P2P lending marketplace Fellow Finance is now open for borrowers in Poland. Polish customers can now apply for peer-to-peer loans with maturity from 1 to 3 years up to 12 000 PLN. For Fellow Finance investors this gives an opportunity to diversify their investments geographically and in two currencies (EUR and PLN) with single consolidated user interface and reporting in investor’s own preferred currency. The ability to operate in multiple currencies also enables Fellow Finance to scale its platform to new geographies swiftly in the future.

‘Poland is a huge market in Europe with 38 million people. The Polish economy is one of the fastest growing in Europe. Consumer and consumption behavior are changing with the expanding economy. Mobile penetration and online lending have seen a fast and continuous growth in the last 4 years. Launching operations in Poland makes Fellow Finance a genuine international platform where investors can easily do direct investments in consumer loans across geographies and in multiple currencies. …’ says Jouni Hintikka, CEO of Fellow Finance. Continue reading →

Currently there is an increase of promotions by p2p lending marketplaces in order to acquire and activate retail investors. Cashback offers are more frequent and Funding Circle is giving away iPads to investors that will invest at least 20,000 GBP during the Funding Circle spring promotion. Investors welcome these added benefits, but for marketplaces it is a fine line to walk. They want to grow originations, but risk that investors will expect getting extras and might hold back further investments until the next offer is made.

I have written about the partnership between Google and Lending Club earlier. The image below shows an actual advertising message Google is sending to its Adwords customers. Note that a special loan is offered, not a standard Lending Club loan. This partnership is a great match for both Google and Lending Club. Google can enable its customers to get access to the funds they need to grow their business and potentially spend more on advertising services supplied by Google. Lending Club can target selected businesses, which were prescreened based on the data Google has via the Adwords customer relationship.

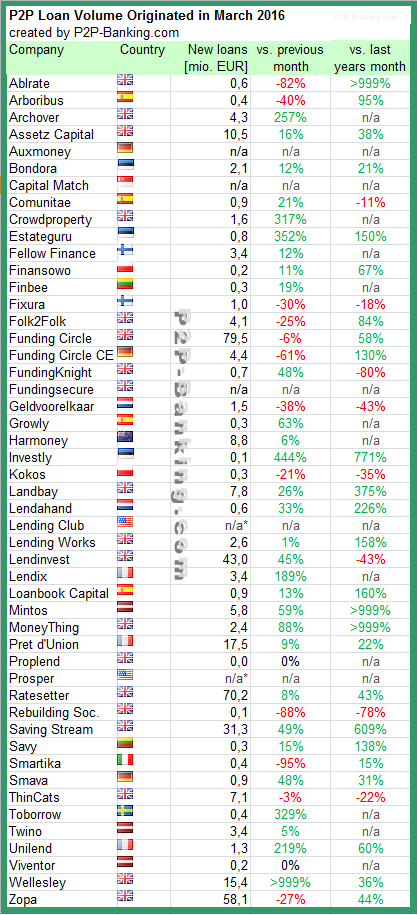

The following table lists the loan originations of p2p lending marketplaces in March. Funding Circle leads ahead of Ratesetter and Zopa. I added MoneyThing to the list. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Table: P2P Lending Volumes in March 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

As I started to check the facts for this article I planned to title it ‘How to Open a Free UK Bank Account Online’. Lateron I had to omit the word ‘Free’ – see below, but it still is a bank account that anyone in Europe can open online, all that is needed is an Android smartphone. That’s right, it is not limited to British expats, but open to anyone living in Europe. There is no iPhone App yet, but it is planned.

Why I opened a UK bank account

For the UK p2p lending marketplaces I use as a non-UK resident, a bank account in the UK is not really necessary. I use Transferwise and Currencyfair to transfer money and handle the currency exchange. One process where I think having a UK bank account is very useful, is when I want to withdraw money from one UK p2p lending marketplace in order to then deposit it at another UK p2p lending marketplace. Naturally in that scenario, I do not want to convert the pounds back to Euro and I want the transfer to be fee-free. Therefore I looked for a bank account, that would allow me to do this online. Another requirement was that I should be able to open this bank account without traveling to the UK and entering a bank branch.

