In Germany Kapilendo and Venturate announced they will merge. Kapilendo is a p2p lending marketplace offering loans between 30,000 and 2.5M Euro to SMEs for loan terms of 1 to 5 years. The minimum amount for investors is 100 Euro. Investors are not charged any fees. Kapilendo was launched in 2015 and recently gained some publicity, when it succeeded to fund a 1M Euro, 3 year loan to first division soccer club Hertha BSC in 10 minutes. This loan has an interest rate of 4.5%. So far loans listed at Kapilendo were in the range of 3.1% to 6.5% interest. Kapilendo uses Fidor as transaction bank to originate loans.

Venturate is a small equity-based crowdfunding site, launched in summer 2015.

FinLab, owner of Venturate will also invest an additional amount to foster further growth of Kapilendo. After the transaction FinLab now owns 25.1% of Kapilendo.

Informed sources told P2P-Banking.com that German Commerzbank plans to launch an own p2p lending marketplace called ‘Main Funders’ in the first half of 2016. The marketplace aims to connect SMEs seeking funding with investors. The name ‘Main Funders’ is a wordplay as ‘Main’ is the name of the river passing through Frankfurt, where the bank has its headquarter. The service is developed together with Main Incubator, the fintech incubator of Commerzbank. Currently all relevant domain names for Main Funders just redirect to the frontpage of Main Incubator. Commerzbank registered a trademark for ‘Main Funders’ in January 2016.

It remains to be seen whether this will be a full fledged marketplace, that also handles all transactions, or more a business initiation facilitator. A short mention in the 2015 annual report of Commerzbank uses the term ‘peer-to-peer-lending-plattform’ to describe Main Funders.

Under German regulation only banks can fund loans. To comply with this all existing p2p lending companies in Germany partner with a transaction bank which originates the loan and then sells the proceeds (repayments and interest) to the investors. So far a handful of small specialised banks were involved in these transaction. Commerzbank would be the first large German bank to enter the space and also the first bank to build an own platform.

Giromatch promises its customers “Better Banking Together”. We are a Direct Lending platform and offer our prime retail borrowers a complete digitized loan process at top rates. For investors we offer in this low yield environment a complete new asset class, namely the Deutschlandportfolio. What previously has only been accessible by banks, is now available to everyone – investing into a diversified prime loan portfolio and achieving an attractive return while keeping risks at a manageable level.

What are the three main advantages for investors?

The first great advantage for investors is that they get access to this new asset class at no costs. Secondly, the investment into the Deutschlandportfolio is automatically diversified. This is being achieved by a matching algorithm that optimizes each investment. The third advantage is the security-pool. Giromatch deposits a certain amount of each earned euro into the security pool in order to build up a security cushion for investors.

What are the three main advantages for borrowers?

The advantages for our borrowers result from the digitized loan application process. The loan application can be finished online in less than 10 minutes, no matter if you access Giromatch from home or mobile. A second advantage is the instant loan term confirmation without registration. After one enters all credit relevant facts, we show a customized rate, which we try to stick to as long as the input data was correct. A registration is not necessary in order to get a customized quote. A third advantage is our technology driven approach during the data verification process. A borrower does not need to send us documents proving the credit history. All we need from the borrower is a temporarily login into his/her current account, such that we can instantly confirm the credibility. Nevertheless, we think the most important advantage are the low rates we offer, which is only possible due to our digitized and cost-saving structure.

What ROI can investors expect?

The ROI depends on the portfolio the investor chooses. We provide two different maturities. The shorter-term Deutschlandportfolio runs for three years and has an estimated gross return of 3.60 % p.a. Investors who choose the portfolio with the investment period of five years can expect a gross return of 4.00 % p.a. Due to our strong credit checks we anticipate no more than approximately 1% losses p.a. post recovery due to expected defaults.

How is your company funded?

