the range of $370 million to $380 million. Adjusted EBITDA(3) in the range of $33 million to $42 million

(3) Adjusted EBITDA and Adjusted EPS are non-GAAP financial measures

Strategy is to focus on the US market in the near future. There is no urgency to expand into international markets. There is not a lot of clarity which of the different models in particular geographies might prevail in customer adoption and get blessed by regulator.

The new study ‘Moving Mainstream – The European Alternative Finance Report‘ is available now (free download). The study by the University of Cambridge and EY looks at the development of p2p lending, p2p equity, crowdfunding and other alternative finance offers in Europe and compares it to the development in the UK. The very comprehensive study combined survey results from 205 platforms in 27 European countries with 50 survey responses gathered from UK platforms as part of the Nesta Study.

P2P-Banking.com was one of the research partners in this study.

Here are the main findings from the executive summary:

Since the global financial crisis, alternative finance – which includes financial instruments and distributive channels that emerge outside of the traditional financial system – has thrived in the US, the UK and continental Europe. In particular, online alternative finance, from equity-based crowdfunding to peer-to-peer business lending, and from reward-based crowdfunding to debt-based securities, is supplying credit to SMEs, providing venture capital to start-ups, offering more diverse and transparent ways for consumers to invest or borrow money, fostering innovation, generating jobs and funding worthwhile social causes.

Although a number of studies, including those carried out by the University of Cambridge and its research partners, have documented the rise of crowdfunding and peer-to-peer lending in the UK, we actually know very little about the size, growth and diversity of various online platform-based alternative finance markets in key European countries. There is no independent, systematic and reliable research to scientifically benchmark the European alternative finance market, nor to inform policy-makers, brief regulators, update the press and educate the public. It is in this context that the University of Cambridge has partnered with EY and 14 leading national/regional industry associations to collect industry data directly from 255 leading platforms in Europe through a web-based questionnaire, capturing an estimated 85-90% of the European online alternative finance market.

The first pan-European study of its kind, this benchmarking research reveals that the European alternative finance market as a whole grew by 144% last year – from €1,211m in 2013 to €2,957m in 2014. Excluding the UK, the alternative finance market for the rest of Europe increased from €137m in 2012 to €338m in 2013 and reached €620m in 2014, with an average growth rate of 115% over the three years. There are a number of ways to measure performance across the various markets. In terms of total volume by individual countries in 2014, France has the second-largest online alternative finance industry with €154m, following the UK, which is an undisputed leader with a sizeable €2,337m (or £1.78bn). Germany has the third-largest online alternative finance market in Europe overall with €140m, followed by Sweden (€107m), the Netherlands (€78m) and Spain (€62m). However, if ranked on volume per capita, Estonia takes second place in Europe after the UK (€36 per capita), with €22m in total and €16 per capita.

In terms of the alternative finance models, excluding the UK, peer-to-peer consumer lending is the largest market segment in Europe, with €274.62m in 2014; reward-based crowdfunding recorded €120.33m, followed by peer-to-peer business lending (€93.1m) and equity-based crowdfunding (€82.56m). The average growth rates are also high across Europe: peer-to-peer business lending grew by 272% between 2012 and 2014, reward-based crowdfunding grew by 127%, equity-based crowdfunding grew by 116% and peer-to-peer consumer lending grew by 113% in the same period.

Collectively, the European alternative finance market, excluding the UK, is estimated to have provided €385m worth of early-stage, growth and working capital financing to nearly 10,000 European start-ups and SMEs during the last three years, of which €201.43m was funded in 2014 alone. Based on the average growth rates between 2012 and 2014, excluding the UK, the European online alternative finance market is likely to exceed €1,300m in 2015. Including the UK, the overall European alternative industry is on track to grow beyond €7,000m in 2015 if the market fundamentals remain sound and growth continues apace.

Most major services grew the originated loan volume in January. Prosper, like Lending Club before, no longer makes data available for the recent month. Funding Circle passed the milestone of 500M GBP lent since inception, while Auxmoney crossed 150M EUR. I added Investly and Mintos. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in January 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations.

Notice to p2p lending services not listed: If you want to be included in this chart in future, please email the following figures on the first working day of a month: total loan volume originated since inception, loan volume originated in previous month, number of loans originated in previous month, average nominal interest rate of loans originated in previous month.