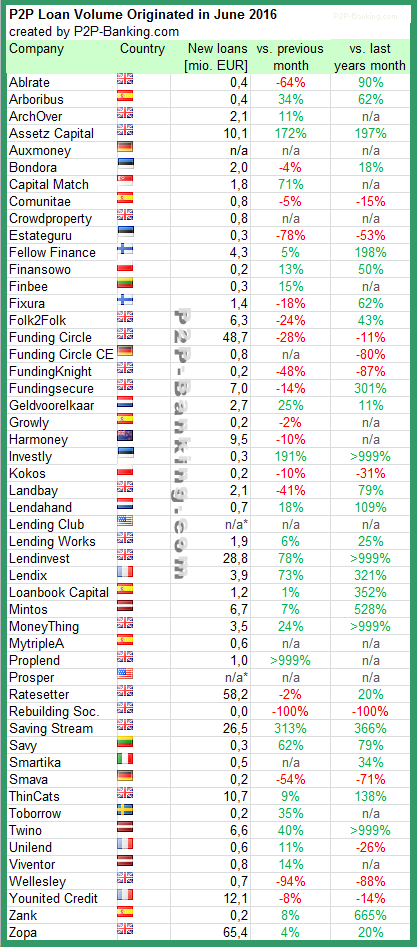

The following table lists the loan originations of p2p lending platforms in June. Zopa leads ahead of Ratesetter and Funding Circle. This month I added MytripleA. The total volume for the reported marketplaces adds up to 334 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Table: P2P Lending Volumes in June 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

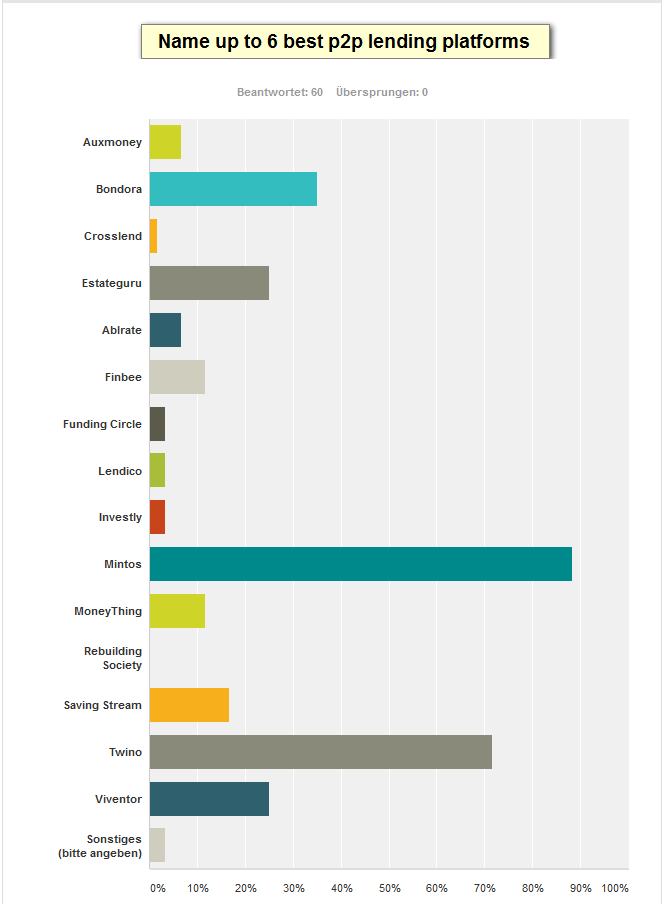

A poll conducted by P2P-Kredite.com among seasoned German speaking investors found, that many prefer p2p lending platforms outside the country they live in. After getting accustomed to the p2p lending concept and liking it, they are on a hunt for higher yields. Further supporting factors are the offered English language interface (a language most understand well), the easy transfer of funds within the Eurozone by SEPA payments and more features offered, e.g. most foreign platforms offer a secondary market, while currently none of the German marketplaces do.

Poll by P2P-Kredite.com, conducted in June 2016. 60 respondents. Each respondent could name up to 6 platforms. Note that Funding Circle refers to the German platform of Funding Circle, not Funding Circle UK.

