Today, new p2p lending marketplace Crosslend launched offering unsecured loans to consumers. Opening to borrowers and investors in Germany and Spain as well as investors in the UK, Crosslend aims for further European expansion and creating a unified European marketplace.

The Berlin headquartered startup was founded by Oliver Schimek and Daniel Schlotter (both had previous FinTech experience at Kreditech) and Marie Louise Seelig (formerly Skrill). Crosslend already raised a funding round prelaunch from Lakestar, Atlantic Internet and others.

Markets targeted by Crosslend

When a loan is granted it is purchased and acquired by Luxembourg based Crosslend Securities SA and securitized by a series of ‘notes’. Notes are debt securities which can be purchased by investors. A series of notes is made up of a number of notes, each with a denomination of 25 EUR. The total nominal value of a series of notes is equivalent to the amount of the loan. When a borrower makes their loan repayments, CrossLend Securities SA makes the corresponding payments of interest and principal pro rata to the holders of the notes. This will enable Crosslend to offer a secondary market, which is due to be launched in a few months.

Borrowers can apply for loans from 1,500 to 30,000 Euro for loan terms from 6 to 60. Crosslend will grade loans in risk classes A to G, HR. Interest rates (APRs range from about 3.5% to about 17%) and borrower fees are dependent on the assigned risk classes. Crosslend checks submitted proofs of income for all loan applications.

To invest lenders first open an account with biw Bank, the partner bank of Crosslend, this involves a short video verification process of the investor’s identity (webcam required). Video verification is an innovative account opening process which several German online banks started to use to replace the identification via postal communication. Investors then deposit money into their account (250 Euro minimum). Then investors can choose which loans they want to invest into (25 EUR minimum bid per loan). Crosslend charges investors a 1% fee at origination.

UK investors should consider using Transferwise or Currencyfair to exchange money into Euro to avoid possible bank fees and a bad exchange rate applied by the bank. Continue reading →

Žltý melón, the first p2p2 lending service in Slovakia, has successfully completed a Series A investment round and raised its capital to strengthen further development and implementation of strategic plans.

According to information P2P-Banking.com obtained from the Žltý melón management, the first tranche was little below 1M EUR, with the agreement for additional capital in range of 2M EUR after several milestones will be achieved.

Žltý melón acquired investments from EU-investment fund program JEREMIE, which is managed by Limerock Fund Manager, FTK Invest, an investment company, and Mr. Hendrik Bremer, a long-time business partner of financial services in Central and Eastern Europe at PwC and Roland Berger, strategy consulting companies. Mr. Bremer has also joined the company’s management and thus supports its existing team.

Read an earlier guest post by CEO Roman Feranec about the P2P lending market in Slovakia. The company plans to expand further into the Czech Republic and other countries in Central and Eastern Europe.

“After being on the Slovak market for two and a half years, we launched our Series A Investment Round in order to raise capital to accelerate growth and further implementation of our strategic plans, particularly in the areas of product portfolio, services for our clients and territorial expansion. We do see the investment as a confirmation of trust in the innovative business model and our company; it also shows that ​​peer-to-peer lending is perceived positively not only globally, but also in Slovakia. We really appreciate that Mr. Bremer has joined our team. His extensive experience in the development of financial services throughout our region will greatly assist in our future development,” says Roman Feranec, CEO of Žltý melón. Continue reading →

The small businesses who already use H&R Block for bookkeeping, payroll, taxes and other accounting services now have access to a new online service: business loans up to 500,000 US$, thanks to a new referral partnership with Funding Circle, a p2p lending marketplace for small business loans.

Through the partnership, Funding Circle loans are the preferred solution for H&R Block Small Business customers seeking financing to grow.

The new agreement bolsters Funding Circle’s diverse strategic partner ecosystem, which has experienced a 313% growth in monthly originations since January 2015. Other key partners integrated onto the platform recently include Intuit, Tri-Net, LendingTree, Credit Karma, Creditera and the National Small Business Association.

“Funding Circle offers strategic partners across multiple verticals the opportunity to build value-added services by leveraging our core technology, strong underwriting and customer-first approach to deliver unique financing solutions for their small business customers,” said Funding Circle co-founder and US managing director Sam Hodges. “Building a rich and diverse partner ecosystem is a core part of our growth strategy, and we are proud to welcome strong brands like H&R Block onto our platform who share our values and mission to help small businesses grow and prosper.”

