[WpProQuiz 1]

See how other users fared: Continue reading

[WpProQuiz 1]

See how other users fared: Continue reading

In October 2012 I started p2p lending at Bondora. Since the start I did deposit 14,000 Euro. Since then I periodically wrote on my experiences – you can read my last review published in August here. In the 4 months since then, many changes happened at Bondora: New portfolio manager, new dashboard view, new collection procedures, a first version of an API in production, no more transaction fees for buying and selling on the secondary market and Bondora now allows investors to sell and buy defaulted loan parts (60+days overdue). I used this change to sell my overdue Slovakian loans at 87% discount. I also sold my remaining Spanish loan parts. I did not have much of either of these in my portfolio anyway.

I also reduced my overall portfolio position at Bondora and transferred 11,022 Euro back to my bank account. I managed to sell many of my Estonian loans at a premium. My perception is that the liquidity on the secondary market increased after the transaction fees were removed. Still it is hard to effectively navigate on the secondary market.

I find it hard to price 60+days overdue loans I want to sell on the secondary market. The site Bondpicking.com has charts with recent transactions for defaulted loan sales on the secondary market that can help as guidance.

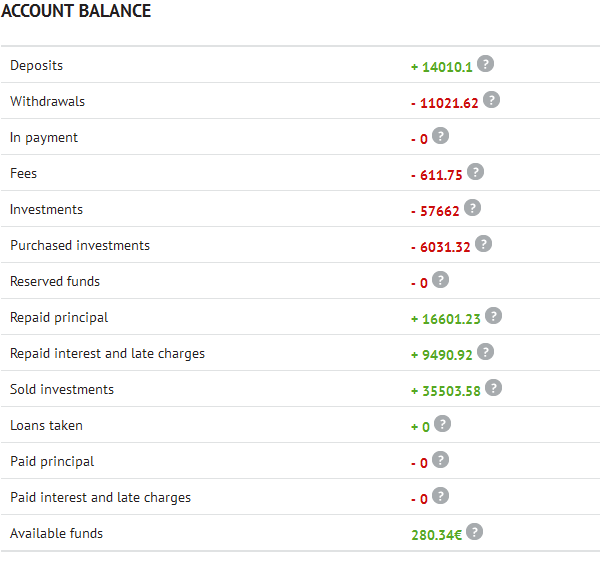

Currently I still have loan parts with the value of 11,428 Euro outstanding principal. Of these 1,441 Euro are in loans that are overdue and 2,076 Euro are in loans that are 60+ days overdue.

At the moment I have 280 Euro cash available.

Chart 1: Screenshot of account balance

My interim conclusions after 3 years

I am very satisfied with my Bondora investment. Of the 14,000 Euro investment I already withdrew over 11,000 Euro, meaning my remaining risk (concerning the initial investment) is very limited and I still have a huge portfolio of loans. Currently Bondora shows my ROI to be 25.0%. In my own calculations, using XIRR in Excel, assuming that 30% of my 60+days overdue and 15% of my overdue loans will not be recovered, my ROI calculations result in 16.3%. Even in a very pessimistic scenario adding up only withdrawals (approx 11,000 Euro), current loans (about 8,200 Euro) and cash (280 Euro), the initial 14.000 Euro grew in three years to a value of 19,500 Euro. Continue reading

![]()

![]() In Germany p2p lending marketplace Lendico uses a solution offered by startup FintecSystems to simplify the borrower application process. Automatically accessing online banking data for the past 90 days of the applying borrower the service makes the postal submission of bank statements and certificates of salary via postal services redundant. This saves time and costs involved in the verification of the borrower’s loan application.

In Germany p2p lending marketplace Lendico uses a solution offered by startup FintecSystems to simplify the borrower application process. Automatically accessing online banking data for the past 90 days of the applying borrower the service makes the postal submission of bank statements and certificates of salary via postal services redundant. This saves time and costs involved in the verification of the borrower’s loan application.

Co-Founder Christoph Samwer said: ‘The integration […] is an important step to offer our borrowers an application process rid of media discontinuity and to improve our risk assessment‘ (original quote in German, own translation).

Here is what FintecSystems says about their service:

…Our recently released new product called FintecSystems RISK enables lenders to obtain real time financial information about their customers using just their online banking account. This results in a more accurate and seamless loan application processes by enriching existing application processes or existing data.

With FinTecSystems RISK lenders can access up to 90 days of customer account activity. For lenders it is possible to derive certain information of interest from the account activity, e.g. using salary to carry out risk assessments. Also validating or completing financial information of the borrower to have a consistent data basis, while reducing the need for manual interaction efforts and costs for both parties.

With FinTecSystems RISK, we build a bridge between BigData and SmartData. Accurate information about a borrower enables the lender to be more effective with loan terms. Precise and quality data is more important than data quantity. Data quality is the crucial factor to establish an online financing process in Germany and Austria. Eliminating a manual finishing processing step for the lender…

![]()

![]() Ratesetter informed its investors that it will update the legal structure of the provision fund by changing it from a trust to a limited company. Ratesetter was the first UK p2p lending marketplace to introduce a fund to protect investors against defaults (up to the amount available in the fund). So far no retail investor has lost a penny on Ratesetter since the launch in 2010.

Ratesetter informed its investors that it will update the legal structure of the provision fund by changing it from a trust to a limited company. Ratesetter was the first UK p2p lending marketplace to introduce a fund to protect investors against defaults (up to the amount available in the fund). So far no retail investor has lost a penny on Ratesetter since the launch in 2010.

Excerpt from the announcement: Continue reading

MoneyPlace, Australia’s second fully licenced peer-to-peer (P2P) lender and Auswide Bank have entered into a significant strategic relationship and equity deal.

The long term relationship, the first of its kind in Australia, includes a 5 year deal to fund up to 60 million AUD to assist MoneyPlace to grow its consumer lending and for the bank to grow and

diversify its financing activities nationally. Additionally Auswide Bank is taking a 20 per cent equity stake in MoneyPlace.

MoneyPlace launched in October after receiving its retail and wholesale Australian Financial Services licence and provides loans of 5000 to 35,000 AUD through its peer-to-peer lending platform.

MoneyPlace CEO Stuart Stoyan said the relationship is a critical milestone for P2P lending globally and demonstrates how banks can work with P2P lenders to provide fairer, better rates

for all customers. Continue reading