Mintos (53 votes) and Twino (43 votes) lead by a wide margin in preference of the respondents, followed then by Bondora (21), Estateguru (15), Viventor (15), Saving Stream (10), Moneything (7) and Finbee (7). Exclusively baltic and british platforms rank best among the respondents. The choice of british platforms for German investors is limited though as some like Zopa or Ratesetter are open only to UK residents or require a UK bank account to sign up. Nearly all votes were cast before the Brexit decision. It remains to be seen how the UK platforms will rank in German investor preference in the future, given the more volatile GBP/EUR rates and the increased uncertainty for the UK economy.

Well that was a surprise. When I went to bed last midnight the news reported more indications for a remain vote than for a leave. Even with psephologists cautioning that the referendum is very hard to predict due to the lack of comparision data from earlier votes, it seemed to me that the outcome was likely pro EU.

While I had personally wished the Brits to stay in the Union they took a democratic decision and now the politicans have to act upon it to execute divorce.

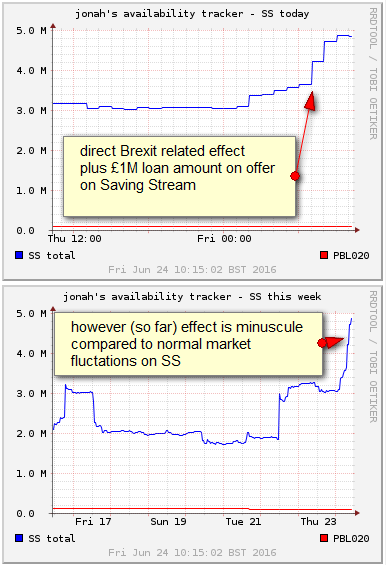

Awakening to the new reality I now have to assess what this means for my personal p2p investment strategy – as a foreign investor. Only a small portion of my p2p investment portfolio is invested in UK platforms (a substantial amount at Saving Stream, small amounts with Ablrate, MoneyThing and Rebuilding Society). The markets are in turmoil, and I have already taken the hit by the pound dropping sharply compared to the Euro this night.

Another effect is that the uncertainty is causing more investors to put up loan parts for sale – the effect is measureable on Saving Stream and currently accounts for a plus of approx. 1M GBP loans on offer there. Still this amount is very small compared to fluctations of liquidity levels due to other factors. For most loans this now means that there is a considerable delay in selling loans, due to queue size. However this could be cleared up quickly by one or two large loans repaying and the interest payout on July 1st.

(Source: jonah; own edits)

With Saving Stream and Moneything loans will depend highly on the development of the property prices. Some expect a drop in property prices. I think it is to early to tell if that will happen, but I think it is very likely that there will be slow down in new development activity while everbody waits to see what the outcome will be. This will affect the demand for bridging loans and thereby Saving Stream and Moneything to a cetain degree.

And then totally unpredictable there is the question how this new direction will effect the European economy as a whole and whether it might trigger a recession. While I am optimistic that it will not, there is an extreme amount of uncertainty and I have to consider that this might impact my p2p investments on continental European platforms.

For now I have decided that I will not deposit new funds on UK platforms (which I was planning to do) but will not withdraw funds either at the moment and will just keep reinvesting the proceeds. I see little point in selling off loans (would be hard right now anyhow as liquidity seems to dry off temporarily), and exchange the amounts back to Euro. That would guard me from further drops of the pound exchange rate, but I think it is not sure that the pound will fall into a continuing decline (even so that seems more likely than any rise in the pound rate vs the Euro).

For the continental platforms my strategy remains unchanged by the event, even though I think that the risks on some platforms have risen somewhat too in the mid-term outlook.

At a press conference this morning in Frankfurt, Michael Kotzbauer of Germany’s second largest bank Commerzbank and Birgit Storz of Main Incubator announced that the new platform Main Funders will launch next week. Main Funders is part of a broader digitalisation strategy of Commerzbank and the first project Commerzbank and Main Incubator built together. Main Incubator previously invested in several Fintech startups.

The aim of the new platform is to bring together SMEs seeking loans in the range of 200K to 10M Euro for up to 5 years and professional investors (institutional and large companies). Both will be already customers of Commerzbank and Commerzbank will make use of its regional sales force to bring borrowers onto the marketplace.

