P2P lending service Bondora* has announced that in future it will focus completely on its hands-off investing product Go&Grow. From February 27th, the products called Portfolio Pro and Portfolio Manager will be discontinued. These allowed investors to select into which individual loans they wanted to invest. Bondora originally started and grew big with investment into individual loans and only 2018 introduced the simplified Go&Grow product which soon became very popular (read my coverage on the start of the Go&Grow product written 5 years ago). Over the years Go&Grow became more and more important for Bondora as investors seemed to prefer the easy to understand product with a fixed interest rate. Bondora’s marketing was focused on this type of investing and also Bondora made it harder to invest into the Portfolio Pro and Portfolio Manager products in the last years by allocating less available loan amounts for investment to these products. In the last years it was no longer possible to invest relevant amounts via Portfolio Pro as allocated investment pieces were only 1 Euro into each loan.

Therefore it comes as no surprise that today’s announcement by Bondora states that currently 96% of all investments are made via Go&Grow. Bondora points out that Go Grow is very easy to use ‘As portfolio diversification is automated, you can just add money, automatically earn returns, and continue living your life. ‘. The Go&Grow product offers up to 6.75% interest (limited for existing customers) or in the Go&Grow unlimited version 4% interest (unlimited, new and existing customers).

The secondary market will continue to operate beyond Feb. 27th. It will still be possible to sell and buy individual loans just not to invest into new individual loans.

Bondora* is one of the longest operating p2p lending services in Europe. The platform has more than 215,000 investors according to the website. Investments are into the underlying consumer loans, which Bondora originates via its website to borrowers in Estonia, Finland, Sweden and the Netherlands. There are few comparable p2p lending services that offer one fixed rate to investors without any configuration/selection possibilities.

Estonian p2p lending marketplace Bondora* announced today that for new customers the availiable Go&Grow interest rate is 4%. They can invest an unlimited amount in the product called Go&Grow unlimited. The Go&Grow tier with an interest rate at 6.75% will remain available only to existing customers that joined before August 24th, 2022. Currently that tier is limited to adding 400 EUR new investment per customer per month.

Bondora says this change is necessary, since they will prioritize launching new loan markets, new financial products, and newtarget audiences in the coming months.

According to the announcement Bondora has 200000 customers, which invested more than 650 million EUR.

Can you please give a short introduction on Bondora*?

Bondora offers a simple way to invest online. We’ve been around for over a decade and have more than 130,000 investors. This year, we announced our third consecutive year of profitability, and are on track for the fourth this year.

What is your background and when and why did you join Bondora?

I worked for two of the largest banks in the UK before joining Bondora. Traditional banking wasn’t for me. Things moved too slow and I wanted to see my work make a change. Around 3.5 years ago, I heard about Bondora by chance and decided to reach out. After speaking with Pärtel and the team, I was 100% sold on the mission. So I made the move to Estonia. I can honestly say it’s the best decision I ever made. Since joining, I’ve worked in a few different roles within Bondora, but my main responsibility is the investor product.

In reaction to the COVID-19 situation Bondora stopped originating new loans in Finland and Spain and also restricted the credit grades that are eligible for loans in Estonia. What was the reasoning for that decision?

We temporarily stopped lending in Spain and Finland as a precautionary measure. As we’re only lending in Estonia, this has significantly decreased our operating costs. Take marketing costs, for example. Marketing in one country to achieve a specific level of originations is much more cost-effective than trying to achieve the same across three countries. In a growth environment, this is not so much of a concern because you’re targeting expansion. But sustainability is our top priority. We will only change our strategy once the data is available to confirm whether we should start expanding again.

You recently capped the maximum amount that can be invested in Go&Grow at 1000 Euro per month. What is the reasoning for this and is this a direct result of the restriction to only lend in Estonia at the moment? In other interviews stated that Bondora could just increase marketing to allocate more loans in Estonia should investor demand increase. This measure seems to contradict that.

Overall, we made this decision for two reasons: 1) Sustainability of the portfolio 2) So everyone can still invest.