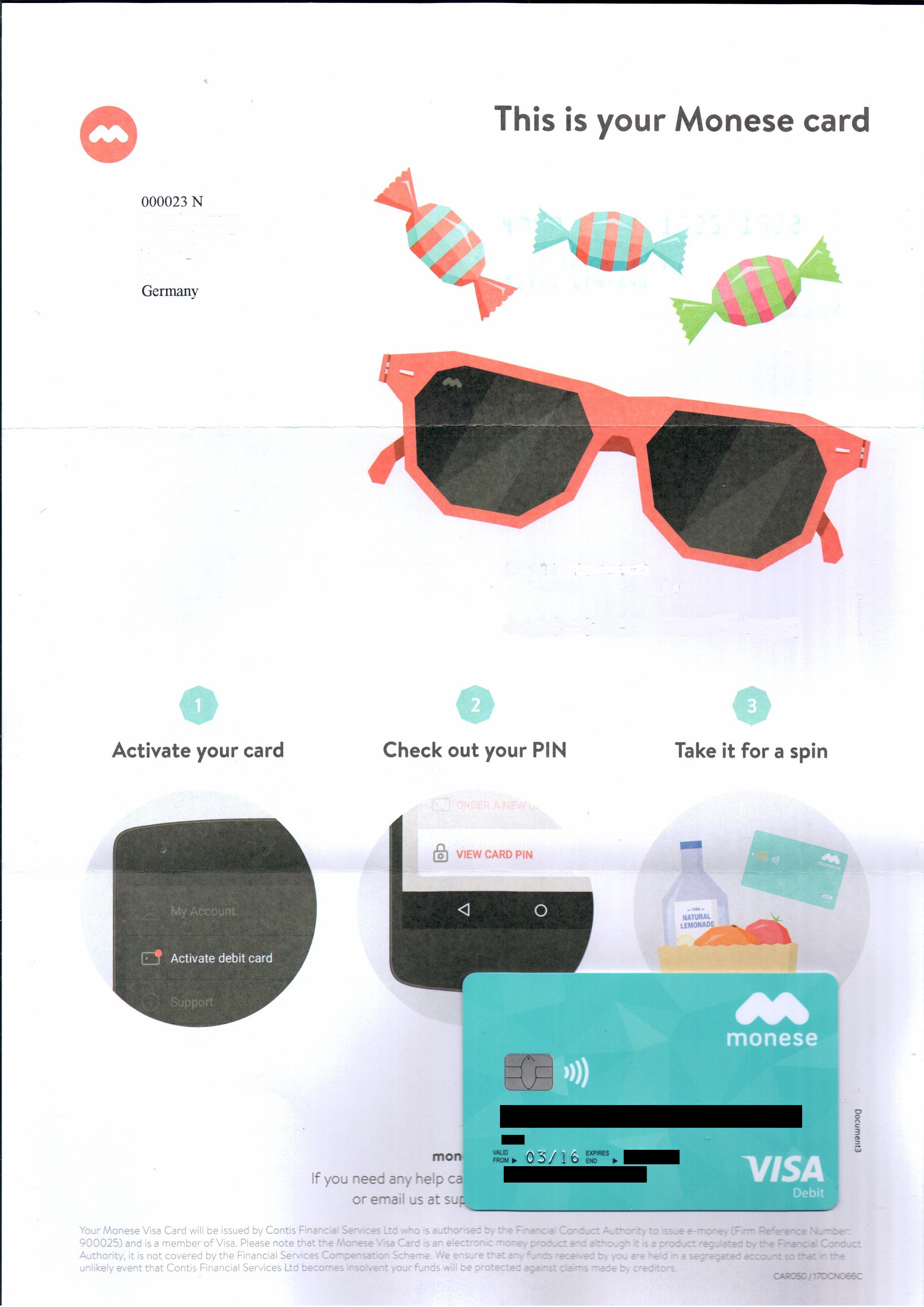

I opened a Monese account

I opened a Monese current account. To do this, I first downloaded the Monese app on my Android phone. Then it took about 10 minutes to register. In the course of the process I took photos of the front and the backside of my ID, did a selfie (smile) and filled in a form. That part was completed rather fast.

After that I had an unverified account, which had some restrictions. To lift these I uploaded the PDF of a recent bill with my name and address on it and waited. It took about 6 days until my account was verified.

Benefits of a Monese account for me

I have an own bank account number. Together with the sort code (which actually is the one of NatWest since Monese cooperates with NatWest) I can transfer money inside the UK fast and free. This is the main function for me. The account has more features, but actually I won’t be using these. Should I want to transfer money from my Monese account to my Eurozone accounts I will continue to use Transferwise or Currencyfair instead of making the transfer as I currently think this is the best way to optimise forex rates and at the same time minimize transaction charges.

Is this a free account?

When I signed up on March 18th, Monese promoted it as a free account. And in fact my account still is, I don’t pay a monthly fee and the transaction types I want to use are still free in my account (see screenshot). Other features – which I do not need like an ATM withdrawal or a card purchase abroad are priced.

But I talked to other investors, who signed up later than me (last week) and they were offered by Monese ‘First month free 4.95 GBP/ month‘. Seemingly Monese no longer offers accounts without a monthly charge to new customers (if this is uncorrect and it is still possible to get open an account without monthly fees applied, please post hints and tips how to do it in the comments. Thx!).

It should be noted that the account is not covered by FSCS as it is regulated as an e-money product.

The app so far does what it should and is self-explanatory, if a bit basic.

About a week after I opened the account I received a welcome letter with a VISA debit card, which I actually don’t need for my intented use of the account. But for other customers it will be useful to have a card with the account.

