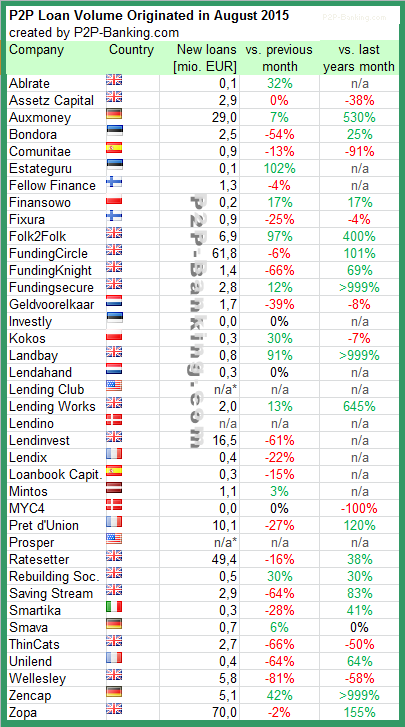

The following table lists the loan originations for August. August was a slow month for many of the listed services probably due to the holiday season. Zopa crossed 1 billion GBP lent since inception (see infographic) and Giles Andrews stated he expects the next billion to be lent in 2016. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in August 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

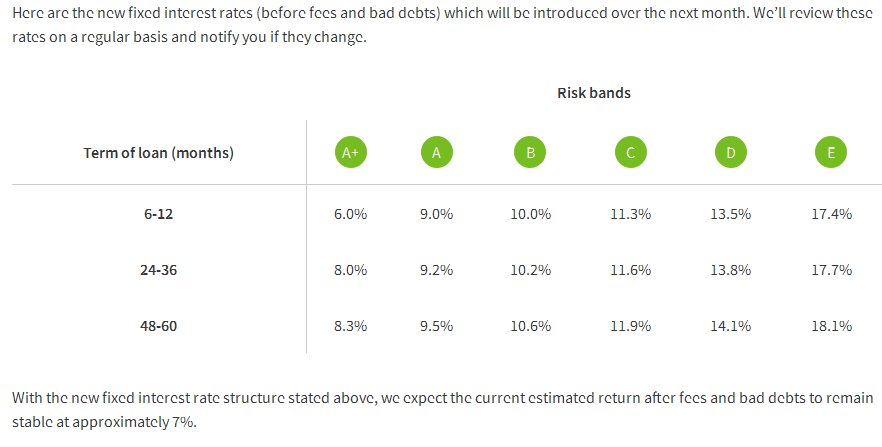

British p2p lending marketplace Funding Circle introduces a new model today. All new loans will be issued at fixed interest rates set by Funding Circle. Coming right after Funding Circle’s fifth anniversary, and 792 million GBP originated in loans to SMEs, the step to discontinue auctions is a major change in the way the marketplace operates.

Spokesman David de Koning told P2P-Banking.com that there were major drawbacks associated with the auction model for borrowers as well as lenders. Borrowers lacked certainty of the final interest rate until the auction period was over which led to some of them cancelling their loan application. Investors on the other hand experienced cash drag and sometimes had to make multiple bids to ensure they participate in the loan they wanted.

Under the new model Funding Circle will set the interest rate based on risk band and loan term. There will be 3 different rates for each risk bank. De Koning pointed out that the introduced model is not completly new for Funding Circle, as Funding Circle did already use fixed rates on property loans and on the US market of Funding Circle. Asked whether he expects loans to close instantly as demand could be higher than loan supply, he said he could certainly see loans to close quicker than before. The long term goal envisioned is that in future borrowers may pre-approve a loan before it is listed and it could close instantly once filled. Continue reading →

Zencap will receive 230M EUR in investments from Victory Park Capital over a three year period, under an exclusive agreement. Vivtory Park Capital, an asset management firm focused on middle market debt and equity investments, will invest the amount into SME loans originated on the p2p lending marketplace Zencap. The partners are teaming up to provide small and medium-sized enterprises (SMEs) in Germany, Netherlands and Spain with efficient, fast and easy access to capital. Zencap allows SMEs to apply for loans between 5.000 and 250.000 EUR.