We were able to inspire several business angels from the financial industry for our seed funding round. Hence, we were able to not only fund the company but also to win many important contacts in the financial industry. Prior to the seed round we invested our own money and money from friends and family. And we were granted an EXIST scholarship by the Bundesministerium für Wirtschaft und Energie (BMWi).Continue reading →

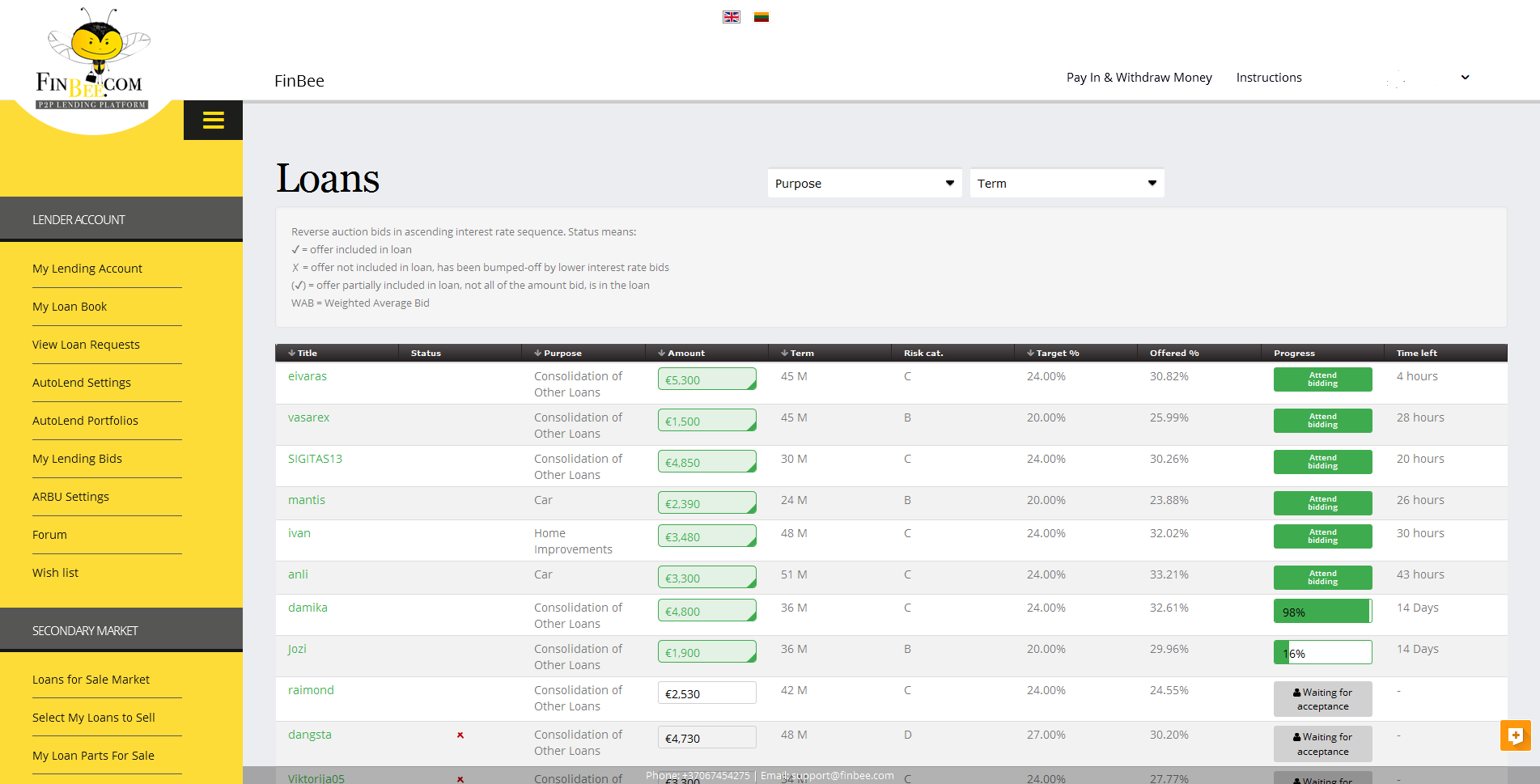

In August 2015 the new p2p lending marketplace Finbeelaunched in Lithuania. Finbee finances small unsecured consumer loans. The CEO told me that they meet all borrowers in person and that these are mostly looking to refinance other debts at higher rates, which they have paid in accordance to schedules punctually over months or years. Typical interest rates for investors are in the range of 20% to 32%. The platform is still very young, but recently loan volume picked up and Finbee crossed the milestone of 1M Euro loans financed since launch.

I started small and deposited only 50 Euro right after launch to test it and gain first hand experiences. Only two months ago I started depositing more and right now my deposited total amount is about 1,550 Euro.

The auction mechanism

Finbee lists all loan request and investors can bid either manually or via autoinvest (autolend). There is an auction period for each loan with investors underbidding each others in an reverse auction, meaning the interest rate will sink once the loan is filled. A pecularity of Finbee is, that each investor with a winning bid gets the individual interest rate he made the bid on, meaning there is no uniform lending rate for investors in the same loan (this is different from the way most other platforms handle reverse auctions, where usually all investors with winning bids get the same rate which is set at the highest winning rate at auction closing).

