The way bidding works at p2p lending service Ratesetter will change on June 24th. Ratesetter informed investors

Currently your money is re-invested at the higher of “Your Rate†(i.e. the rate you have specified) or “Market Rate†(i.e. the rate that is worked out daily at RateSetter looking at the whole market). Once re-set to Market Rate it stays at that rate which resulted in some scenarios where your money could be sitting at Market Rate unmatched when in actual fact your specified rate was lower.

From 24th June, your money will simply be put on the market to be re-invested at your specified rate. Simple as that.

It is worth saying that if the highest borrower bid at the time of your re-investment is higher than your specified rate, your money will be matched at that rate.

So, we hope that you can now use the “Your Rate†functionality to better control the rate at which you re-invest. One way of looking at it is that is like a floor – you will get at least your rate, or the best borrower bid if that is higher.

There has been some discussion among investors what this means and what actually changes for investors. The way I interpret it (but I am not even a Ratesetter investor) is that the market rate will become less important as Ratesetter could advice the borrower at what rate his loan request would match instantly. Since many investors will not micro-manage their set rate and only login occasionally it will lead to a broader distribution of interest rates set as ‘Your Rate’ and thereby reduce volatility. E.g. should interest rates move upward on the market (for whatever reason), unchanged ‘Your Rates’ at lower levels from earlier times will delay and slow the rise (provided they have unused cash from repayments in their accounts). But let’s hear opinion of actual Ratesetter investors in the comments, please!

When German p2p lending startup Finmar tried to register their logo as a trademark they were in for a negative surprise. The trademark office in 2014 forwarded them a 500 page objection filed by the FINRA (Financial Industry Regulatory Authority) which complained that the design of Finmar’s logo to closely resembled FINRA’s logo which was already protected by a European trademark filed in Madrid. Given the similarity of name and logo FINRA feared that there is a risk that both are confused.

Finmar was flabbergasted but tried to reduce the damage. They negotiated with FINRA that Finmar would change its logo but could keep its name. Finmar designed a new logo (see above), revoked the old trademark application, submitted a new one and exchanged the logo on the website and in all social media channels. In total this dispute took Finmar more than 15 months to settle.

Swedish crowdfunding marketplace Fundedbyme today announces that its partner Alix Global Sdn Bhd, was awarded one of six coveted licenses to operate equity crowdfunding in Malaysia. Malaysia is the first South-East Asia country offering equity crowdfunding licenses. The license allows FundedByMe to start operations in the new market.

The announcement follows careful deliberations by the Malaysian Securities Commission, which closed submissions for licenses in May 2015. The license comes under Section 34 of the Capital Markets and Services Act (2007), by the Malaysian Securities Commission. It will permit the selected platforms to help privately owned businesses raise money from a spectrum of investors – including institutional, accredited, and retail investors – with limitations placed on non-accredited investors.

“We’re extremely excited to be one of the few platforms selected by the Malaysian Securities Commission today, which is a first for the region, and marks a historic moment for Malaysia and the crowdfunding industry. As a business-building crowdfunding platform, we together with our partners Alix Global are thrilled to help build this fast-growing industry of which empowers businesses through crowdfunding,†said Daniel Daboczy, CEO and Co-Founder of FundedByMe. Continue reading →

When was the last time you stood in a long line outside your bank branch, patiently waiting to deposit money into your savings account? Imagining a scene like that seems ridiculous at a time with near-zero interest rates in an increasingly large number of developed countries.

But there where you would least expect it, in the Fintech world of fast-moving bits, some startups actually are imposing measures to throttle influx of investor money in order to balance it with borrower demand. Welcome to p2p lending (short for peer-to-peer lending). The sector is experiencing tremendous growth rates. With attractive yields for investors some platforms struggle to acquire new borrowers fast enough for loan demand to match the ever-rising available investor demand.

One challenging factor is deeply ingrained in the business model of p2p lending marketplaces: once a new investor is onboarded and found the product satisfactory, he is most likely to stay a customer for years to come and reinvest repayments received and maybe the interest also. On the other hand the majority of borrowers are one-time customers. They take out a loan typically just once. While it may take years for the borrower to repay that loan, in most instances there is no repeat business for the marketplaces. So the marketplaces have to constantly fire on all marketing cylinders to win new borrowers in order to keep up and grow loan origination volume.