Update: Just received the message that my account won’t stay free either: ‘Hi …, as one of our early members you have been enjoying a mostly free service as part of our launch celebrations, only paying our rock bottom 0.5% fee on currency exchange when sending money abroad. Without you, we would not be here today and as a small “thank you” we’d like to give you an additional 2 months free servic. From 1st June, 2016 you will be billed a simpley fixed price of £4.95 per month taken directly from your Monese account balance,…’

To achieve further diversification of my p2p lending investments I opened an account at the UK p2p lending marketplace MoneyThing. All loans on the platform are secured by assets, which consist of a mix of property and other items like cars. MoneyThing launched one year ago and has since originated 10 million GBP in secured loans. It is operated by Capital Mortgages Direct Ltd. in London. So far none of these loans had any troubles.

The key aspects for investors:

12% interest rate p.a.

interest paid from the day the bid is made into a loan

no fees for investors

all loans secured by assets

bridge loans with a term of 3 to 24 months

there is a secondary market

minimum deposit is 100 GBP, minimum bid is 1 GBP

Steps to start lending

1. Registering

First I filled in the online form. MoneyThing is open to international investors, but the form had no country field, so I did enter town and country in the ‘town’ field. Later the same day I got an email from support asking me for ID and a further document to be uploaded as non-UK residents can not be automatically verified by their systems. I did that and within 5 minutes received the message that my account is now verified

2. Depositing

I used Transferwise to make my first deposit into the account to reduce transfer and currency exchange costs. A Transferwise alternative is Currencyfair. This time Transferwise took 3 days – a little longer than my usual experience for transfering to the UK with them.

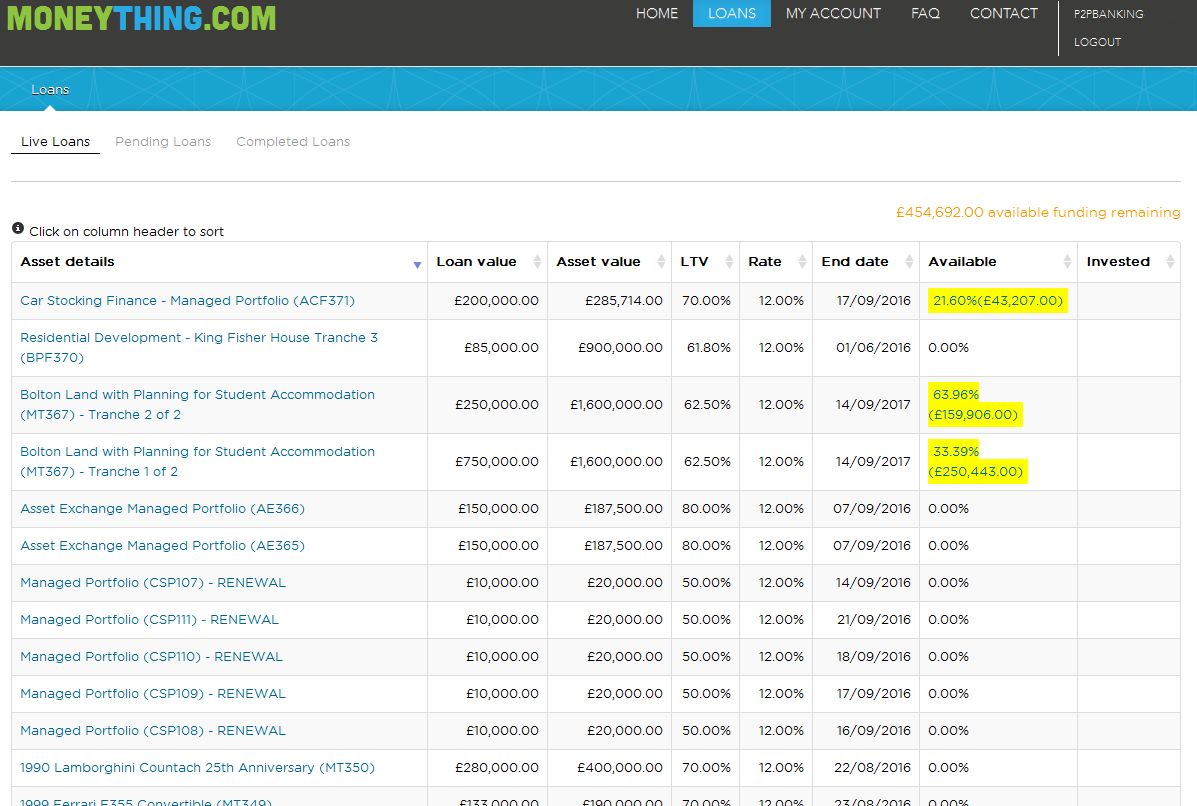

3. Selecting the loans on the market

MoneyThing lists all loans in a single market view – there is no separate secondary market view. All available loan parts are highlighted in yellow. Since loans are sorted chronologically to find parts of older loans on sale the easiest way is to resort by the ‘Available’ column. Otherwise just scroll down.

Clicking on a loan reveals detail information about a loan and supporting documents (e.g. a valuation report). Continue reading →