“The mission of our two organizations are very similar,” said Jeremy Smith, director of Block Small Business. “We both provide services to small businesses that enable successful, sustainable growth. Given that we do the accounting for service businesses with less than $20MM in revenue, our clients have found it difficult to get loans from traditional banks. Well, Funding Circle specializes in lending to these types of businesses; so now our clients have a go-to source for capital to grow their businesses.” Continue reading →

British p2p lending marketplace Assetz Capital will launch a new ‘Quick Access Account’ (QAA) in the very near future.

The new account has a capped target rate of 3.75% gross per annum (before tax and any loan losses) and benefits from the added protection of a Provision Fund. The target rate can vary each month, being set at the beginning of each month based on the loans within the account, but the target rate will never fall below 3.75% gross per annum. Investors may invest up to 25,000 GBP each and the account will be capped at 1M GBP initially and is expected to grow in the future.

The QAA is designed to provide the highest possible speed of access to their money if an investor wishes to withdraw funds at any time, for whatever reason. In normal market conditions transferring funds between Assetz Capital Investment Accounts should be possible within seconds, while withdrawal of funds completely should happen within two days.

There is no fee for immediate access nor any notice period.

The accounts main use will likely not be long term investment, but rather help investors avoid cash-drag while waiting for new investment opportunities to open. Chris Mellish, Technical Director stated: “This isn’t an invest and hold account, ….  One feature … is that you can set your other accounts to automatically invest idle cash in the QAA.  So you could have 10K GBP invested in the MLIA, for example, waiting for a loan to draw down or waiting for .. loan units to become available and that money will earn 3.75% until it’s needed.  The system will automatically pull the money out of the QAA as soon as loan units become available on the loans you’re interested in.”

Stuart Law, CEO at Assetz Capital commented, “We believe that quick access to funds is a fundamental challenge in any investment product – whether it’s a bond, an ISA or a peer-to-peer product. The Quick Access Account not only means that money can be accessed quickly, but because of Assetz Capital’s model, the account offers a target rate of 3.75% gross per annum which should appeal to those looking for good risk-adjusted returns.â€

The Quick Access Account invests in both short and long-term loans and interest is earned and paid monthly. The account always retains substantial cash balances in order to facilitate quick access for investors who require their investment back on short notice and really helps address the issue on many P2P platforms where uninvested cash does not usually receive any return. An investor can press a button to choose to invest any spare cash they have at any time in the QAA and then release it when they wish to invest it elsewhere.

Mr Law, added: “This account really opens the world of peer-to-peer lending up to the mass market. Those investors who want to dip a toe in the water, earn a fair return and have quick access to their cash rather than be tied up in a 5 year loan can do so. Those who were worried about being able to access their funds quickly can be reassured that this product delivers that and therefore the returns on offer can be realised.†Continue reading →

Mintos is a marketplace lending platform that brings together investors and borrowers by enabling various loan originators to use a marketplace lending model in funding loans. Previously loan originators established their own platforms; now Mintos offers a single platform to those non-bank lenders that seek to sell loans. This means non-bank lenders do not have to make major investments in establishing and maintaining their own platforms. By connecting to the Mintos platform non-bank lenders get an instant access to investors that are looking to purchase marketplace lending assets. Thus, non-bank lenders can focus on their core skill of originating loans.

What are the main advantages for investors?

At Mintos investors can invest in loans that are originated by various non-bank lenders that use our platform to fund their loans. The main advantage for the investors, accordingly, is that they get an access to much broader investment opportunities as part of a single platform, both in geographic terms, and in terms of various loans originated by various non-bank lenders. Investors on the Mintos platform can invest in mortgage loans, secured car loans, small business loans, and soon also unsecured loans. Loans are currently originated in Estonia, Latvia, Lithuania, and we are about to add loan originators from Finland, Georgia, and Spain. This, combined with the fact that the minimum investment in one loan is EUR 10, means that investors can easily build very well diversified investment portfolios. Also, as a result of having various loan-originators and many investors on one platform our secondary market is very liquid.