And the previous statement we made remains true. We could quite easily boost the portfolio if we wanted to. The demand is there. However, we are not going to make any shortcuts regarding the quality of the portfolio. With the current global situation, it is better to be cautious and assess the data once it is available rather than target exponential growth. Hence the €1,000 net limit per investor to match our originations. As a business, we do not need to generate enormous growth in our key metrics every year to stay afloat. If we choose to decrease our originations, our operating costs decrease in line with this.

Will you restart lending in Finland and Spain?

We do not have a decision regarding when we will restart activities in Finland or Spain yet.

As a result of the COVID crisis the Go&Grow product could no longer supply instant liquidity earlier this year. Instead partial payouts were enacted for withdrawals. I understand the situation is back to normal with instant payouts again, but can you please share looking back what it meant for your investors and how they reacted to this measure?

This was a necessary measure built into the product from day 1. When partial payouts were active, I read through hundreds of support tickets, social media comments and forums to try and grasp the overall reaction investors had. Most understood why we activated this feature and why it was critical to the sustainability of the product. It’s worth noting that nearly 6 months later, this has not impacted our key metrics (customer satisfaction, investments, withdrawals, referrals). Investors would not continue to use Bondora if they did not trust us and see us as a sustainable company.

A lot of questions from investors are about the buffer Bondora keeps to make Go&Grow more liquid. Bondora* in the past declined to disclose how much money there is in the buffer, can you please describe the mechanism as precise as possible? Where is the money from this buffer kept? Is it sitting in a bank account, meaning the buffer does not generate any interest? We aim to keep the cash reserve at roughly 15% of the Go & Grow portfolio. Of course, this may change based on daily withdrawals and money received. The money is on a segregated bank account, separated from Bondora’s funds. It’s there so investors can get fast access to their money when they need it.

One point of critic several investors have mentioned is the way Bondora treats late loans for calculating the net return figures in the investor dashboard. Only the amount of the overdue instalment rate is treated as late for this purpose not the whole outstanding loan amount. Critics feel that this leads to overly positive displayed net return figures creating expectations which are later deflated once the portfolio matures and the return calculations are lowered. What is your opinion on that and are there any plans to change the calculation method?

Overall, we have no plans to make any changes to our calculation methods. I think it’s important that we’ve remained consistent in our calculations, so the returns of the portfolio over the years are comparable. Treating the whole outstanding loan amount as late would also have its limitations. It would be overly negative because it disregards the 60% (for example) of the loan that would be recovered.

Bondora* provides a lot of information and statistics. One that seems to puzzle investors frequently is the “cumulative cash on cash return graphs in the public reports sections. Some of the charted lines do not seem to reach 100%. E.g. for 36 months loans from Q3 2014 the displayed value is 91.23%. Does that mean that investors investing at that time incurred losses or how is that graph to be read?

This chart is only reflective of loans that have matured, because it shows the % of the original investment amount which has been paid back. If the loan period has matured and the % is less than 100, this does not necessarily mean that the investor’s portfolio return is negative. Typically, most portfolios are made up of a range of different loan durations from different cohorts. For example, there were very few loans issued in Q3 of 2014 with a 36-month duration – meaning this is not reflective of an investor’s full portfolio composition. We publish this graph simply to give full transparency and visualize information on the data we publish in our public reports.

Looking forward, do you expect default levels to rise on your consumer loans in Spain, Finland and Estonia in the remaining months of 2020 and 2021 as a result of the economic fallout of the COVID-19 crisis?

So far, our portfolio data does not suggest a trend of rising defaults. Again, this is why we made the decision to reduce our originations throughout the crisis period (as a precautionary measure).

How do you see the development of regulation on a European level?

My opinion is that although events this year with other smaller platforms have cast a negative light on the industry, there is a silver lining. Events like this can offer trigger expedited financial regulation due to the need for some form of consumer protection being brought into the public eye. We have always been in favour of pan-European regulation for P2P lending, and continue to work with regulators in support of this.

Yes, we have been profitable for three years. We recently released our financial results for 2019 and announced a net profit of €2.3M.

