I started investing in loans on the Latvian p2p lending marketplace Mintos right after it launched 12 months ago. At that time Mintos offered real-estate secure loans only. The service has evolved hugely with a much wider range of loan types on offer now. Mintos now serves as a platform to enable the transactions while partnering with loan originators, who actually originate loans and are responsible for vetting the borrowers.

Overview of the current main parameters for investors:

Different loan types

Typical interest rates range from about 8% to about 14%

0% fees for investors on the primary market (1% seller fee on the secondary market)

All loans prefunded; investors earn interest from the day they invest money into a loan

Depending on the provider, some of the loans offer buyback guarantees; that means if the loan becomes more than 60 days overdue the provider will pay the principal and the interest of that loan to the investor

Open to international investors

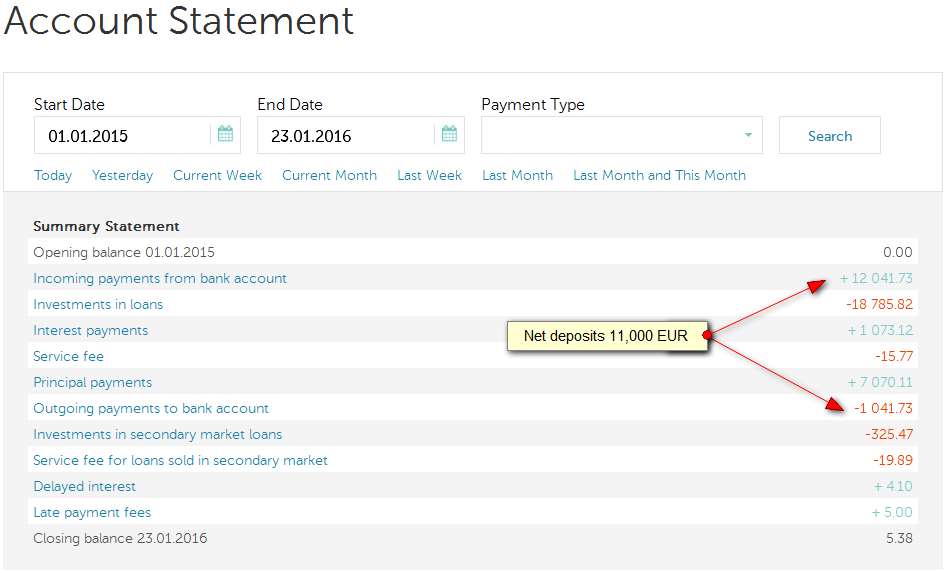

During the past year in several installments I deposited 11,000 Euro into the account via SEPA transfer (actually I deposited 12,041 Euro; but I also withdrew 1,041 Euro). Deposits are fast and reliable; they usually took less than 1 business day for me. Most of the time, I reinvested all repayments and interest earned.