Under the terms of the preferred partnership agreement, VPC will be the largest institutional investor on the P2P platform and has secured a credit facility from a leading global bank to leverage Zencap loans at favorable rates. The transaction represents the largest commitment to an online lending platform in Continental Europe and underlines the increasing importance of the sector.

“We are impressed with the Zencap team’s ability to execute an ambitious strategy, and their results in the three countries they operate in give us confidence that this emerging platform is serving a critical market need,†said Gordon Watson, principal at Victory Park Capital. “With this additional lending facility, Zencap will be well positioned to continue to achieve substantial growth over the near term and firmly establish itself as a market leader in Continental Europe.â€

Matthias Knecht, co-founder and managing director of Zencap, added, ‘We are excited to announce this long-term, strategic partnership with VPC, the leading investor in the industry. This groundbreaking transaction will help to further accelerate our growth and support us in our mission to provide fast and seamless access to capital for small businesses in Europe.’

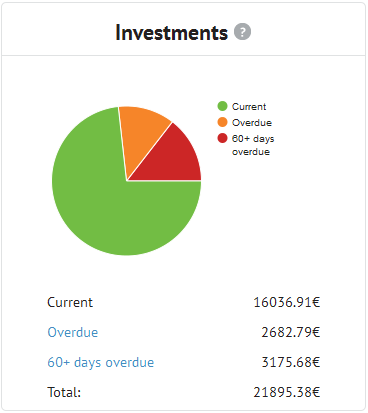

In October 2012 I started p2p lending at Bondora. Since then I periodically wrote on my experiences – you can read my last review published in April here. Since the start I did deposit 14,000 Euro (approx. 15,900 US$). My portfolio is very diversified. Most loan parts I hold are for loan terms between 36 and 60 months. Together the loans add up to 21,895 Euro outstanding principal. Loans in the value of 2,683 Euro are overdue, meaning they (partly) missed one or two repayments. 3,175 Euro principal is stuck in loans that are more than 60 days late. I already received 15,202 Euro in repaid principal back – this figure includes loans Bondora cancelled before payout. I reinvested all repayments.

Chart 1: Screenshot of loan status

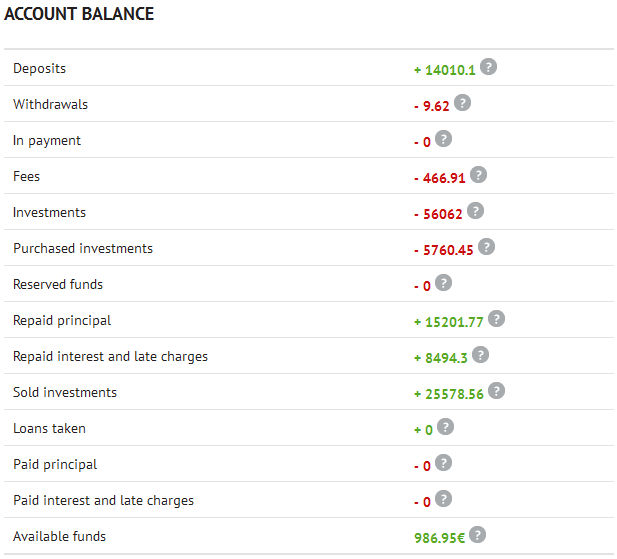

At the moment I have 0 Euro in bids in open market listings and 987 Euro cash available.

Chart 2: Screenshot of account balance

Return on Invest

Currently Isepankur shows my ROI to be 26.76%. In my own calculations, using XIRR in Excel, assuming that 30% of my 60+days overdue and 15% of my overdue loans will not be recovered, my ROI calculations result in 21.8%.Continue reading →

Today British p2p lending service Saving Stream introduced a new pre-funding option. This is essentially an autobid, which allows investors to bid on every new loan.

Investors have long complained that (smaller) loans were filling within minutes, were not (always) announced in advance and lately the demand caused the server to fail frequently when new loans were announced.

Here is what Saving Stream says about the new pre-funding model:

Rationale

We want to give as many people the chance to invest as possible so we will provide an option to buy in before the loan goes live up to a self-determined limit. We want the smaller investors to be guaranteed a position in every loan, and the deeper pocketed investors will also participate at the same amount as everyone else. If there is spare capacity, the larger investors will pick this up subject to their pre-set investment levels.

