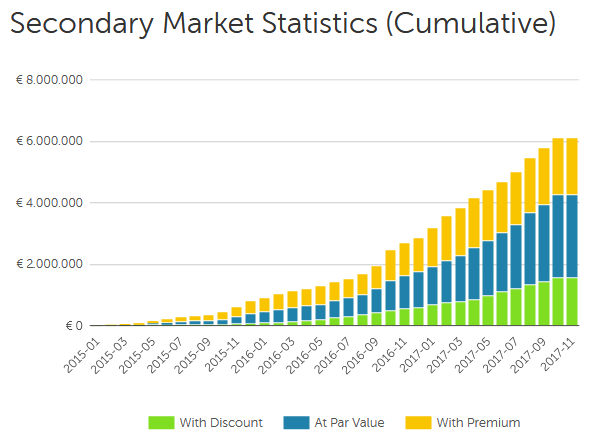

Latvian p2p lending marketplace Mintos announced today that all transactions on the secondary market are now free.

Exciting news! Starting from today, November 1, 2017, we have removed the 1% fee for selling loans on the secondary market of the Mintos marketplace. This means from now on, there are absolutely no fees for investing through Mintos.

“A secondary market with no fee will greatly benefit our investors. We expect the secondary market to become even more liquid now. This is especially good news for investors who want to pursue a long-term investment strategy and invest in loans with longer maturity. In the case investors will need the liquidity before the loan matures, they will be able to sell their investment with no extra fee added,†says Martins Sulte, CEO and co-founder of Mintos.

The monthly volume of traded loans on the secondary market is about 300,000 Euro per month.

Baltic Bondora stopped charging fees on its secondary market in November 2015.

‘Easy access’ investment will be available in a RateSetter ISA

RateSetter has improved customers’ access to their money by removing all early exit fees from its monthly investment market. This means that RateSetter’s 33,000 investors can now benefit from great rates of return combined with easy access to their money.

RateSetter’s monthly market has proven very popular with investors, delivering an average rate of 3.1% p.a. over the last five years. The latest rate can be found here.

As with all marketplace lending, the speed of access to money is dependent on liquidity. RateSetter has managed market liquidity for over five years, the result being that no investor has ever had to wait to withdraw their money from RateSetter. Early withdrawal fees remain in place for RateSetter’s one year, three year and five year investments. More information can be found here. RateSetter is looking at options to simplify the way fees are calculated to provide greater certainty to investors.

The announcement comes less than two months before the launch date for the Innovative Finance ISA (IF ISA) on 6 April and follows the release of information on RateSetter’s forthcoming IF ISA over a week ago. RateSetter has confirmed that customers will be able to invest in any of its markets within an IF ISA wrapper, and thus can benefit from easy access investments with tax-free returns. Continue reading →

Everybody talks about the win-win situation p2p lending offers for lenders and borrowers. By cutting out the large spread a bank takes when making a loan, the lender can get a higher interest rate, than he might in a savings account and the borrower may get a lower interest rate, than using his credit card. But who does actually decide what the interest rate for a p2p loan will be?

Several market mechanisms have developed. P2P lending services use combinations of these to built their platforms. I’ll describe some of the elements:

Individual Loan Listings vs Markets: With Listings (e.g. Prosper, Lending Club, Auxmoney, Isepankur) lenders can look at individual loan listings and see multiple parameters (e.g. credit grade, income, DTI, occupation, location,…). The lender can select (“filter”) loans based on his strategy. This is not necessarily a manual process as he can opt to use automatic bidding tools that make the selection for him based on criteria he set in advance. Other p2p lending services use Markets (e.g. Zopa, Ratesetter) which combine loans based on broader criteria (e.g. loan term, or credit grade). Here a lender can only decide which market to invest into, but does not pick individual loans.

Close at Funding vs Auctions: Some p2p lending services close loan listings once they are 100% funded. The loan is then originated. Others uses an auction process where the listing is open for bidding for a set time. If the loan amount is 100% funded then the bidding continues for the remaining auction period. New bids at lower interest rates push out old bids at higher interest rates, thereby lowering the final interest rate for the borrower. Some p2p lending services allow loan listings of both types or let the borrower prematurely end an auction (e.g. Rebuildingsociety, Isepankur, Assetz Capital).

