In March Lendinvest reported a surge in loan originations and had an exceptional month with more volume originated than Ratesetter or Funding Circle. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in March 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month

This is a guest post by Roman Feranec, CEO of Žltý melón (full bio at the end of the article)

Slovakia is an Eastern European country with 5.5 million inhabitants. The country borders with Poland, Czech Republic, Hungary and Ukraine. Regarding its real GDP per capita exceeding 10 thousand EUR, it is one of the most developed countries in eastern European region. Slovakia is a NATO and EU member and in 2009 the country joined Eurozone and started using EURO as its currency.

Peer to peer lending, also known as Marketplace lending, started in Slovakia at the end of 2012. In just two years of operation it proved that it could be an interesting financial alternative with valuable benefits for people in need of money, as well as for people looking for a stable and good appreciation of their savings. This all despite the fact that Slovaks are generally more conservative than their peers in western countries and banks in Slovakia were almost no hit by the recent financial crises.

The Slovak market of unsecured consumer lending reaches a volume of approximately 150 million EUR in new loans every month. There is a big competition between 12 retail banks keeping the average interest rate at about 14 % p.a. P2P loans at the moment represent just a tiny fraction of the market with 0.1 % market share. This can also show a huge growth potential for this alternative.

The first and so far the only domestic P2P loans provider is called Žltý melón. The company was set up by a team of people with long-term experience in banking and financial industry. Žltý melón was launched at the end of 2012 and since then it has provided about 2 million EUR of loans with current volumes of 160 – 200 thousand EUR of new loans per month. It provides ordinary unsecured retail consumer loans – purpose or non-purpose. Recently it has also introduced loans for financing real estates with a guarantee for investors covered by real estate and also company guarantee of major development company. The new product is one of the outcomes of a bigger partnership between Žltý melón and local leading residential developer Cresco Group. Continue reading →

Funding Empire entered a cooperation with the Business Lending Exchange (BLX) to offer asset backed loans on the marketplace. These new asset backed loan investments will be backed by realisable security and go through BLX’s proven and experienced credit assessment process – they will be available to FundingEmpire investors from tomorrow.

Parag Patel is managing director of FundingEmpire, a growing peer-to-peer business lending platform. Announcing the new product, he said: ‘This is the first step in an ambitious plan to deliver a number of different peer-to-peer investment products that we have designed to cater for all kinds of investors and their varying risk profiles. Asset finance offers funding for businesses and is a long established traditional finance product backed by tangible security. In this new model our lenders will receive monthly capital and interest repayments, unlike many other asset backed lending repayment structures that defer payment of capital and sometimes also interest, until the end of the loan term. We have had huge demand for a non-property based, asset backed product that provides monthly income – and we’ve responded to that demand.‘

Loans under this model will be for a maximum of 50,000 GBP over a maximum term of 3 years providing monthly capital and interest repayments to lenders. Loan requests will typically last between 5-7 days and will operate as fixed rate auctions. They will end either when the loan request is filled or it expires. Loan parts from this model can be traded as normal on our secondary loan market. Continue reading →

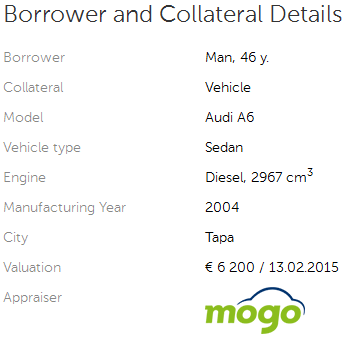

Today Latvian Mintos expanded by now offering loans to Estonian borrowers on the p2p lending marketplace. These loans are secured with a car as collateral. Today 15 loans were posted on the platform. Typical (nominal) interest rates for these loans seem to be between 11 and 13%. LTVs are as of today in a wide range from 26% to 90%.

CEO MÄrtiņš Å ulte told P2P-Banking.com: ‘From today we also offer investors opportunity to invest in loans secured by vehicle. We provide these loans in cooperation with Mogo (http://mogofinance.com), the market leader in car loans with operations in Latvia, Lithuania, Estonia, and Georgia. … as part of our international expansion we have set up a company in Estonia and are working on entering Lithuania and Poland to boost our loan origination capacity‘. Continue reading →

German p2p lending service Lendico today added SME loans to its marketplace which previously focussed on consumer loans. This is in my view a peculiar move as now Lendico poaches in the realm of Zencap, which is already focussed on SME loans, considering that both startups were backed by Rocket Internet. Continue reading →