What plans does Bondora have for the next year?

This year, we’ve already spent a lot of time working on building automation for internal systems and customer facing parts of the product. For example, we just released an instant-answer support site which we’re still improving (this will eventually be localized into 24 languages). We’re continuing to work on automation as a priority this year. Reason being, once the world economy stabilizes and we are ready to target growth again, we’ll be able to scale quite rapidly without any dependencies on manual processes.

Final note – Thank you to all of our investors who have continued to support us over the years. We are looking forward to when the world is back to normal and we can welcome you in our office again. Stop by if you are ever in Tallinn 🙂

Not only the stock markets, but also the p2p lending sector is heavily impacted by the current coronavirus situation. In this article I’ll try to give an overview of what’s currently the situation.

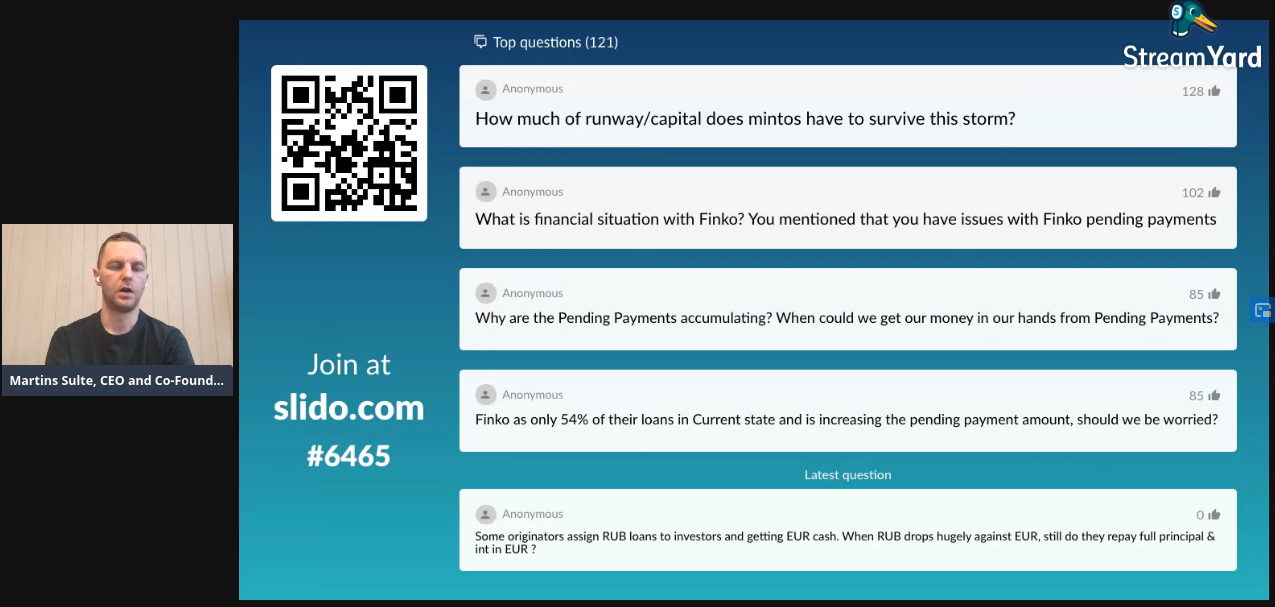

I watched the Mintos* live webinar on the current situation for the past 90 minutes. Some screenshots of the slides shown are at the end of this post. About 800-900 Mintos investors were watching and I think they highly appreciated the time and effort Mintos took to communicate. CEO Martins Sulte spent over 45 minutes answering questions. And there are a lot of questions investors have in times like these.

My take is, that the biggest trend we saw in p2p lending in the past week is the hunger for liquidity. Both on the investor side as on the loan originator side (on those marketplaces that work with loan originators).