Uniform vs Mixed Lender Rates: After an auction the interest rate for the borrower can be set at the rate of the highest successful bid. In this case all lenders on the same loan get the same uniform interest rate (e.g. Isepankur). Another option is to calculate the interest rate as an aggregate of all successful auction bids. In this case each lender gets the rate he did bid – there will be a wide mix of lender interest rates on the same loan (e.g. Rebuildingsociety).

Who does decide what the interest rate will be on a p2p loan

I. Borrower sets interest rate

The borrower decides, what (maximum) interest rate he is willing to pay (e.g. Smava, Auxmoney, Isepankur). The lenders can then decide, if they want to fund this specific loan at that rate or not. If there is an auction and lender demand is strong, then the borrower may get the loan for a lower interest rate then specified. Obviously lenders will fund loans with most attractive rates first and other loans will go unfunded. These borrowers can react by relisting at a higher interest rate. Continue reading →

Documents available to P2P-Banking.com show that German p2p lending service Auxmoney raised a series A round in the end of 2012 from 2 companies. The new investors now hold 21.8% of the shares, the 3 founders Philip Kamp, Raffael Johnen and Philipp Kriependorf hold 40.4% of the shares and the remainder is held by various seed investors (mainly from Austria and UK). The volume of the Series A round was not disclosed. In fact the round itself was not announced in public.

Yesterday Auxmoney did change its business model. In the past Auxmoney approach was subject to continued criticism (see also), because Auxmoneys largest fee income came from listing fees that every applicant for a loan had to pay. And with 80-90% of applications not funded, many critics felt that this model was unfair to the borrowers.

New fee model

Since yesterday Auxmoney charges borrowers a transaction fee for funded loan applications, but no more listing fees. This is in line with fee structures used by most major p2p lending services. Lenders pay a 1% transaction fee on successful bids.

No more auctions

In the past Auxmoney used a mix of loan listings that closed when they reached 100% funding and loans with reverse dutch auctions. In future all loan listings run for a maximum of 20 days and close immediately when they reach 100% funding. Raffael Johnen, co-founder of Auxmoney told P2P-Banking.com: ‘Lenders told us, that when they had bidded, they wanted to be sure to have invested in the loan part and disliked when they were outbid in the course of the auction‘.

New interface

Auxmoney also redid parts of the user interface and the dashboard for lenders. Johnen promised faster and more transparent information from the collection process. Continue reading →

Multi-sided platform are platforms that need to attract two or more customer groups in order to create value. They interconnect these groups serving as intermediary setting the rules. The platform need to achieve satisfactory results for both/all sides.

One example are video game console manufactures. The product will only attract enough buyers if enough games are at available. Developers on the other hand will prefer those manufactures, that already sold large numbers of consoles and thereby offer a large potential of customers.

Another example is Google. One customer group are the users. The value proposition here is ‘free search’. With the huge audience Google has and the algorithms for matching, Google can offer targeted ads to advertisers.

So Google gives away search for free, in order to make profit from charging advertisers. In this case there was not much alternative in deciding which customer segment to charge. But sometimes both customer segments are charged and it is hard to decide which side to charge (more).

P2P Lending services are obviously multi-sided platforms, too. They need to match borrowers and lenders. Ideally there will be roughly the same level of demand as of supply of capital.

The current situation is that most p2p lending services charge borrowers more fees than lenders.

Possible causes for this are:

At the inception of p2p lending services, opinion was that it is harder to convenience lenders to trust this unproven model and unknown new company running the service – therefore lenders were charged nothing or little to not build entrance barriers

Orientation on established models for loans – banks charge borrowers fees too, therefore borrowers will accept these as usual

Cost-bast pricing: In vetting a borrower the service will incur costs, whereas a new bid by a lender will incur close to zero costs as it can be processed automatically. Even higher than the vetting costs are the customer acquisition (marketing) costs to obtain borrowers.

