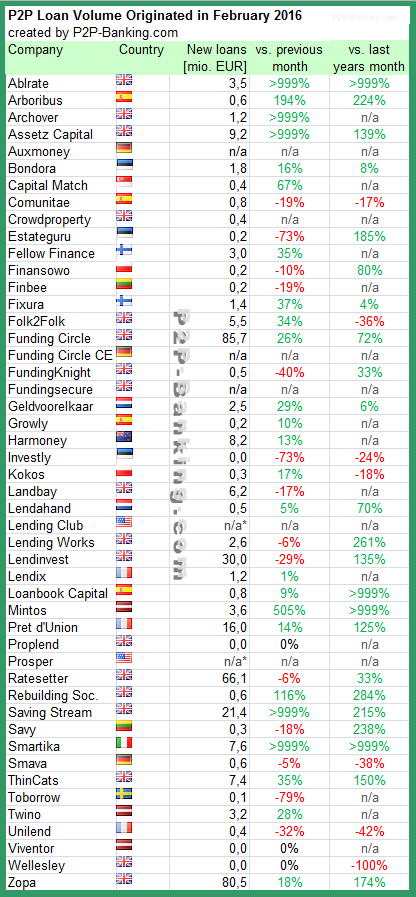

![]()

![]() After what felt like a drought period, Bondora seems to focus again on working to improve functionality for investors. This week they released a new version of the cash flow report, with the following upgrades:

After what felt like a drought period, Bondora seems to focus again on working to improve functionality for investors. This week they released a new version of the cash flow report, with the following upgrades:

1) Historic payments will be split between current loans and loans in default as per the status active at the date of the payment

2) We will introduce day-level information that shows cash flow categorized per each investment

3) Forecast settings can be defined also for historic schedules so you can use cash flow based adjustments for predicting future payments

4) You can adjust your net return calculation based on the probability settings defined in the cash flow report

5) Cash flow report will show the opening cash balance and closing cash balance for each period

6) You will be able to define which data series to show on the chart

7) Historic planned schedules will be split between current loans and loans in default

8) Cash flow table results can be exported to Excel

9) You will be able to define which data series to show in the cash flow table

10) Live data from the current day (currently under Account statement for the last 24 hours) will be incorporated into the cash flow report

11) All data is in one table

12) You will be also able to filter to a specific loan in the Investments list straight through the cash flow report so you can quickly take loans off secondary market or put them there based on the information visible in the cash flow report

I have experimented a bit and like the way this report page gives me a quick visual representation of what is happing in my account and that it is very customisable. Plus it lets me set my personal values for expected loss rates and use that to calculate net return displayed in the dashboard. Read also what investor Oktaeder blogged about this feature.

If you are not investing at Bondora, this Bondora video will give you a good overview of the functionality.