Loan requests at Finbee. The ones with the green button at right are open for bidding. Auction periods are initially set to 14 days but then reduced to 48 hours, once the loan is 100% filled by bids.

This auction mechanism often causes a mad rush in the last 5 minutes. Lots of bids are made right before closing and it is usual that the top closing interest rate drops 3-5% in these last minutes.

This is aided by a mechanism abbreviated ‘ARBU’ (Automated Response to Bumbed-off Underbids). Investors can enable ARBU to make lower bids on their behalf, once their original bid is outbid. The mechanism is quite configurable in selectable settings, but the catch is that it will not make more than 5 lower bids per loan. This led me to do quite a bid of configuring and experimenting with my settings. I also changed my strategy from multiple smaller bids on the same loan (e.g. 5 bids at 20 Euro), to now just 1 or 2 bids per loan at 30 to 35 Euro.

My strategy

In the first months I have just observed what is happening on the Finbee marketplace. Since February I go for the riskiest loans, risk category ‘D’ and sometimes ‘C’ with the highest loan amounts and the highest interest rates. I do all bids manually and have ARBU enabled with my settings, which I tweaked quite a bit. If I have multiple successful bids in one loan I try to sell some of the loan parts on the secondary market at premium in order to reduce the concentration. On the secondary market only current loans, that have made at least one repayment, can be sold. I also try to sell my late loans on the secondary market, but that means I have to wait for them to turn current again before I can sell them. Continue reading →

SocietyOne, an Australian p2p lending marketplace announced that it completed a 25M AUD round, supported by its existing shareholders. In 2014 Westpac owned Reinventure invested into SocietyOne. SocietyOne is led by CEO Jason Yetton, a former Westpac executive, who was appointed in March. The SocietyOne loanbook is currently over 100M AUD.

FriendlyScore is about allowing borrowers to use their online footprint as a way of increasing the amount of information a lender has about them. This can be useful for borrowers who lack credit history to get access to products they deserve, and also for allowing borrowers with some history to get better products by making lenders more comfortable with their risk profile.

How can your company help p2p lending marketplaces? Can you please share some references?

We help lending marketplaces make better credit decisions by enabling them to get way more data on their customers. By incorporating FriendlyScore into the platform’s decision engine, we can help prevent outright fraud; validate user identity and personal information; and most importantly, gain propensity insights from the users behaviour. This allows the platform to approve more borrowers (or lenders), reject more fraudsters and bad borrowers, as well as price their risk more accurately.

A borrower your software identifies as creditworthy has been previously ruled out by the scoring mechanism of the marketplaces. How would the marketplace deal with this loan when showing a credit grade/score class for this loan to investors? Assign a new class?

Our most common use case in the p2p space is for FriendlyScore to be offered as an optional way for borrowers to bump up to a higher internal credit rating if they get a high FriendlyScore. In other words, it is an opportunity for borderline declines to get bumped up to higher-riskaccepted, and for the accepted applications to get a better risk grade and hence a lower interest rate from the lending community. This allows the marketplace to increase approvals and hence conversion and also to more competitively price good borrowers. As our algorithm develops, we expect to be able to function as a standalone credit score.

How do you price your service for p2p lending marketplaces?

Our standard pricing is on our website at https://friendlyscore.com/page/pricing. We charge a subscription price to make the decision simple and easy for marketplaces. We are open to alternative, variable pricing models where they make more sense for the customer on a case-by-case basis.

Do you think your service will be more beneficial for marketplaces in developed countries or in developing markets or what factors indicate in which markets you could add most value?

We can service marketplaces in any market because, at the core, we are simply a data enrichment and machine learning platform for improved decisioning. We are however seeing steadily increasing interest from emerging market lenders which makes sense based on the following two macro factors that drives demand of our product:

1) Shortages of credit bureau data (much more prevalent in emerging markets). 2) High internet and social media penetration (much higher in developed markets but converging quickly). We will always be able to help developed market lenders access non-traditional borrowers (students, young professionals and foreign nationals). However, in developing markets where vast portions of the population lack financial history, and will soon be using the internet as much as anywhere else, we have a chance at bridging an accessibility gap in finance that unfairly applies to a large portion of the normal population. Continue reading →