This has sparked some outside of the box thinking, e.g. the partnership of Ratesetter with CommuterClub to win their loan volume, which is in fact mostly repeat business.

Winning investors has been relatively easy for many of the p2p lending services in the recent past. Investors are attracted typically through press articles or word of mouth. One UK CEO told me he never spent a marketing penny ever to acquire investors.

But what happens on the marketplace, when there are so many investors waiting to invest their money in loans, but loans are in short supply?

If the marketplace does nothing or little to steer it, then those investors that react the fastest, when new loans are available, will be able to bid and invest their money. This is the situation e.g. on Prosper, Lending Club and Saving Stream.

The marketplace has some kind of queuing mechanism. This is typically coupled with an auto-bid functionality. Examples of this are Zopa, Ratesetter and Bondora.

The investors are competing during an auction period by underbidding each other through lower interest rates. Examples of p2p lending services with this model are Funding Circle, Rebuilding Society and Investly.

The marketplace can lower overall interest rates to attract more borrowers while the resulting lower yields slow investor money influx.

The UK p2p lending sector is eagerly awaiting the sector to become eligible for the new ISA wrapper. Inclusion into the popular tax-efficient wrapper will attract an avalanche of new investor money to the platforms.

“That’s going to be a challenge for the industry,†said Giles Andrews, CEO of Zopa. “Once the dates are worked out, the industry will need to plan for that together, and we may have to do something we have never done before, which is to limit the supply of money. It’s not good to have people’s money lying around [awaiting new borrowers] or to lower standards of borrowers.â€[1]

So there is some speculation that UK p2p lending services could impose temporary limits on new investments.

The investor viewpoint

The aim of the investor is to lend the deposited money easy and speedy into those loans that match his selected criteria/risk appetite. Idle cash earns no interest and will impact yields achieved (aka cash drag).

For the retail investor none of the above mentioned mechanisms are ideal. The “fastest bidder wins†scenario means he would either have to sit in front of the computer most of the time or be lucky to be logged in just as new loans arrive. The queuing mechanisms are disliked as they can prove to be very slow in lending out the funds and can be perceived as nontransparent (see the lengthy and numerous forum discussions on the Zopa queuing mechanism). Underbidding in auctions does provide the chance to lend fast, but at the risk of setting the interest rate too low and this requires a strategy and can also be time consuming.Continue reading →

The following table lists the loan originations for May. The top four UK services volumes are close together, with Wellesley catching up. I added two new platforms. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in May 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month

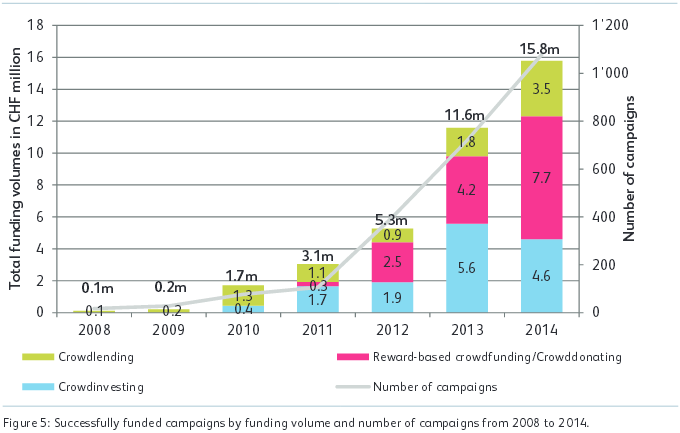

Prof. Dr. Andreas Dietrich of the Lucerne University of Applied Sciences and Arts, Simon Amrein, Reto Wernli and Dr. Falk Kohlmann have published the study ‘Crowdfunding Monitoring Switzerland 2015‘. It analyses the development of crowdfunding in Switzerland giving special attention to the development of p2p lending.