105 German investors participated in a poll I ran over the past two days. Of these

11% say they increase their p2p lending investment, to buy and profit from loans that are available at (large) discounts on secondary markets

3% say they are increasing their p2p lending investment for other reasons

30% reinvest as usual

26% are withdrawing money as the want to reallocate it to the stock money

20% are withdrawing money as they think the risk is too high

So even in this small, non-representative poll nearly half the investors are saying they are withdrawing money.

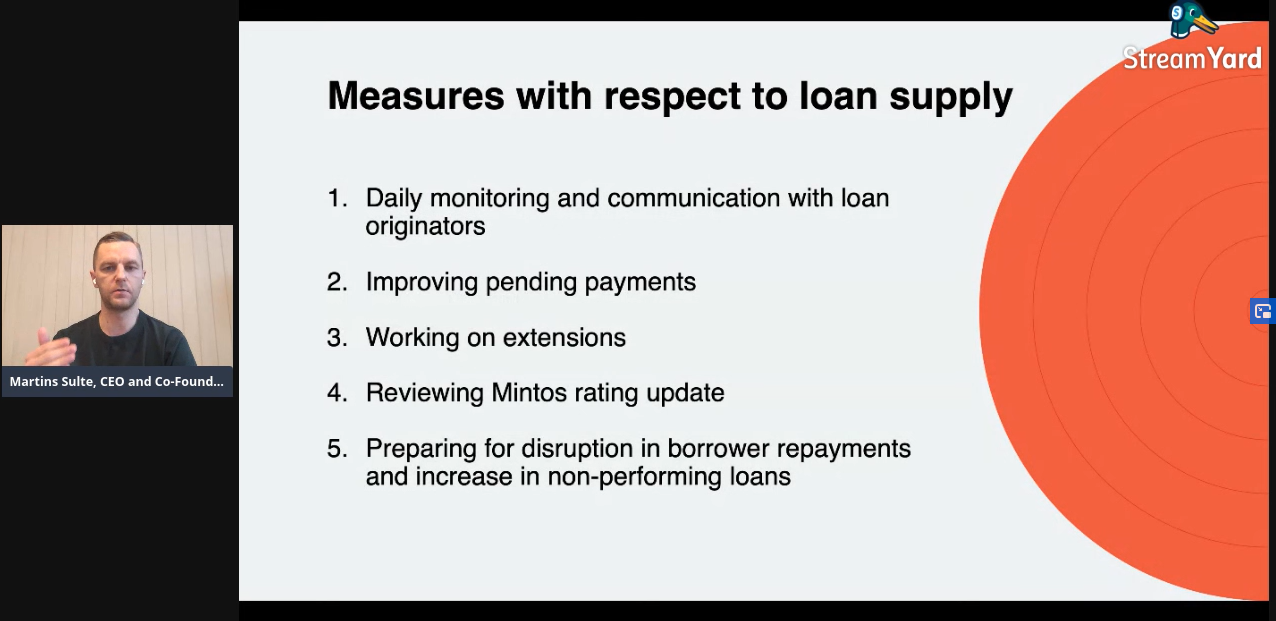

How that impacts the p2p lending marketplaces can be observed exemplarily on Mintos* :

loans on offer rose and still rise sharply both on the primary market (900,000 loans) and on the secondary market (1.7 million loans)

as many investors scramble to exit, this is only possible for them if they offer extreme discounts on the secondary market (the highest discount for current loans on offer is currently -20.1%, resulting in YTMs of 30% and higher for the buyer)

The volume of newly financed loans on the primary market has tanked

Interest rates offered on the primary market rise (current maximum 21.1%, Mintos even had to adapt the range the slider in the UI could show), together with cashbacks on offer and there are also measures to tie in capital longer.