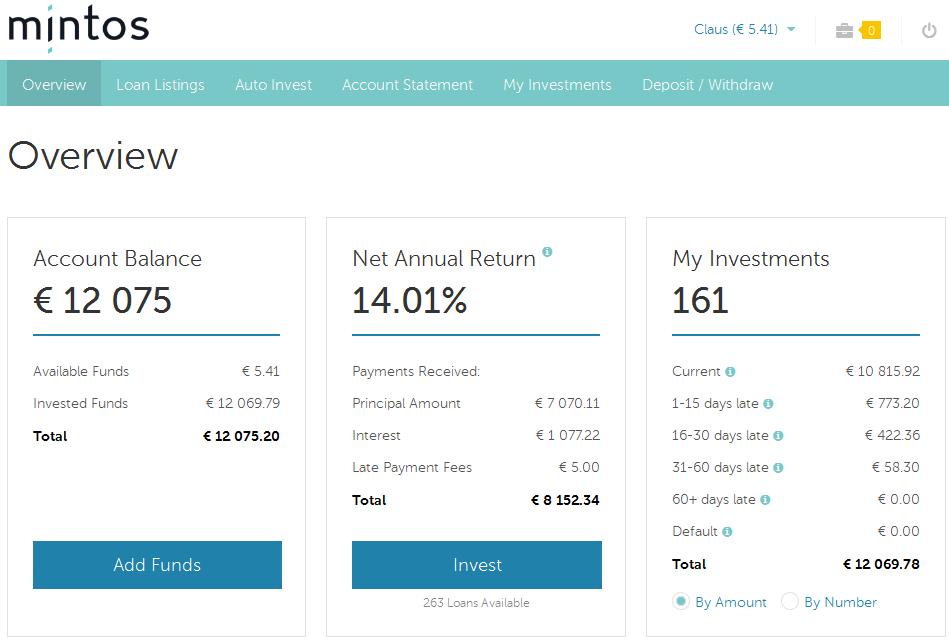

My portfolio yielded 14% ROI so far

Currently I have 12.069 Euro invested in 161 different loans. Over 70% of the amount is in Mogo secured car loans (with buyback guarantee). Over 20% is in mortgage loan (without buyback guarantee). The remainder is in business loans and invoice finance loans (mostly without buyback guarantees). I stayed clear of the personal loans Creamfinance originated in Georgia. The shown 14.01% are an accurate reflection of the actual ROI, I believe. Continue reading →

Beehive is the first and only P2P financing platform in the UAE (United Arab Emirates). Otherwise known as marketplace lending, peer-to-peer finance is the practice of lending money to unrelated individuals, or “peers”, without going through a traditional financial intermediary such as a bank or other traditional financial institution. Beehive bridges a significant funding gap that currently exists in the UAE market. Our platform applies the innovative technology of crowdfunding to eliminate the cost and complexity of conventional finance. Businesses bypass conventional intermediaries and receive financing directly from the crowd. This enables them to get faster access to lower cost finance, while investors get better returns. Beehive is a facilitator that enables businesses to secure the funding they need by creating the organizational framework and infrastructure required for community and financial support to materialize.

What are the three main advantages for investors?

The three main advantages for investors are:

No Barrier to Entry: Individual investors can invest from as little as AED 100 into each business listed on the platform and receive monthly repayments currently averaging 12% per annum with reinvested returns. Investors get money transferred into their account in as little as two days.

Diverse Portfolio: By investing on the Beehive platform, investors can diversify their risk across a number of products offered to a variety of companies operating across diverse sectors, with new companies listing on the platform every week. They are able to directly invest in a business they believe in. Investors are also able to buy or sell their finance parts to other investors on the platform through Beehive’s secondary market. This gives investors access to a market place where they can trade finance parts and allows greater access to liquidity and diversification.

Sharia Compliant Structure: Beehive allows investors to ethically invest in some of the most innovative SMEs in the UAE. Beehive supports Dubai’s ambition to be a Global Financial Capital with its innovative Sharia-compliant platform, which helps Islamic finance customers to achieve their financial goals in a more ethical structure, and helps compliant SMEs tap sources of Islamic finance liquidity. Beehive was certified by the Shariyah Review Bureau (SRB) as a Sharia-compliant P2P finance platform in September 2015, making it the first P2P platform in the world to independently confirm its processes are compliant with Sharia principles.

What are the three main advantages for borrowers?

The three main advantages for borrowers are:

Cost of finance: The platform offers considerable savings to businesses that need it: Businesses using Beehive save on average 30% on their financing costs. The average bank borrowing rate (unsecured) for SMEs in the UAE is over 18%, often much higher. Because investors compete for rates in a reverse auction process, business receive the lowest possible average rate from investors.

Time to finance: The Beehive online marketplace facilitates faster, more flexible funding, with companies typically getting a decision on their finance requests in 3 days. The application process is completed online, and businesses receive funding in 14 days or less.

Invoice Financing: Beehive’s SME invoice financing tool is designed to serve SMEs and help them manage their cashflows by closing the gap between the issue of an invoice and the receipt of actual payment. By unlocking the value of their accounts-receivable, they are able to tackle the dual challenges of rising inflation and late payments. These products give SMEs more options to plug invoice gaps, giving them greater control over their business and finances, and thus a greater opportunity for security and growth.

What ROI can investors expect?

The average return for investors is 12% per annum with reinvested returns

Please tell me more about Islamic Finance and Sharia Compliance. Is that a main factor for attracting clients?

One of the things we are very proud of is receiving our Sharia Certification. Globally we’re the first platform to be certified sharia compliant. It was our plan from the beginning to make a sharia P2P platform, because it hadn’t been done before and it would open a new asset class to Islamic investors. About 80-90% of businesses on the platform are Sharia compliant. What we find is that if the listing is sharia compliant, then investors will engage with the business whether they are conventional or Islamic, so it is a very attractive feature for both investors and businesses across the board.

