From Tuesday till Friday I was in Riga for the Finfellas Riga Conference. I spent the day before the conference in scheduled meetings at the offices of several platforms to update me on current news and keep in touch with platform managers. A preparty in the evening allowed to “warm up” and exchange news, ideas and gossip. The conference itself started on Thursday. Most of the Baltic platforms were present. Total attendance I would estimate about 250 to 300 persons consisting of representatives for platforms, loan originators, service providers (e.g. legal, payments, …), financial institutions, regulators, investors and bloggers. The conference was very well organized and featured panel discussions, presentations and demos over the two days as well as an exhibition area with platform booths. The best part as always for me was the networking opportunity.

As several platforms have received licenses by the regulator meanwhile, one of the main topic was the maturing of the industry and the advantages that come with regulation (e.g. reduced counterparty risk, and better matching to suited investor due to required suitability tests).

The trend to simplified product selection (one click investing, autoinvest, streamlined UIs) continues .

The overall mood was confident and optimistic after having navigated two black swan events (pandemic & Russian invasion of Ukraine) in the recent past.

Assuming the conference will be held next year in Riga again: See you all there!

I am looking forward to attending the P2P Conference 2020*, which takes places in Riga on June 19th/20th. If you want to go too, you can order your tickets using this link P2P Conference 2020* together with code Claus for 20% discount (click on ‘enter promo code’ on the page where you enter the ticket quantity).

I went to the conference last year and enjoyed it. You can read my article about it here.

This year I plan to arrive a few days earlier (on the 16th) in Riga, using the time to meet up with platform representives. I also plan to organize a lunch or dinner meetup for P2P-Banking readers so we can chat and discuss current p2p lending developments. If you are interested send me an email and I’ll inform you once the planning is further advanced.

On Friday and Saturday I attended the P2P Conference* in Riga. It was the first p2p lending conference in Riga and I was very impressed how well organized it was for a new event. Kudos to the Targetcircle staff who organized that. The audience was platforms, retail investors and bloggers/youtubers mainly from the Baltics and Germany but also sprinkled in from other countries all over Europe. I would estimate about 350 to 400 people in total.

Platforms presenting and attending were nearly exclusively from Eastern Europe (mainly the Baltics). Most of the retail investors came for the chance to meet and speak to the platform representatives in person.

The organizer of the conference is Norwegian affiliate technology company Targetcircle. Targetcircle was founded in 2014. I became aware of them when Mintos switched their affiliate tracking from an inhouse solution to their system around November 2016. Since then they won a wide variety of Eastern European p2p lending platforms as clients for the affiliate tracking solution, but also recently the Irish platform Flender*. Targetcircle concentrates on the underlying technology as a marketing solution for fintechs but also as a (whitelabel) technology for other affiliate networks. The CEO told me he aims next to win more clients for his solutions in the UK and Spanish market and then later on in East Asia.

The conference started with a day of presentation, demos and time to visit the exhibiting platforms at their booth. There was ample time for networking with good catering (outside barbecue with DJ music). A recorded livestream video of the main stage activity is available here.

I really enjoyed the opportunity to talk to so many platform representatives, other bloggers and hear the opinion of many retail investors from recently started to 10+ years investing into peer to peer lending. In general the investor crowd was optimitic about the future prospects of investing into p2p lending and we all exchanged experiences, opinions and tipps on strategies, selecting platforms and evaluating risks.

The atmosphere was very relaxed and informal and it moved to a vacation feeling when on Saturday the venue was located on a beach at a lake.

Attendees spent most of the time chatting and networking, but some more venturous ones took up the offer to try wakeboarding or stand up paddling or got active playing volleyball or boule.

Targetcircle plans to do the conference again next year and I am looking forward to going again.