It is also important that non-bank lenders whose loans are available to investors on our platform are experienced in underwriting. The platform is used by Capitalia, for instance, which is the leading small business lender in the Baltic sates and has been lending for five years. All lending processes are orderly at the company, it has experience, and it has access to historical data. That is essential for investors who can be sure that the detailed credit analysis are preceding the granting of a loan. Moreover, the loan originators on the Mintos platform are required to retain a part of each loan on their books, i.e., to have “skin in the game†to align their and investors’ interests.

Finally, all loans on the Mintos platform are prefunded by the loan originators; thus investors can start earning from the moment of the investment and there is no cash drag. At the moment more than EUR 1 million of loan inventory is readily available for investment on our platform.

What about borrowers? What are the advantages for them?

Mintos does not issue loans, but it is important for us that the loan originators who use our platform at the end of the day can offer cheaper rates to borrowers. Also, the lending process is much more convenient at these loan originators. When borrowing money from Capitalia, for instance, a small company can expect the money to arrive in its account in just a few days’ time, usually even faster. At a bank, by contrast, that could take several weeks. Finally, some of the loan originators who use our platform provide loans and services to those borrowers who might not have had an access to affordable credit before. For instance, among clients of Mogo, the largest non-bank car loan provider in the Baltic region that is also on our platform, there are those who are seeking a car loan, with the average requested sum being around EUR 3,000. This segment is underserved by the banks.

What ROI can investors expect?

So far the average net annual return for investors investing via the Mintos platform have been slightly below 13%. We expect the average net annual return to hover around the low double digits also in the future. However, investors should look not just at the return, but also the relevant risks. In the case of Mintos, investors can easily build a very well diversified investment portfolio across different loan products and geographies, thus reducing unsystematic risk within the marketplace lending asset category. Also, the Mintos platform was the first with a buyback guarantee where some of the loan originators buy back non-performing loans from investors, thus substantially reducing risks for investors.

What is the background of Mintos?

We started to work on the idea in mid 2014 and launched the platform in January 2015. I come from the investment banking where I spent six years before going for an MBA at INSEAD. That, actually, was the first time I heard about the peer-to-peer lending because I borrowed from Prodigy Finance, a platform that provides funding to international postgraduate students attending top-ranked business schools, while also delivering competitive financial returns to institutional and private investors. The other Martins, Martins Valters, our CFO and also a Co-Founder, has 11 years of experience from Ernst & Young where he audited some of the largest financial institutions in the Nordic region.

To fuel our growth we have raised EUR 1 million in venture capital to date. That has helped us in forming a strong team and an experienced board of directors. In a bit more than six months since the launch, more than 2,400 investors from 30 countries have registered on the Mintos platform and funded more than 1,500 loans for a total of more than EUR 4 million, of which EUR 1 million in the last month alone.

Is yours a bespoke platform?

Yes. We began work on the platform half a year before we launched it to the public, and we developed it in-house from scratch. Each marketplace lending platform has its own nitty-gritty approach, so it is best to design the platform ourselves. The Mintos platform is used by various non-bank lenders, and so we see ourselves as a technology company with a strong finance background. Currently, we have eight software developers in our team. We listen carefully to what investors say and appreciate their feedback as it greatly helps in improving the platform. Continue reading →

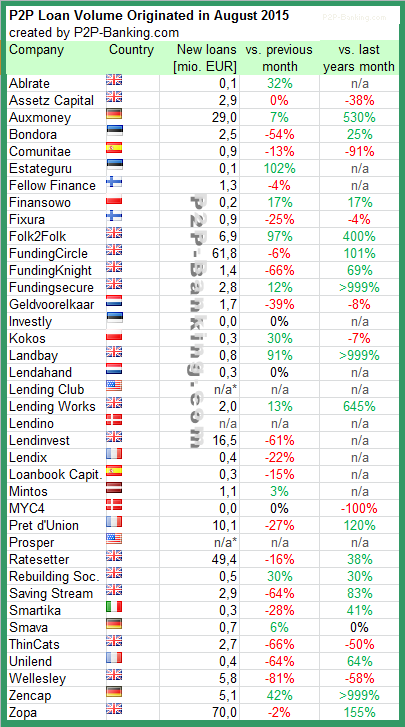

The following table lists the loan originations for August. August was a slow month for many of the listed services probably due to the holiday season. Zopa crossed 1 billion GBP lent since inception (see infographic) and Giles Andrews stated he expects the next billion to be lent in 2016. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in August 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.