In the current situation most investors in the discussion seem to assume that elevated risks come by the potential inability of borrowers to repay the loans, due to economic downturn. That may well be, but would impact the yield mid- or long-term (weeks or months). In my view there are two very short-term risks that many investors overlook:

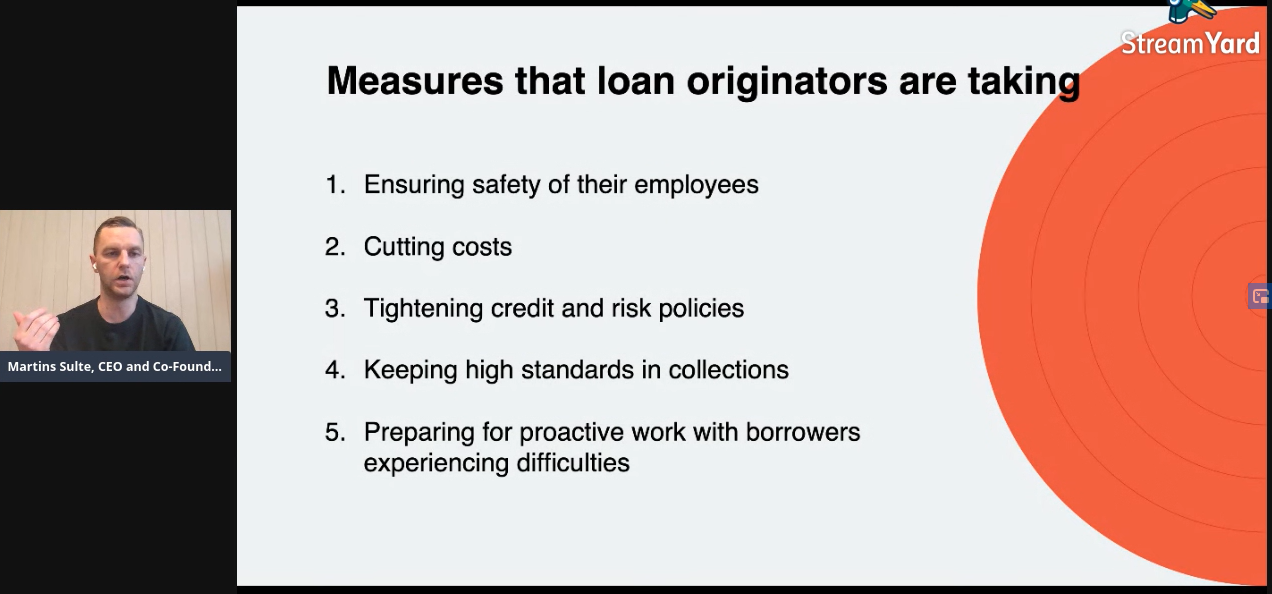

The currency risks for many Mintos loan originators: Many have issued loans to borrowers in weak currencies like RUB, KZT or GEL, but need to pay Mintos investors in EUR. The sharp change in exchange rates could pose major problems for the liquidity of the loan originators.

Many loan originators were growing fast and required constant cashflow to finance their lending and operations as they were not yet profitable. Some were even leveraged. External refinancing might be very hard to impossible to obtain in current market conditions (see for example investors reaction on trading of the Mogo Finance bond). And as said the volume financed on Mintos primary market is slowing. Again this could pose liquidity problems to originators.

An industry insider I spoke to said he would expect at least 2-3 loan originators to fail short term. CEO Sulte acknowledged in answering the questions on the webinar that “not all” could be expected to make it in the current situation, pointing to the large number of loan originators active on Mintos.

The two cited short term problems are especially a concern on those p2p lending market places that operate with loan originators. Of course the investors are also withdrawing increased amounts on “classic” p2p lending marketplaces like Assetz Capital, Bondora, Ratesetter and Zopa, but this poses no short-term risks to the stability of these marketplaces in my view.

Other investors share this opinion, pointing to the different levels of discounts on different secondary market (for current loans: Mintos* -20.1%, Viventor* -6%, Iuvo* -5.7%, Finbee* -5%, Savy* -5%, Neofinance* -5%, Bondora* -3%)

The platforms have reacted by four ways: communication, temporarily suspending borrower repayment requirement (especially SME loans, e.g. Linked Finance, October, Neofinance* ), and stepping up marketing and increasing interest rates:

Bondora* runs a raffle for investors which can win a BMW, minimum investment 1 EUR required.