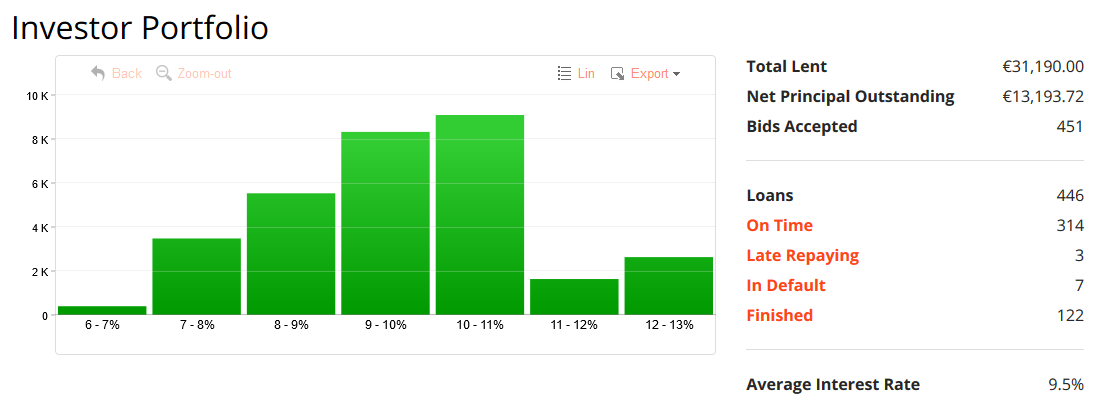

I covered my p2p lending portfolio periodically over the past 12 years in this blog. The following report is a snapshot on how it is composed right now (May 2019) and which strategy I will take for the next months. As you can see below I aim for a widespread diversification (over different platforms as well as geographically) of my p2p lending investments.

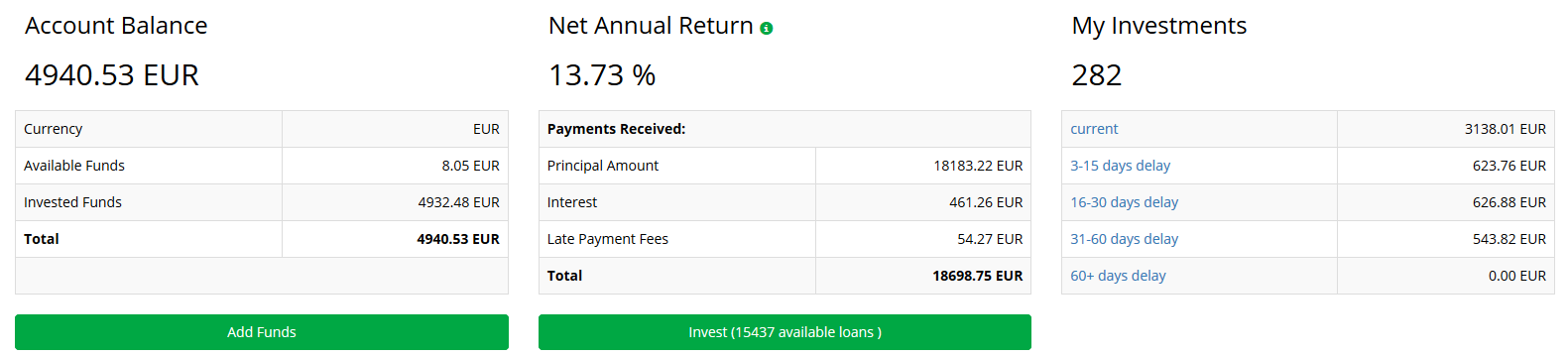

Mintos

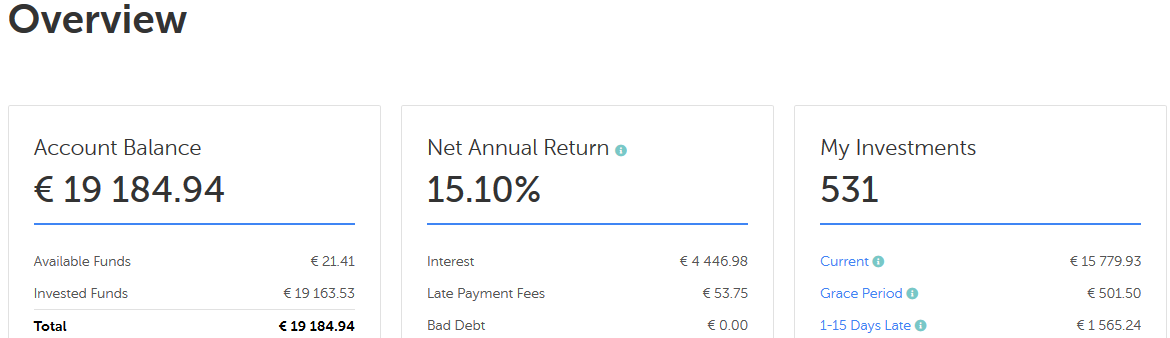

Mintos* is my biggest position. I run a trading strategy on Mintos. Mintos gives my net annual return as 15.1%. Calculating it myself based on the deposits and withdrawals I get a XIRR value of 24.8%. The cause for the huge discrepancy is that Mintos does not account correctly for the cashback of the campaigns. I heavily traded, when Mogo ran a campaign. For example I invested in new Mogo loans that were offered with a 2% cashback on the primary market, nearly instantly sold them with 1.8% discount on the secondary market and pocketed the cashback. Rinse and repeat.