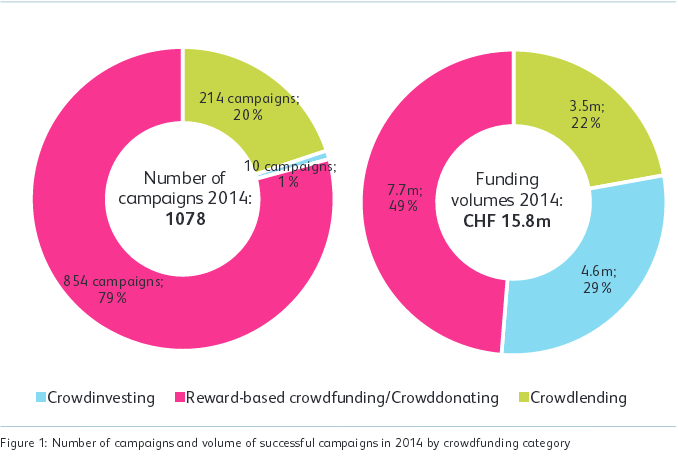

The Swiss market is growing fast; albeit on low absolute numbers compared to other European countries. The market is in a very early development stage. As the following chart shows the volume is mainly generated by crowdsupporting/crowddonating.

Source: Crowdfunding Monitoring Switzerland 2015 study

The total market for new loans to consumers in Switzerland in 2014 was 3.9 billion CHF. Via p2p lending 3.5 million CHF were originated in 2014, so that equals a market share of only 0.1%. But the p2p lending volume has nearly doubled compared to 2013 (1.8 million CHF). The authors state:

The crowdlending market has experienced the strongest year-on-year growth of all crowdfunding segments. … The number of campaigns rose from 116 to 214, and all of them were successfully funded. The current challenge of crowdlending platforms is not finding funders. On the contrary, it is (more) difficult to get borrowers on the platforms. Crowdlending campaign funders invested an average of CHF 1,100, which is substantially different from the figures in reward-based crowdfunding & crowddonating as well as in crowdinvesting. The average campaign amount was CHF 16,200, which was slightly higher than in the past year (CHF 15,000). The average loan amount in crowdlending is very similar to the average consumer loan as of the end of 2014. The crowdlending market is, however, still niche market.

Source: Crowdfunding Monitoring Switzerland 2015 study

Regulation limits that a private consumer loan cannot be financed by more than 20 different individual lenders.

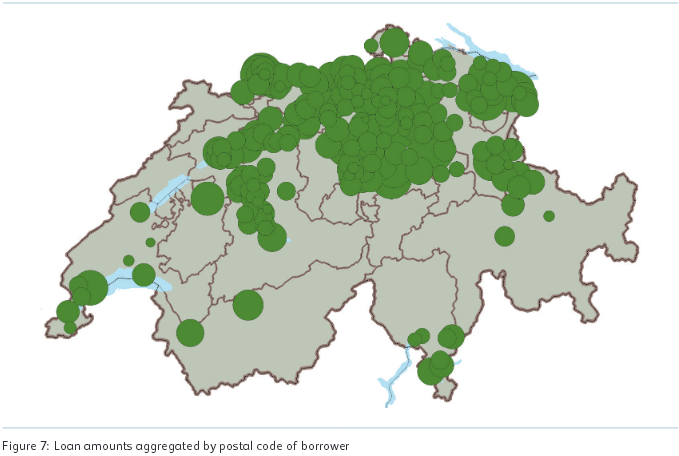

The authors analysed loan data of the Cashare marketplace. Examining who uses p2p lending as a borrower the study finds:

The average borrower age is 38. One fifth had at least one child under the age of 16 at the time the loan was raised. At 37 percent, married people were proportionally under-represented, although they make up 54 percent of the permanent resident population. 19 Homeowners (19 percent) and women (24 percent) are also under-represented. The distribution of nationalities is slightly more representative of the Swiss population. 71 percent of the borrowers were Swiss, while 29 percent of the borrowers were not in possession of a Swiss passport. The average proportion of the foreign-born resident population in Switzerland was 22 percent between 2008 and 2013. The age distribution of the borrowers leads to the conclusion that crowdlending is currently still primarily used by the tech-savvy Generation Y. 60 percent of all loans raised since 2008 went to people under the age of 40. Only 4 percent of the borrowers for successful projects were over 60 years of age.

Also the borrowers regional distribution shows that use is much more common in the German speaking areas of Switzerland.

Source: Crowdfunding Monitoring Switzerland 2015 study