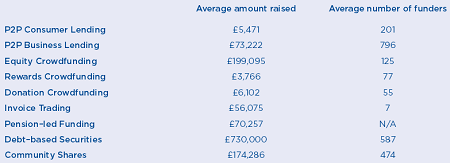

Today the Nesta Study ‘Understanding Alternative Finance – The UK Alternative Finance Industry Report‘ was released. The researchers Peter Baeck, Liam Collins and Bryan Zhang worked in four stages to compile this great report. One included questioning more than 15,000 users with the help of the platforms in distributing the surveys. Furthermore to gauge awareness of the general public for alternative finance 2,007 consumers and 506 SMEs were questioned.

The more than 90 page report documents and visualizes the fast ongoing growth of all alternative finance sectors in the UK and the positive reception by the users. I will conclude by citing some graphs from the study to induce everybody interested in p2p lending and alternative finance to read the full study.

At the moment there is not only one but two open pitches from UK crowdfunding/fintech startups raising money in exchange for equity at Seedrs. I invested small amounts in both of them and will become a shareholder when the pitches successfully close.

Crowdlords

Crowdlords is a pre-launch two-sided, residential buy-to let crowdfunding platform that wants to bring together landlords and investors.

Landlords who are fully vetted, would identify the properties and be required to invest a minimum amount themselves – the balance is sourced from Investors. Each property would be held in a Special Purpose Vehicle (SPV) with the shareholdings in each SPV split between the Landlord and the Investors.

Investors would be able to select from a range of properties and investments. Investors would gain returns from ongoing underlying rental income and a proportionate share of sale proceeds when the property is sold. Investors could invest fairly modest sums with a minimum investment of 1,000 GBP.

Crowdlords is pitching for 90,000 GBP offering 10% equity (810,000 GBP pre-money valuation). The pitch is currntly 83% filled.

Trillion Fund

Trillion Fund is a crowdfunding platform that raises money for environmental and social projects from ordinary people who want better returns.

Trillion focuses on loan based crowdfunding in green energy and social investment, and earns a percentage of funds raised, paid by borrowers, and an annual percentage of funds lent, paid by the lenders.

Using profit as motivation Trillion aims to re-engage consumers with their money and help them make a profit and make a difference. Trillion effectively operates a two sided network, bringing together people with money and those who need it.

Trillion claims that the recent merger with Buzzbnk has made it one of the largest social crowdfunding business in the UK.

The pitch seeks to raise 500,000 GBP in exchange for 7.7% equity (6M GBP pre-money valuation). The pitch just started and is currently 2.7% filled. Continue reading →

October was overall a good month for p2p lending services. Especially Zopa did grow and closed a bit of the gap to the 2 other UK p2p marketplaces . Prosper reached a total volume of 2 billion US$ originated since inception. I added one more service. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in October 2014. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations.

Notice to p2p lending services not listed: If you want to be included in this chart in future, please email the following figures on the first working day of a month: total loan volume originated since inception, loan volume originated in previous month, number of loans originated in previous month, average nominal interest rate of loans originated in previous month.

Seedrs, a UK crowdinvestment platform, has announced that it acquired California based Junction Investments. Seedrs plans to use this acquisition to expand to the United States in early 2015. Junction’s co-founders, Adam Kaufman and Brian Goldsmith, are now Co-Heads of Seedrs America, and they will be leading this expansion.

Seedrs was already open to international investors and startups, but so far the focus was clearly on the UK and Europe.

Seedrs on building a global platform: ‘A founding principle of Seedrs is that investment in startups and growth businesses should be global. We believe in a future where entrepreneurs and investors from all over the world can connect online. Investors should be able to discover and invest in opportunities anywhere, and entrepreneurs should be able to access capital worldwide.

Financial regulation remains largely national or regional, however, and compliance with applicable law has always been a non-negotiable element of Seedrs’s approach to business. Building a global platform is thus a multi-stage process that involves identifying the right approaches and partners in different jurisdictions.

Having opened across Europe at the end of 2013, we began to look at the U.S. market at the beginning of this year. The U.S. has been slower to embrace equity crowdfunding than the UK and Europe have, and full-scale crowdfunding is not yet possible there. But with the opening of online investment to accredited investors at the end of last year (under Title II of the JOBS Act), and the prospect of wider crowdfunding on the horizon (under the yet-to-be-implemented Title III of the JOBS Act, or an amended version thereof), we feel that now is the right time to begin building our U.S. presence.’

My take: This is one of the first international mergers in the equity crowdfunding space. It will be interesting to see if and how other players do on taking internationalisation beyond Europe.

LoanBook Capital is a Spanish peer-to-business (P2B) finance platform, providing an alternative to traditional savings and fixed income products to investors of all types via direct participation in loans, and other forms of credit finance, to mature, good quality Spanish SMEs.

LoanBook provides credit origination and management services to clients. These services are supported by an online platform, which gives investors access to credit opportunities through an auction marketplace, as well as a soon to be launched secondary market for trading loan participations.

What are the three main advantages for investors?

As with other P2B platforms, the main attractions for investors of this model are typically greater risk adjusted returns, control and transparency over investments and lower fees. LoanBook is no different in these characteristics: we provide access to an asset class that offers a return that exceeds that available from traditional fixed income investments with comparable characteristics (e.g. risk and liquidity), we allow investors to manage the risk and return profile of their portfolio online in a transparent way, and we do not charge fees to investors, other than for providing liquidity through our secondary market.

As with advantages to investors, LoanBook offers the borrower the typical advantages that you would expect from a P2B platform; competitive and transparent cost of capital (interest rates & fees), access to an alternative channel of finance and a quick and easy application process.

How did you start Loanbook Capital? Is the company funded with venture capital?

LoanBook was started at the end of 2012 by two founding partners with their own capital and initiative. The company’s shareholder base has moved on somewhat since then, with each of the three-man management team, and a number of the employees, having an ownership stake in the company. Continue reading →