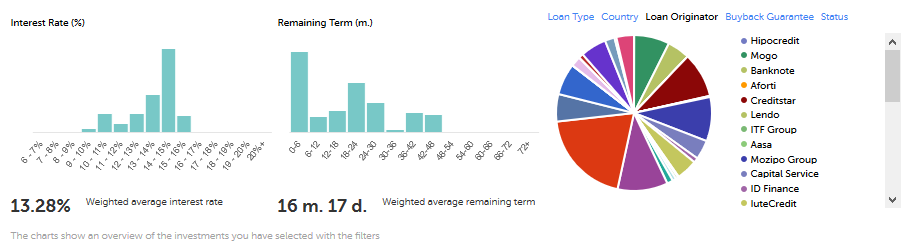

I am satisfied with the current degree of diversification over loan originators in my Mintos portfolio. The bulk of my investments is in loan terms between 3 and 30 months at interest rates ranging from 13% to 15%. The lower interest rate loans are usually only held temporary as part of my trading strategy.

For the coming month I plan to keep my Mintos* investment at roughly that amount, reinvesting the paid principal and interest. New investors registering via this link at Mintos, get 1% cashback on amounts invested in the first 90 days. Mintos is currently not accepting UK investors.

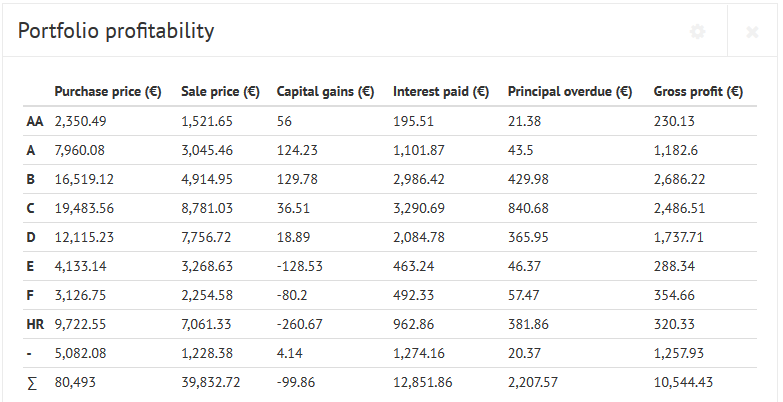

Linked Finance

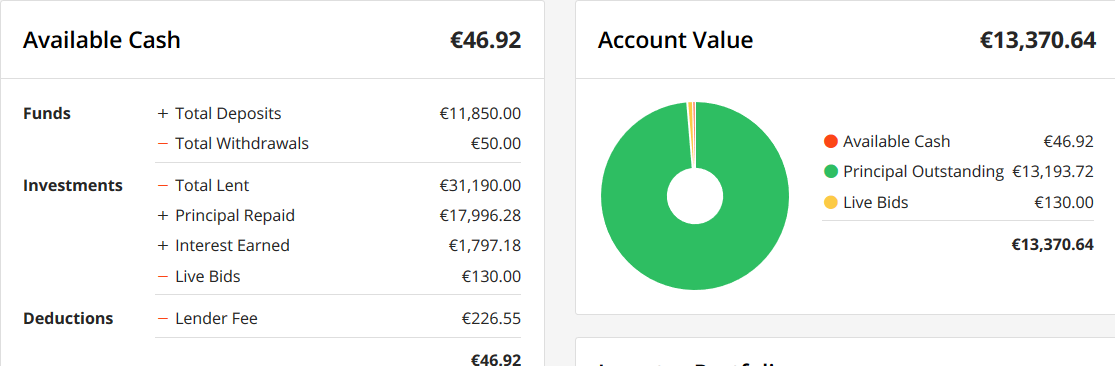

My second largest p2p investment is on Irish SME loan platform Linked Finance.

Diversification achieved is good. The majority of my loans have interest rates between 8% and 11%. Most loan terms are 2 or 3 years.

I “collected” 7 loans in default (double dip on the golf loan). But 5 of these had repaid more than half the principal before they want into the default state so the principal in default sums up to only 270 Euro. My self-calulated XIRR value is 6.4% if I totally write off the amounts in default and 7.1% if I assume that half the amount in default will be recovered. I plan to slightly increase my Linked Finance* portfolio in the next months. Linked Finance is not offering any cashback or bonus rewards for new investors.