Now years after launch, most p2p lending service are “short” of (good) borrowers. Their lenders have a surplus of capital that could be lend out, would there be more loan applications on the platform. And typically customer acquisition costs are much higher for winning new borrowers than for winning new lenders. Furthermore borrowers must be acquired over and over again, whereas lenders remain customers for longer periods of time and reinvest capital.

The logical consequence would be for the p2p lending marketplace to change the pricing. By charging borrowers less and charging lenders more, the value proposition to borrowers would be lower APRs, attracting more borrowers.

A counter-argument voiced against this, is that pricing would not change, because lenders would just raise the interest rates they offer to cover the higher fees. This will happen to some degree, but I think how much is dependent on the model the p2p lending marketplace works. In a market place where lenders do set interest rates themselves (e.g. Ratesetter) this will in my opinion be likelier than in a markplace where the operator sets the interest rates (e.g. Lending Club) or where the initial rate is set by the borrower (e.g. Smava) and can possibly be bidden down (e.g. Isepankur). Furthermore even if costs for borrowers overall would not change, the marketing-message could – ‘fee-free loans’ will be more appealing.

This change would need to be a gradual shift as existing lenders are accustomed to current prices and will resent higher fees. For the p2p lending service the effect per loan could be neutral. The amount of fees earned per loan would stay the same, just the proportion of the parts payed by lenders vs. borrowers would change.Continue reading →

Auxmoney.com is the second largest (by loan volume) p2p lending service in Germany. The new loan volume per month is about 700,000 Euro (approx 900,000 US$). A recent estimate puts the monthly revenue of Auxmoney at about 57,000 Euro (approx. 74,000 US$; based on August numbers). The majority of these revenues comes from the sale of so-called ‘certificates’, which the borrower can optionally buy. Examples for certificates are credit scores, income validations or car value assessments.

The fees for the optional certificates as well as the listing fee are due in any case – regardless whether the borrower’s request for a loan is funded or not.

Effective September 1st, 2010, Auxmoney raised several fees:

Lender fee for successful bids is now 1% of bid amount – at least 1 Euro (previously there was a flat fee of 1 Euro per successful bid)

Borrower fees for successfully funded loans are now 2.95% of loan amount (previously 1.95% or 2.50% of loan amount depending on loan term)

A new rule in the terms and conditions states that the auction duration of a listing that has not completely funded after 14 days will automatically prolong as long as the listing is not funded or the maximum duration of 90 days is reached or the borrower objects to the prolongation. The borrower can object to the extension any day he wants by pressing a button in the online interface. If he does that the listing ends after 5 more days. Every additional day (!) of extension (beyond the original 14 days) the borrower is charged 1 Euro (approx. 1.28 US$). Therefore if the loan does not fund within 90 days and the borrower did not stop the listing, he is charged 76 Euro extension fee on top of the original 9.95 Euro listing fee.

With the legal construct Auxmoney has selected, the listing fee, the fees for the certificates and the extensions need not be factored into the APR that Auxmoney calculates.

Could these circumstances damage the image of p2p lending?

P2P Lending worldwide has received positive press coverage and benefits from offering an alternative to the currently ill reputed banking sector. Only occasionally are single players causing bad publicity (e.g. the high default rates of Prosper or the Boober failure). Looking at the German market, press coverage for p2p lending was nearly all positive. One exception was the warning of a well-known consumer advocacy which accused Auxmoney of using false marketing claims on its website. Auxmoney sued the publisher – the case is still ongoing.

The latest change in the fee policy of Auxmoney could lead to a negative change in the perception of p2p lending by consumers. Should internet users start to associate p2p lending with high fees that are charged even if no loan was obtained (currently on average 10-20% of all loan listing on Auxmoney are funded – see green line in this chart) then p2p lending would risk losing any competitive advantages over bank loans.

Fees at other p2p lending services have risen several times in the past too in the struggle of these marketplaces to become profitable. While these fee increases do impact the attractiveness for the users the difference is that at least the fees in most cases only apply to loan transactions on funded loans.