This will also help us know how much is potentially available to lend out. This has been a continual problem that we just don’t know the exact appetite for our loan products and thus limits the number of loans that we can make.

How pre-funding will work?

Set your limit to invest in each new loan. When a new loan becomes available, you will be guaranteed at least a portion of your investment amount if not all, depending on the loan size. You will be notified of your participation and are expected to follow up with a bank transfer, much in the same way as normal. You can sell your loan if you want.

For example  – you set your limit to £1k. There are 400 people who have the same limit and 40 with a limit of £10k. A loan of £1m is launched. All 440 people will get £1k (£400k total) and the 40 people with higher limits will get an additional £9k each in the surplus thus they get £10k in total. The remaining availability will go to the market and can be bought by whoever wants it.

It will become complicated when the loan is less than the amount in the Pre-Fund pot i.e £500k loan, 400 people with £1k, and 40 with £10k. Again, all 440 people will get £1k leaving £60k to divide by the 40 which is an additional £1.5k each, giving a total investment of £2.5k for those investors who set their limit higher.

Those investors with higher limits might be disappointed that they didn’t get their full allocation, but they should be happy that they have participated in an equitable distribution model which should assist with the growth and opportunities available. The next loan might be able to take all of their demand plus more.

You won’t be able to review the loan parts or valuation beforehand (yet) but the secondary market is incredibly liquid and we are confident of the ability to sell your position if required.

I expect that Saving Stream customers will widely use this new option. While it seems strange that this option excludes the possibility to review loan details before bidding, this has been essentially happening before already with loans gone in minutes. And the Saving Stream secondary market is very liquid, therefore it is usually not a problem to sell (unwanted) loan parts fast. Continue reading →

Laimonas Noreika is the CEO of Finbee, a p2p lending service that launched last week and is open to international investors starting today.

What is Finbee about?

FinBee is about borrowing for less and earning more when investing. We also are most user friendly p2p lending platform in Lithuania.

What are the three main advantages for investors?

Firstly, our loans have high interest rate – from 10 to 40 percent. That means, that investor can expect higher return of investment, compared to other p2p lending platforms. Secondly, we have reliable software, that is developed by UK based Madiston. That means, that it is tested and extremely user friendly from day one. And finally, we pay great attention to selection of borrowers, so that the risk for investors is minimized as much as possible. On top of that, we invest 10 percent on total sum into each and every loan, so we share the risk with investors. In the near future we also will introduce compensation fund that in an unlikely case of borrower defaulting on its loan will compensate lenders their investment.

What are the three main advantages for borrowers?

I would say that first and foremost, we offer cheaper loans than most of the players in Lithuanian market, including banks, payday loan companies and credit unions. This is achieved by implementing auction principle when borrowing. That means, that borrower can set interest rate ceiling, for example 15 percent. Lenders then are able to offer lower interest rate, therefore making loan interest rate for the borrower as little as 12 or 13 percent. This is free market at its finest, when the market sets the real interest rate for the benefit of the borrower. Secondly, we are very consumer friendly. We talk, look like and do our business like majority of our clients. We know, what they want and we are doing our best to meet those expectations. Lastly, we have a fair commission policy. That means that if borrower has high credit rating, our commission is lower.

What ROI can investors expect?

It‘s all up to investors. Loan interest rate will be between 10 and 40 percent, therefore investors can decide for themselves if they want lower risk and lower potential ROI or higher risk with possibility of higher potential ROI.

How did you start Finbee? Is the company funded with venture capital?

FinBee started little over a year ago, when I quit my position as a CMO in one Lithuanian company and started everything from scratch: examining the market, getting know-how, attracting investors and partners, picking up experienced team members. Big breakthrough moment was when Madiston became our partner and we got a technological edge against our local competitors

Is the technical platform self-developed?

No, software is provided by Madiston, whose Tim Simon is also member of FinBee board. Tim has an extensive experience of delivering successful applications to the Financial Technology marketplace as a founder and CEO of Quotient plc and Mondas plc, listed on the London Stock Exchange and AIM respectively. Continue reading →