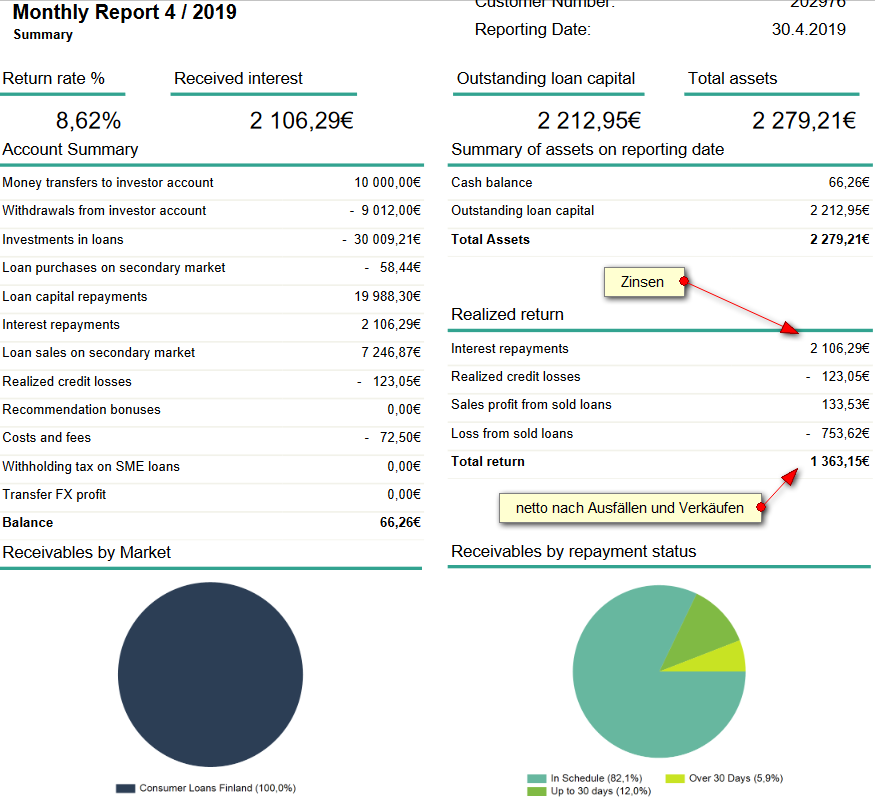

Bondora

Bondora is my third largest and oldest (still running) p2p lending portfolio. I started in 2012. My self calculated XIRR value is 16.6%. A yield that high is not achievable nowadays anymore. My portfolio profited heavily from the first years when interest rates were typically 28% to 34%.

I am currently investing into Estonian A and B loans using these autoinvest settings. I have used these settings unchanged for 11 months now and it is running totally hands-off with no maintenance required.

On Bondora* I reinvest the bulk of my repayments and occasionaly withdraw some funds. New investors registering on Bondora using this link get a 5 Euro sign-up bonus.

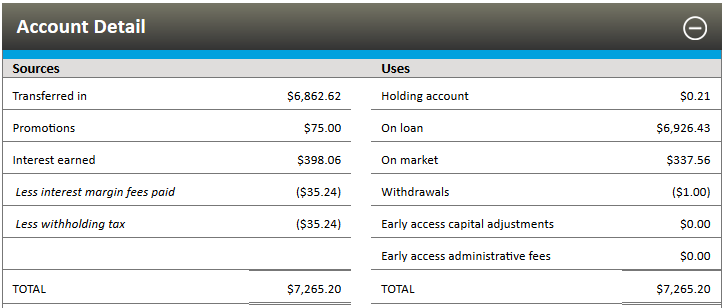

Ratesetter Australia

Ratesetter Australia* is my fourth largest p2p investment and also one of my youngest. I started in August 2018. My XIRR value self calculated in AUD is 9,1% if I include the 75 AUD sign-up bonus and 7.4% if I do not include that.

My money is mostly invested on the Ratesetter 5 year market at an average rate of 9.2% (that is after fees but before withholding tax).

In the past months the interest rates have dropped considerably therefore I am parking some funds on the 1 month market or invest them on the 3 year market.

I am reinvesting all repayments at Ratesetter Australia. If rates go up again I plan to do that on the 5 year market, otherwise I’ll settle for the 3 year market. It is a little complicated to register as a non-resident, but I have described how I managed to sign up as a European here. New investors can earn a 75 AUD promotion bonus by investing 2,000 AUD or more in our 3 year Income or 5 year Income lending markets before 31st May 2019. Achieving that requirement in time will not be easy, even if you start directly.

Iuvo Group

The fifth largest position of my p2p portfolio is invested at Iuvo. It is running hands-off and does not require any maintenance.

I continue to reinvest all repayments. Iuvo pays new investors a very generous cashback of up to 90 EUR. For more details and how to get it see the cashback overview page.

Estateguru

After I completely exited Lendy in last autumn, baltic Estateguru* is now my largest platform for property secured loans. I don’t use the autoinvest. Instead I periodically login and manually invest into a new Estonian loan secured by a first rank mortgage.