How did you start Beehive? Is the company funded with venture capital?

Beehive has so far received two rounds of external funding in addition to founding investment.

Is the technical platform self-developed?

All the technology on the Beehive platform has been developed using in-house capabilities. Our in-house IT development, design and creative teams allow us to be agile and responsive to market needs. Continue reading →

I started investing at the UK p2p lending marketplace Saving Stream in December 2014. The last Saving Stream review I wrote was 9 months ago, therefore time is right to post an update on how my portfolio is developing.

For those p2p lending newbies that have not heard of Saving Stream so far here are the basics again:

Bridge loans, secured by commercial properties (first or second charges)

12% interest (interest rate is the same on all loans on the platform)

0% fees for investors (on primary and secondary market)

All loans prefunded; investors earn interest from the day they invest money into a loan

A provision fund shall provide a buffer against default losses

Open to international investors

To deposit money I used Transferwise and Currencyfair saving me bank fees and allowing me to know the currency exchange rate in advance.

I made 5 deposits over time totalling 5,441 GBP (7,403 EUR).

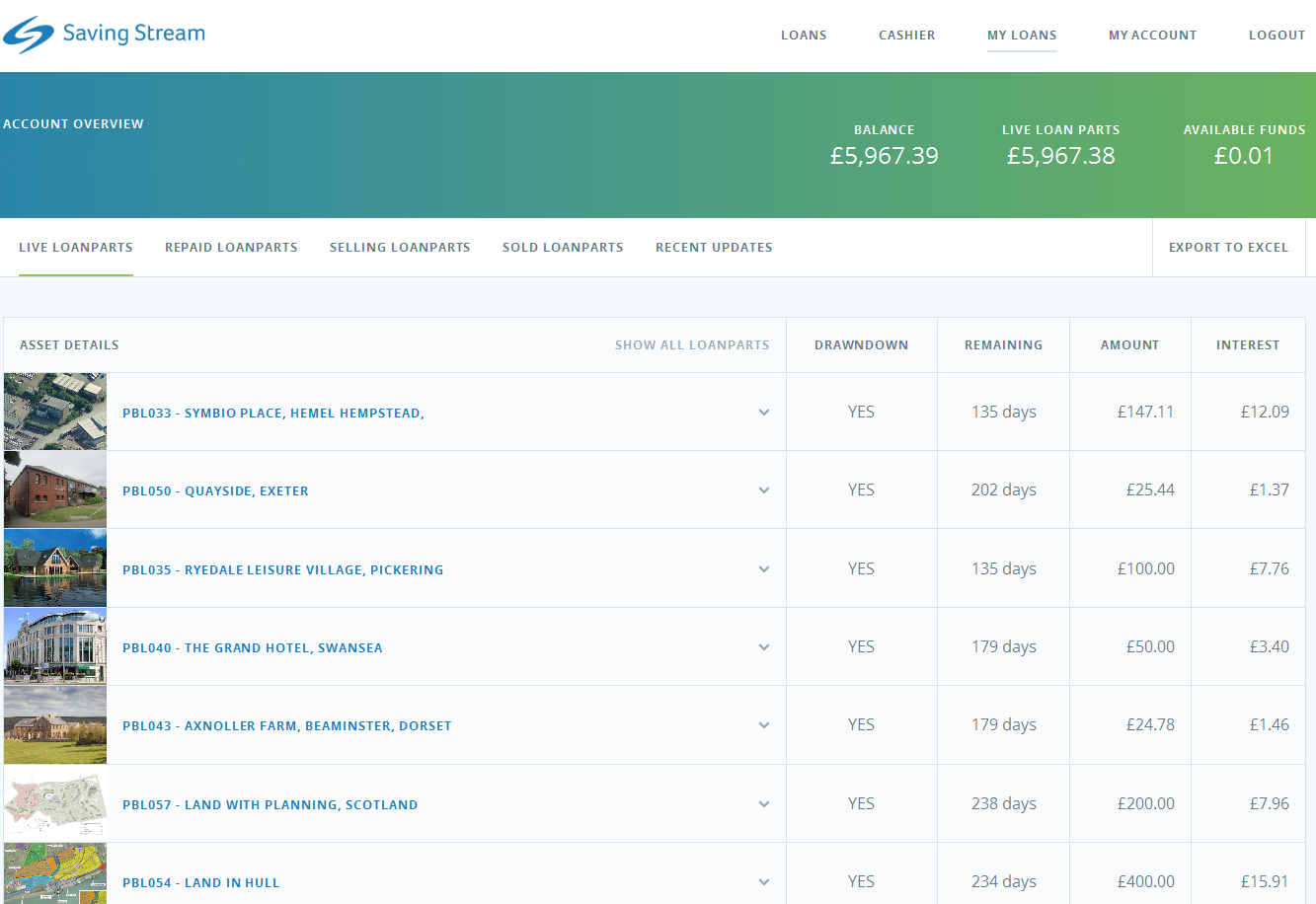

Screenshot: Top of the list of my Savingstream loan portfolio

My portfolio grew nicely and yields a very got ROI

As you can see in the image, my original 5,441 GBP grew to 5,967 GBP current portfolio value. I reinvested all repayments and interest earned. It sure is nice to earn 60 GBP interest per month (1% of live loan parts amount). My ROI is actually a bit over 12% so far as I profited from several cashback offers. I did not experience any defaults on my loans so far.

The new website

Late in 2015 Saving Stream overhauled the website. Major improvement is that this fixes the situation which frequently occured on the old website, where loan parts sold/bought on the secondary market might get stuck when a loan amount left on offer accidently ran into a negative value and needed manual operator intervention to clear. The new website also introduced the two step verification security option. I enabled this security feature for my account. Continue reading →

Viventor is about providing sensible investment opportunities for investors from all over Europe. As we started considering the idea of Viventor less than a year ago, peer-to-peer financing was achieving remarkable success in the US and the UK. In contrary, the “old continent” was relatively underserved.

And so the goal was set – to build a peer-to-peer lending platform for European investors that is accessible, makes investing convenient, and offers high quality services, investment opportunities, and the product itself.