Borrowers will list their project n the platform, visible only to logged in investors, which in can browse the listings and select those that match their interests. Main Funders will assign credit grades to the loan requests and set the interest rate, taking into account that all loans will be unsecured. Since borrowers already have a credit history with Commerzbank, Storz says that the process, including the handling of the contracts, will take only a short time frame.

Main funders charges borrowers 0.45% of the loan amount multiplied with the duration and investors 0.2%.

Unlike on other platforms investors won’t have to ‘park’ cash to be able to invest but rather will be able to pay for funded loans after all contracts have been signed, an advantage to avoid cash drag.

Once the loan is fully funded, the loan will be serviced by a third company (not Commerzbank or Main Funders).

Main Funders says it is uniquely positioned compared to other p2p lending marketplaces in that it is able to facilitate very large loans and benefits from the relationship and trust Commerbank already has to target customers.

With Main Funders Commerzbank aimes to:

increase customer satisfaction

strengthen its competitive position

react to rgulatory requirements

create a basis that will allow it to build further innovative loan products upon

Storz declined to give a figure on the expected loan volume in the first year, saying it is important to be able to react and adapt quickly in such an innovative product offering.

Some questions in the press conference targeted whether Commerzbank is cannibalizing the own products and if there is no conflict of interest in the decision of whether to finance a loan itself or put it on the platform.

Kotzbauer said that Commerzbank is reacting to the wish of some of their customer to diversify financing options. The decision of whether to finance the loan request themselves or put it on the platform is made after consulting with the borrower on his financing needs and wishes and not discriminating by credit grades or other parameters.

Commerzbank is one of the first large banks in the world to have developed its own platform (together with its incubator). Other banks have taken the route to acquire lending startups (e.g. Barclay Africa Rainfin, Westpac with SocietyOne, or Banca Sella at Smava and Prestiamoci). Several banks are investing into consumer and SME loans on p2p lending marketplaces, especially in the US and the UK.

The initiative of Commerzbank is likely going to give a boost to awareness and credibility of p2p lending in Germany, even though it remains close to the conventional process with the restriction to existing customers and institutional investors. Continue reading →

This is a guest post by Kylie Greeff of whitelabelcrowd.fund

As one of the first countries in Asia to publish a regulatory regime, Malaysia is opening up to entrepreneurs, institutions and global operators to facilitate the ease of business credit through P2P lending. Ranked 18th on the World Banks’ Ease of Doing Business league tables, Malaysia is positioning itself as the conduit for global players to setup in Kuala Lumpur as gateway for serving P2P lending markets across Asia. Malaysia has one of the highest levels of financial inclusion in the world at 92 per cent and the country has taken advantage of mobile phones and online banking to expand access. The recently published Securities Commissions (SC) of Malaysia’s rules on the operation of a Peer-to-Peer platform sets out the minimum requirements for the compliant operation of a Loan based crowdfunding platform in Malaysia.

Given the recent publication of the SC’s rules, we have undertaken a comparison of the regulatory requirements imposed on Malaysian P2P platforms with their UK counter parts. The comparison highlights a number of differences first both in the rules that must be followed to operative a platform as well as the minimum standards imposed on operators operating the platforms in Malaysia. Whilst the comparison identifies a number of differences between the two bodies of regulation, this is not unexpected give the differences in maturity of the two markets. P2P in its earliest form began in 2005 in the UK, with the UK regulator announcing its intention to regulate the sector in 2013. The UK’s early P2P regulations were very similar to those now produced by the SC.

The SC in their production of their regulations have clearly done their research into the rules implemented by many platforms and regulators around the world in helping them draft their first guidelines, and have arguably used the UK’s regulations as their closest reference. A strategy that appears to have been widely adopted in their regulation of other financial markets as well. Below is a more detailed review of the UK and Malaysian regulation.