I mostly reinvest all repayments. New investors get 0.5% cashback for all investments in the first 90 days, if they sign up using this link.

Fellow Finance

I used to have a larger portfolio at finnish Fellow Finance but I did not want to go below 12% for 4 star Finnish consumer loans therefore I started withdrawing funds last year. In January the sale price collections paid tor Finnish loans dropped from 70% to 53% which reinforced my decision to exit.

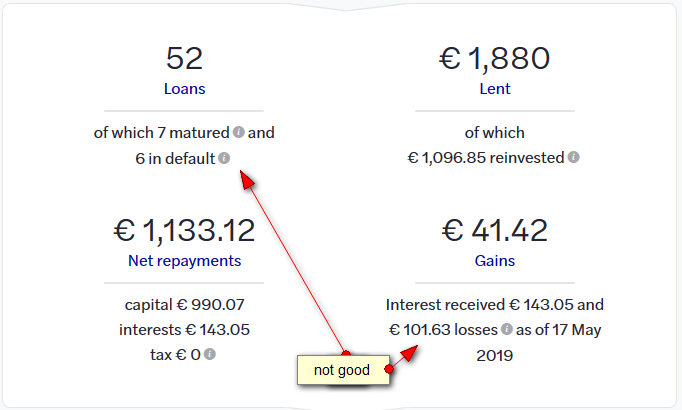

October

I am running down my portfolio on French SME loan marketplace October. With the low interest rates and rising defaults (6 out of 52 loans) in my portfolio the risk reward ratio is not for my taste anymore.

New investors signing up on October using this link* can get 20 EUR bonus (200 Euro minimum investment)

More p2p lending marketplaces

Due to professional interest (want to gain first hand experience) and curiosity I have more p2p lending portfolios at Ablrate* (small, reinvesting), Assetz Capital* (tiny, reinvesting, possibly increasing), Bulkestate* (tiny, testing), Crowdestate* (small, reinvesting), Finbee* (tiny, nearly exited), Investly (small, reinvesting), Lenndy* (tiny, watching), Monestro, (tiny, exiting), Moneything* (small, exiting), Neofinance* (small, testing, probably running down), Reinvest24* (small, testing), Robocash* (small, reinvesting), Zlty Melon* (tiny, exiting next month when terms are up).

Crowdinvesting

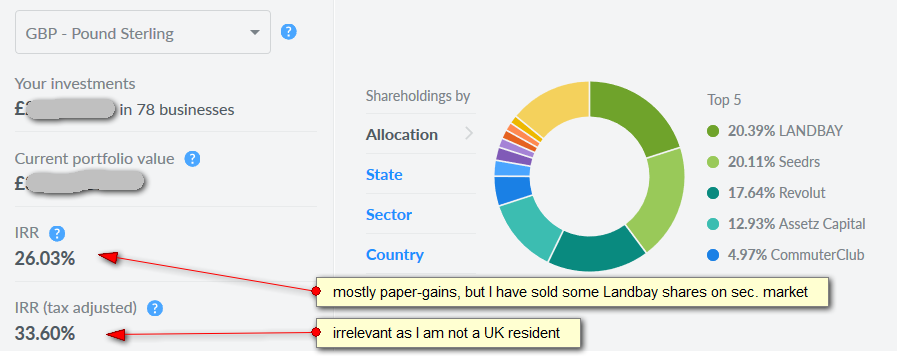

Not p2p lending but investing in startups. I am a huge fan of Seedrs*. Investing in startups is of course even higher risk than investing in p2p lending. Nevertheless I went ahead and built a big Seedrs portfolio over the last years. Snapshot:

P2P Conference Riga

I am looking forward to be at the P2P Conference in Riga* which is less than 4 weeks away. The conference is reasonably priced (enter promotional code P2PEARLYBIRD40 for 40% rebate) and Riga can be reached with cheap flights from many European cities. BTW, Riga is an interesting town, if you have not been there yet you could combine the conference with some sightseeing.

Lendit Europe time of the year again. My fourth time as a particpant of the London conference. It is now marketed as an ‘Event for Innovation in Financial Services’ and that means a wider scope of topics – and presenting companies – than in earlier years, when it had a single focus on p2p lending / marketplace lending. I truly enjoyed the conference, it had quality sessions and its high level attendants (more than 1100) allow great networking and making interesting contacts.