What are the three main advantages for investors?

Firstly, it is the investments themselves. All loans currently offered are secured by liquid real estate mortgages, as well as come with Buyback Guarantee. The weighted-average LTV ratio of our loan book is 28.45%, and we are proud to be the market leaders in terms of providing such low-risk opportunities.

Secondly, the investors receive fixed monthly interest payments. Relatively few platforms do this, but we see it as an advantage for the investors. Instead of diminishing interest and trying to crack advanced formulas, we offer straightforward logics and exactly the same payments every month. We want to make investing convenient also for people relatively unfamiliar with the world of finance and peer-to-peer lending.

Thirdly, it is the simplicity and convenience of investing. We are constantly making efforts towards removing the friction from the investment process itself by building the platform and its UI simple and intuitive for any user. Improvements based on everyday findings are constantly implemented, new languages are added, and educational material is made available. Our aim is to for investing to be simple and enjoyable.

What are the three main advantages for borrowers?

Viventor does not originate loans itself, and this is unlikely to change in the foreseeable future.

However, if we speak about the partner companies that have currently listed their loans on Viventor, there are a couple of things worth noting. The companies consist of professionals, possessing years of experience in non-bank lending and underwriting, and having their skin completely in the game. Also, access to financing for eligible borrowers is considerably faster than that offered by alternative creditors. This has been achieved by combining years of experience and knowledge with machine learning and other modern technologies.

What ROI can investors expect?

Currently, investors can earn up to 7% p.a. fixed, and there are no fees withheld. The number will be going up though, as we will be adding other types of loans with higher levels of interest.

Prestamos Prima, the mother company of Viventor, operates in Spain? What led to the decision to incorporate Viventor SIA in Latvia?

We as professionals have been in the non-bank lending for many years, involved in other projects before Prestamos Prima. While Spain is one of the major markets at the moment, it is certainly not the only one, and you can expect loans from other European countries being added.

What concerns Viventor being incorporated in Latvia – we are Latvians, and prefer to stick to our origins whenever we are able to choose. There is a lot of untapped potential and hidden talent in the Baltics, but then again – I believe people familiar with the European peer-to-peer financing market are well aware of that already.

Is the technical platform self-developed?