Lendermarket* has increased interest rates from 12 to 14% and offers 2% cashback for any investment increase

European p2p lending services are growing. And yields of 10+% are achievable on some of the platforms. This attracts international investors. But if you are a US resident, you may have made the experience that you cannot register on some marketplaces. This is mainly due to KYC (know-your-customer) and AML (anti-money-laundering) requirements, which get more complicated if the client is outside Europe.

I have asked many of the European p2p lending marketplaces, whether they accecpt US residents and US companies as investors.

Here is an overview of 5 services (sorted aplphabetically) that do allow US investors. I have not provided a review for each of the service as the article would have gotten too long, but you can easily find news and reviews by entering the company name into the search box on the upper right of this blog.

On some platforms you need a bank account in the European Union. In most cases Transferwise* borderless or Revolut* will help (while technically e-money accounts, they function pretty similar to bank accounts) and do not charge any monthly fees. They are both very useful for currency conversion (Revolut is better). On Assetz Capital the currency is GBP. On the other marketplaces it is EUR. Mintos has additional currencies. Transferwise borderless is available in all US states except Hawaii and Nevada. Revolut* is currently rolling out the service in the US.

Mentioned new customer cashbacks were correct at the time of the publication of this article. If you are reading the article at a later time, it may have changed. A current list of cashback offers is here.

Assetz Capital

Assetz Capital* is a marketplace for UK SME and property development loans. The liquid ‘access’ products offer 4.1% to 5.75% interest. Other product types offer higher rates. US investors are welcome. UK bank is account required – see notes above. US companies are eligible, but verification might take longer than for individuals. Expect 1-10 days for company registration.

Assetz Capital cashback for new investors: 50-250 GBP (dependent on investment amount; minimum 1000 GBP). To get it just register using this link: Assetz Capital registration and start lending

Bondora

Bondora* is an Estonian p2p lending marketplace for consumer loans. The highly liquid Go&Grow product offer yields 6.75%. With other products higher yields of 10+% are achievable. US investors need to be accredited investors to use Bondora. A bank account in the European Union is not necessary. US companies are eligible to invest. Bondora recommends that interested US investors and companies contact them at investor@bondora.com or by phone at +44 1568 6300 06 (during business hours, Mo-Fr: 9–17 EET) to check eligibility and clear any questions concerning registration.

Bondora cashback for new investors: 5 EUR, to get it just register using this link: Bondora registration and start lending

Estateguru

Estateguru* is an Estonian marketplace for property loans. Typical interest rates are 10-12%. US residents are eligible, if they have a bank account in the EEA (European Economic Area) – see notes above. US companies can invest, if they have a bank account in the EEA.

Estateguru cashback for new investors: 0.5% (1% in October) cashback on all investments in the first 3 months. To get it just register using this link: Estateguru registration and start lending

Flender

Flender* is an Irish marketplace for SME loans. Typical interest rates are around 10%. US investors and US companies are eligible.

Flender cashback for new investors: 5% on all investments in the first 30 days after signup. Register using this link Flender registration and start lending

Mintos

Mintos* is a Latvian p2p lending market place. A wide range of loan types is offered. The fairly liquid ‘Invest&Access’ product currently promotes around 8% rate. Yields of 10+% are possible with manual and autoinvest.

US investors and US companies are welcome. A bank account in the EEA (European Economic Area is required) – see notes above.

Mintos cashback for new investors: 1% cashback on all investments in the first 90 days. To get it just register using this link: Mintos registration and start lending

The article was updated on Nov. 21st as Estateguru has meanwhile changed its position saying that Revolut or Transferwise are sufficient now to satisfy the requirements on a bank account in the European Union.

P2P lending bears high risks, including total loss of investment. This article is not investment advice.

Mintos* will launch a new product offer called Invest & Access tomorrow. It was already unveiled and presented at the P2P Conference in Riga on Friday. Before I write about it watch the video below for about 10 minutes with Mintos CEO Martins Sulte explaining Mintos Invest and Access.

the video should autostart at the right point. If not it is at 2:29:22

The new offer makes it super-easy for investors to invest and automatically diversify through a very wide selection of loans. Mintos does that by investing the money in all loans on the platform that carry a buyback guarantee and are from originators that are at least 6 months on the platform. Mintos promises that investors will be able to cash out easily (subject to market demand) instantly, saying investors don’t need to bother about handling the loan selling on the seondary market. Mintos does that by selling the non-late loans to other investors.