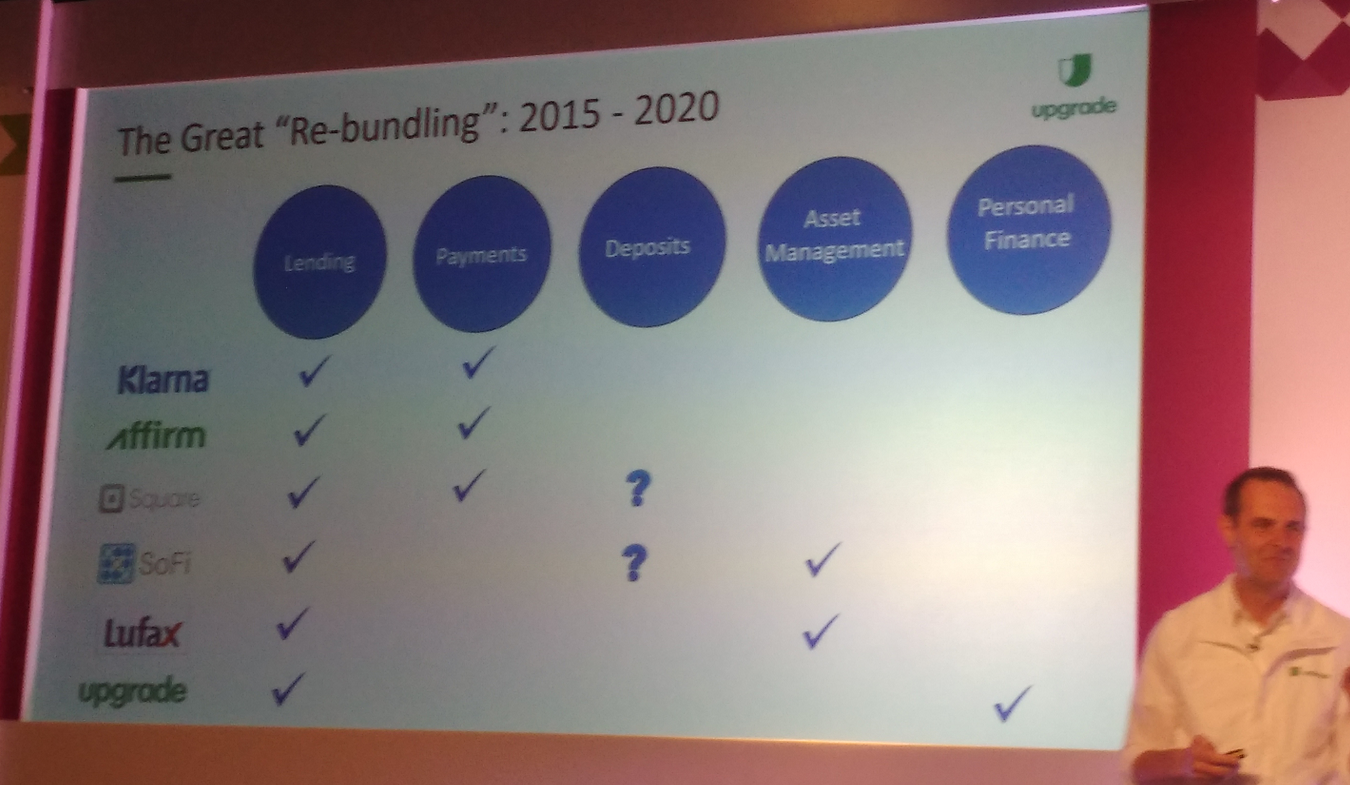

In writing this recap I find it much harder than in previous years to identify the main trends/topic that were discussed. There has been no single big announcement or issue happening that dominated the talks. So I’ll start with 3 predictions Renaud Laplanche, CEO Upgrade made in his motivating outlook on Online Lending 2.0:

Prediction 1: ‘The growth of online lending will accelerate in the next 15 months’

Prediction 2: ‘An organized secondary market for online loans will emerge in the next 15 months’

Prediction 3: ‘Continued re-bundling will give birth to at least one major consumer product innovation in the next 15 months’

From my viewpoint the first prediction is the one with the highest probability to come true, the second one is mainly important for the US market and it is actually the third one that is most interesting (but also most open).

His slide on rebundling examples

There are connections to another development that goes into the same direction and surfaced in several other sessions: More and more fintechs in this space are cooperating to better serve the customer and integrate multiple products into one user experience.

Furthermore there were several sessions around machine learning, artifical intelligence and automated underwriting with a wide range of opinions to what extend processes will be fully automated or whether human intervention or oversight is stll desireable for some specific decisions.

Looking at the scene from a geograhical perspective, many panelists emphasized that there are still a lot of difference between regions. The Americas, Asia or Europe (or even areas inside Europe) show a lot of differences no matter if the specific panel discussed funding, risk, investor yield, regulation or banking. So while many (especially VCs) would love to see fintech innovations that work globally and (if they are consumer faced) reach billions – that is extremly hard to achieve and therefore probably not going to happen in the near future.