Yes, Viventor has been built in-house from the very first line of code, and we will keep the development of platform to ourselves. All in all, we believe the right approach for improving Viventor is by gathering feedback, applying our lessons learnt, constantly pivoting and optimising. And it is clearly much more efficient to achieve this with a dedicated engineering team in-house. Continue reading →

Marketinvoice and Platform Black have offered the possiblity to invest in invoice finance / invoice discounting loans for some time in the UK. However these were not an option for me due to requirements (minimum invest and/or UK bank account).

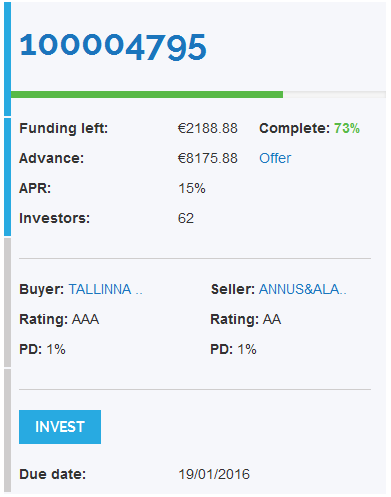

Therefore I made my first bid on a loan of this type on Investly on Dec. 31st. It was the first invoice discounting loan the Investly marketplace launched, making this asset class available to investors in the European Union from bid amounts as low as 10 Euro. Investly ran the offer in a three day auction period, with 15% maximum interest. Even though the bidding period was over New Year, the demand was high and several investors were outbidded during the underbidding auction (screenshot right shows status on first day of auction). Registered investors are able to see the underlying invoice that is financed.

The loan is for less than a month, due to be repaid on January 19th.

Today Mintos launched a cooperation with DEBIFO which as a originator will provide invoice finance loans on the Mintos platform. That enabled me to make my second bid in invoice financing. The loans listed today at the Mintos p2p lending marketplace carry interest rates from 11.2% to 13.8% and are for a loan term of less than a month.

‘For most of the small and medium enterprises in the Baltics, receiving client payments in time is critical in order to ensure continuous operations. While many of these companies have large, reliable and stable business customers, they typically set payment terms of up to 60 days or more, which makes it hard for small businesses to survive’, says the peer-to-peer lending platform Mintos CEO Martins Sulte, who welcomed the cooperation with DEBIFO.

Mintos management forecasts high investor interest in this investment product. Martins Sulte continued by saying ‘Most of these outstanding invoices are from stable, large companies, which means that the risk is relatively low. The other aspect that investors will like are the short repayment terms’.

Funding Societies is a peer-to-peer (P2P) lending marketplace for small-medium enterprises (SMEs) to get loans to grow and investors to get good returns in Singapore. We pride ourselves on innovation, as the first and only platform in the region to implement escrow service, e-contracting, webinar, internet chat and more. Since our launch in Jun, we have crowdfunded ~3M SGD (approx. 2M EUR) in loans to 35 SMEs with 100% repayment. We aspire to be the most trusted P2P lending marketplace in Southeast Asia.

What are the three main advantages for investors?

As investors ourselves, we believe returns, convenience and security are critical. Therefore we offer an alternative investment that gives investors a much better return than traditional fixed income, through the convenience of a fully-online and hassle-free investment approach, with funds handled by a professional escrow agency for security.

What are the three main advantages for borrowers?

Having worked with many SMEs, we find their biggest constraints to be capital, time and energy. Therefore we strive to provide them with capital at competitive rates, fast speed-to-cash and best user experience with minimal effort.

What ROI can investors expect?

We target the SME segment structurally underserved by existing financial institutions. Our interest rates are just a few percent higher than banks’, to minimize adverse selection. We charge 9% to 14% simple interest and pass the full return to investors with only 1% service fee. With diversification, we believe investors can earn at least 7%, much better than deposit interest of 0.05% in Singapore.

How is your company funded?

We began by bootstrapping. Thanks to a talented and committed team, we achieved numerous awards within the first 6 months and received considerable attention from the investor community, including strategic VCs who share the same values with us and now fund us.

Is the technical platform self-developed?

Yes, we built everything from scratch based on best practices we observed. It took us 95 days from start to launch, thanks to our talented CTO Felix Richard. Our goal is to deliver the best user experience, while ensuring security and scalability. Continue reading →