The investor can still see how the portfolio he holds is composed on an overview page. One important aspect for the market dynamics on Mintos marketplace is that Invest & Access will invest before the autoinvests.

Mintos is cleary aiming to make it easy for new investors that don’t want to spend much time thinking about the investment and optmizing yields by giving them the average yield by just one click. The Invest & Acesss page will show the weighted average interest rate, which at the time I saw that page was showed as 11.98%. But the figure will change and update as market conditions fluctate and as the FAQ says it is not guaranteed.

One important point in the FAQ/footnotes is that the ‘instant access’ only applies to current loans. That means if the investors has e.g. 15% late loans, that would mean that he gets only 85% as instant withdrawal and for the remaining 15% has to wait until either the loan is bought back by the buyback or becomes current again (I suppose in that case the investor could trigger another cashout).

Investors can runs both Mintos Invest & Access as well as the existing autoinvests, should they which, but in that case Invest & Access would use any available cash the investor has first, therefore I would guess that there are rarely any funds left for the autoinvests to use.

My Opinion on Mintos Invest and Access

Mintos clearly offers a product that makes it as easy as possible, lowering the entry hurdles especially for new investors. And as Bondora Go&Grow* shows there is a high demand by investors for simplified products. Statistics published by Bondora show that in April 2019 63% of the new investments in that month where conducted via the Go&Grow product, which is constantly gaining over the other investment methods Bondora offers. Other examples are the Access products offered by British Assetz Capital*.

Looking at it from the perspective of an investor that is a little more experienced and willing to spend a little time Invest & Access does not seem an attractive offer. By definition it offers the weighted average interest rate.

By setting up own autoinvests at Mintos, keeping a good diversification and foregoing the highest risk, investors can currently achieve about 13-14% yield on Mintos. So if they would instead use the new product they would have about 2-3% lower yield, and have actually less control on which originators they invest in. An important point to consider, is that the value Mintos shows you, is the average interest rate, NOT the expected average yield. The yield will be significantly lower than the interest rate as Mintos will include buyback loans from originators with long grace periods or originators that do not pay interest income on delayed payment. Excatly those are typically avoided when investors configure their own autoinvests.

And concerning the argument of liquidity. Mintos is very liquid anyway. Without using the new product it is no problem to liquidate a portfolio within a few minutes to a few hours it just depends on the price. Sure you might have to offer a discount. Maybe depending 0.2%-0.6% on average. But that is a small price if you had the higher yields before.

So would I recommend using Invest & Access over the ‘traditional’ way of setting up own autoinvest? There is one use-case I would. If an investor wants to invest very short-time (for whatever reason ‘parking’ money) for less than say 120 days, than it is worth considering.

In my opinion on why Mintos launched the new product, there are actually two reasons:

there is demand for a simplified product and this new product shall satisfy that

the new product will help on the sales site for attracting and onboarding new orignators. Originators that can only offer rates that are below the average interest rate on the Mintos platform so far were hard to sell. With Invest & Access they will be just part of the bundle and automatically sold (once the originator has been on the platform 6 month)

That brings us to an interesting point. How will Mintos Invest & Access the market dynamics? The big factor here is that Mintos Invest & Access happens BEFORE autoinvest and manual investment. There are already (even before launch) speculations and fears of investors that it might bring down interest rates or ‘force’ them to use the new product to avoid cash drag, but I think it is much to early to make any prediction what might be the outcome. But I sure am curious what this will do to the activity on the Mintos marketplace.

What are your opinions on the new product? Please share them in the comments. Thx.

P.S.: The following interview with the Mintos CEO was recorded just before the announcement of the new product, therefore it does not cover Invest and Access – but it has a lot of information on the current state of Mintos.