This touches several speakers commenting and speculating whether the big tech giants like Amazon, Facebook, Google or Apple have ambitions and plans to offer financial services as they cater to a global audience, and what impact that would have on banks and fintechs. I found some aspects of this interesting, but mostly those discussions are futile because I feel there is such a lot of speculation involved and no real indicators that any of these companies are making steps in that direction. (sorry if there were any hard facts presented, I might have missed them as I did not see all the sessions).

I enjoyed Pitchit, where 8 startups battled for the vote of the jury and the audience. Swiss Sonect won both by hoping to replace ATMs by a platform approach where merchants can become the point where cash is dispensed (this is actually in collaboration with banks as they want to reduce the costs for maintaing ATM infrastructure and not anti-bank as it might sound on first impression).

All sessions at Lendit were recorded and will be made available over the next days here.

Seems like next year Lendit might come to a different location. The exit survey asked attendees to rate how they would like Frankfurt, Berlin, Barcelona vs London again.

I attended Lendit Europe in London the last days, an industry event of the p2p lending (or marketplace lending) industry. This was my third Lendit and it was not only bigger (904 attendees from about 180 companies) but again better than the previous year.

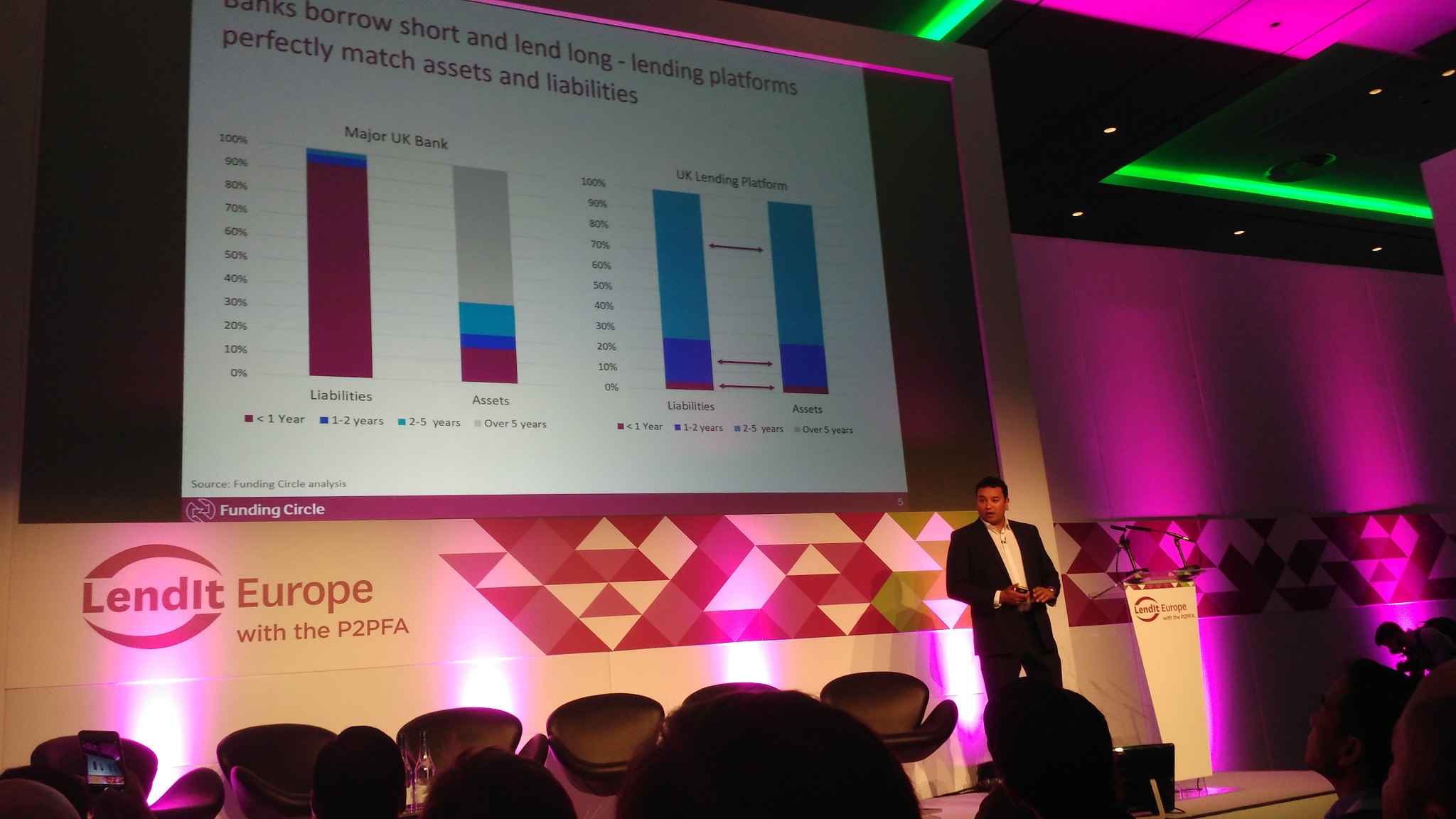

Samir Desai, CEO of Funding Circle in his opening keynote sees it as the golden age of the industry. And that certainly is the sentiment that much of the British part of the market would agree with. However there is headwind to be countered. The P2PFA, the association of the UK marketplaces that co-hosts the event, comissioned a report on the economics of peer to peer lending. Christine Farnish, the Chair of the P2PFA said that they did this to rebuke assertions by facts and counter comments by the tradional industry about risks.

The new Oxera report is available for free download here. Reinder van Dijk presented the findings of the report which focuses on the eight members of the P2PFA. He showed based on data, that in general the platforms did a good job on assessing risk, as the actual defaults for the years 2013 and 2014 were mostly in line or lower to the predictions the marketplaces made beforehand.

Lord Turner, former head of the UK Financial Services Authority created a media stir earlier this year with a very critical remark on p2p lending. In his keynote speech Turner did a turnaround saying he had not fully understood the p2p lending model in detail at that time and that he thought the interview was over when he made the comment. His final message to the marketplaces is keep it simple and transparent.

Impression from Lendit 2016 (own photo)

One major topic for the UK players is when FCA approval and the launch of the IF ISAs will occur. There is a feeling – but no certainty – that it’s getting closer. Farnish says she expects IF ISAs to be available by spring 2017. I also asked several people whether they expect it to be a big bang event, meaning that all the big players get approval at the same time to launch their ISA offer. Again there is no certainty but most respondents said they feel it would be only fair to grant the approval simultaneously because otherwise the first starter would have quite an advantage.