Capital Requirements

The first noticeable difference in the platform operator rules is the requirements by the SC for a platform to have a minimum paid-up capital of RM5 million (approx. £80,000). The UK regulatory body the Financial Conduct Authority (FCA) does not impose a minimum capital requirement for the start-up of a platform. The FCA instead imposes a capital adequacy Requirement (CAR) on platforms once they are trading and authorised by the regulator. A platform’s CAR requirement is based on the trading performance of the platform weighed against its loan book. The SC’s decision to incorporate a minimum capital level on start-up platforms could be seen as a possible reaction to the recent debate in the UK and USA about the possible implementation of Capital requirements on P2P platforms similar to those currently applicable to banks. This being said, the requirement of RM 5m is not prohibitively high and may not be seen by many market entrants as a particularly high barrier to entry, particularly by those supported by financial institutions familiar with far more prohibitive capital requirements.

Whilst the FCA does not have a start-up paid up capital requirement, recent feeling and expectation in the UK is that the FCA will potentially move to more onerous Capital Requirements similar to those imposed on many other financial institutions.

Investor Communication and Transparency

It is interesting to note that the SC has decided to enforce a specific requirement on P2P operators to use ‘an efficient and transparent risk scoring system’ and to ‘carry out a risk assessment on issuers’. The FCA imposes no such requirement on platforms, although the majority of platforms do incorporate a risk rating identification system for the benefit of lenders, the platforms do not openly publish their system or processes as these are closely guarded as valuable IP of the platforms. In the absence of a specific requirement to have an ‘efficient and clear risk scoring system’ the FCA would expect platforms to assess their market and client needs and ensure that they operate with in the FCA’s Principles for Business (PRIN), most notably in regard to risk modelling, Principles 5,7 and 9. It’s worth noting here that the SC operate similar principles in terms of Fund Management Companies, see Guidelines On Compliance Function For Fund Management Companies.

The language used by the SC of ‘efficient and transparent’ is surprisingly vague and may be intentionally left as such to allow platforms the space to develop naturally allowing the SC room to review practices and later set what they deem to be appropriate transparent and efficient processes.

In its list of Operator Obligations, the SC appears intent on ensuring that the platform operators acknowledge and respond to the need to maintain transparency between the investors and the Issuers and to make investors aware of the nature of their investment. This can be seen in rules 13.05 (d-f). Interestingly rule 13.05 (d) requires operators to ‘carry out investor education programmes’. The FCA again poses no requirement on platforms to ‘educate’ their investors but it does impose standards of disclosure and business conduct in its Handbook. The FCA expects platforms to take measures to ensure that they are open and transparent about the nature of the investment products it offers and that information is clearly displayed and prominent for investors (COBS 2.2.1 and 2.2.2).

Carrying out educational programmes in the form of video’s and blog post as well as informative events are a good way to encourage a higher level of customer engagement, but also goes a long way to building the trust of investors in the platform. Rebuildingsociety.com has benefited greatly from publishing a number of blogs about its journey, the types of investment it offers, the internal processes it uses to ensure the efficient and safe operation of the platform. Transparency is greatly valued by both the investors and the regulators.

Anti-Money Laundering and Financial Crime Prevention

As expected, the SC has incorporated the need and responsibility of platforms to ensure that they carry out sufficient Anti Money Laundering (AML) and Financial Crime (FC) Prevention practices as part of their normal operating processes. AML and FC are increasingly sensitive areas. Whilst the SC’s Guidelines on Recognized Markets does not set out specific instructions and guidance on the expected processes and levels of due diligence required by platforms, platforms should look to the SC’s ‘Guidelines On Prevention Of Money Laundering And Terrorism Financing For Capital Market Intermediaries’ which was developed from Section 83 and section 66E of the Anti-Money Laundering and Anti-Terrorism Financing Act 2001 (AMLATFA) and section 377 of the Capital Markets and Services Act 2007 (CMSA). This document sets out the SC’s expectations of platforms in relation to AML and FC prevention.

The SC’s guidelines on AML and FC prevention are broadly similar to those of the FCA set out in SYSC 6.3, in that advocate a risk based, profiling approach to AML and FC prevention processes and require firms to incorporate enhanced Due Diligence practices where individuals are profiled to be higher risk. Continue reading →

The following table lists the loan originations of p2p lending marketplaces in May. Funding Circle leads ahead of Zopa and Ratesetter. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Table: P2P Lending Volumes in May 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.