By the way most of the sessions, panels and demos are available here as videos and can be watched free. I recommend Cormac Leech’s keynote as a data rich, not easy to digest, but highly informative appetizer. Then for a second course with some added spice injected by Kadhim Shubber, FT, watch James Meekings of Funding Circle, Giles Andrews of Zopa, Peter Behrens of Ratesetter, Christian Faes of Lendinvest and Anil Stocker of Marketinvoice here. And for a maximum of contradicting opinions during one panel you might finish here, where Cormac Leech suggests that p2p lending marketplaces should monetize by ‘bombarding’ users with cross selling offers, not only for fintech related offers but for example also selling holidays. He think the bombarded users would be receptive if only the marketplace at the same time gives them a better rate. (I might be compressing his argumentation, please watch it in full). This to me is a stretch. I think that p2p lending marketplaces should deliver what the investors expect from them: great returns. Surely there is some opportunity for cross-selling with related financial products. On the other hand I do believe that the challenger bank (Monzo) present in this panel has some merit with it’s plan to analyse data to make fitting offers based on the budget and the spending pattern of the customer. Will that appeal to everybody? Certainly not. But the customers that will sign up with them are looking for a change from their previous banking experience so they might be open to that.

Another argument was on ‘pure’ marketplace lending model versus hybrid versus balance sheet based lending. While there are different opinions and preferences voiced, several speakers thought that there will be players of each type that are succeeding.

I actually missed many of the afternoon sessions of the first day, because one main benefit of Lendit for me is the networking opportunity. I talked to many marketplaces I knew, to keep up with their developments and plans, and made contact with new marketplaces. My view is a bit biased on topics of interest of retail investors from the continent so I am overweighting platforms news that are revelant to these in the following paragraph.

I checked with Saving Stream and they confirmed that they will lower interest rates with the intention to win more borrowers. The one size fits it all rate will be gone which takes away some of the straightforwardness/ease of use. I wasn’t told how much lower rates will go and on my question whether rates will vary depending on the loan risk, the answer was that this is yet undecided. Ed of Moneything said progress to growing loan volumes even further is good. Investly will disclose a new UI for investors soon. Aurora Exchange from Finland says it will not only launch there but will be able to serve all of Europe (not only from the investor side but also on the borrower side).

I had so many conversations, that I missed most of the Pitchit, which I had really looked forward to see. But I was in time to see the pitch by Lendingwell which was very good and as it turned out the next day that was the pitch that won.

I had the pleasure to moderate a panel on up and coming European platforms, this year featuring Creditshelf, Giromatch, Finbee and Viventor. I am looking forward to next year and am curious which great event location Peter Renton and his team will scout next time.