P2P lending marketplace Mintos crossed 50 million Euro in loans to both private individuals, as well as small and medium sized businesses after 18 months of operations. Mintos marketplace arranges loans from 14 non-bank lenders, which have joined the marketplace from the Czech Republic, Estonia, Latvia, Lithuania, and Poland.

According to funded loan volume, to date most money has flowed into loans in Latvia’s – 33%, Lithuania’s – 31% and Estonia’s – 23%.

‘All around the world, peer-to-peer lending concept is slowly replacing bank services from which the commercial banking sector is retreating. Today, banks no longer conduct the main mission of the financial system — connecting those postponing consumption with those who are consuming today, i.e. connecting savers and borrowers. Deposit rates are close to zero or even negative, while access to credit is limited. This increases the non-bank financial services market, which offers consumers easy, convenient and affordable services,’ emphasizes Mintos CEO and co-founder Martins Sulte, predicting that by year end, investors through Mintos will have financed EUR 100 million in loans. Continue reading →

P2P-Banking.com Interview with Laimonas Noreika, CEO of Finbee

You launched Finbee a year ago. Can you sum up the major developments since?

More than 3,000 investors have issued 2M EUR worth of loans via FinBee and none of them lost any money due to a default and our compensation scheme. We are very proud for this result. We have a reliable and highly skilled team that has built a company that is constantly growing. We are in full legal compliance with existing regulation and are constantly working on developing new products and features for our investors and borrowers.

What were the biggest challenges in this first year?

P2P lending is a relatively new concept in Lithuanian lending market, so raising awareness and overcoming scepticism was one the biggest challenges that we’ve faced from day one. Also, when we started to expand, building a team that can deliver results while maintaining highest standards was also time consuming. From technical perspective, learning the dynamics of supply and demand in FinBee auction was also something that we put a lot of effort to.

In your opinion, which 3 most important skills does a CEO need to successfully lead a fintech startup?

In my personal opinion, a key feature that a CEO has to be experienced in is team building. Even the most outstanding CEO will not be able to achieve much without a great team. A great manager has to have a diverse experience in corporate governance, finance, legal matters, marketing and IT. Also, I would like to emphasise, that simple and transparent communication is vital for a CEO.

Are collection and default figures in line with the expectations & projections you had a year ago?

Current default figures are better that we expected and projected. We expected to operate with 8 to 10 percent of non-performing loans. Currently we have 2.25 percent (it worth noting that we consider a loan to be non-performing when two monthly instalments are missed, that is when loan is 60+ days late). We also project 40 percent recovery of non-performing loans. So we expect 4.8 – 6 percent losses after recovery. Having in mind that investors now invest on 26 percent interest rate on average, they can expect 20 percent returns even without our compensation fund.

We achieve this by minimizing the chance of default with wide range of measures. For example, we check every single borrower using more criteria than is required by regulation. Also, we meet each and every one of them personally. We confirm only 7 percent of loan requests and only then pass them to the investors. Continue reading →

Silver Bullion Pte Ltd in Singapore reported today, on the anniversary of the launch of their bullion secured peer-to-peer(P2P) loan platform, that the platform has funded over S$11 million across more than 400 successfully matched loans. There were zero occurrences of borrowers defaulting on their loans. One hundred percent of lenders, with loan tenures expiring within the first year, received their principle with interest on time.

Launched on 5th August 2015, Silver Bullion offers a p2p marketplace that allows borrowers to obtain a loan using physical gold and silver bullion as collateral. This gives lenders, seeking a good rate of return, confidence that their investments are safe.

Silver Bullion’s CEO, Gregor Gregersen, commented: ‘The first year results of our P2P loan platform shows that owners of physical gold and silver like to have the option to be able to borrow short term funds at good rates with the bullion that they store with us. Now, they are able to reinvest with the borrowed funds whilst continuing to own bullion and benefit from rising gold and silver prices.’

P2P-Banking.com conducted an interview with Gregersen earlier this year.

Due to the safety that Silver Bullion’s loan platform gives to lenders, 72% of the matched loans were initiated by borrowers. The company has seen more than 30 loans matched consistently each month since March 2016 – a rate of more than 1 matched loan per day. Interest rates across all loan tenures currently hovers between 2.5% and 4.5% per annum. Unlike unsecured P2P lending platforms, loans matched by Silver Bullion’s lending platform are fully backed by physical gold and silver. Loans with tenures longer than 6 months begin with a collateral-to-loan value of 200%. The exceptions are loans with the 1 month tenure which have a lower collateral-to-loan value of 160%.<

Borrowers’ collateralized bullion is stored at Silver Bullion’s vault, The Safe House. They are covered by one of the most comprehensive insurance policies in the industry that also insures against inside jobs and any unexplained losses.

The following table lists the loan originations of p2p lending platforms in July. Zopa leads ahead of Funding Circle and Ratesetter. Assetz Capital and Lendinvest achieved a big surge in volume. The total volume for the reported marketplaces adds up to 341 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in July 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

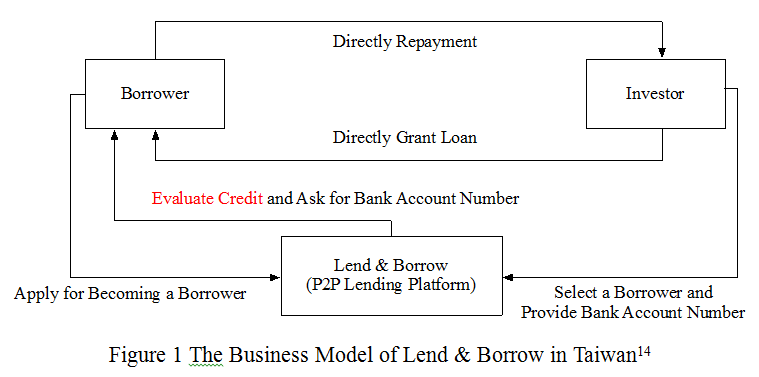

This is a guest post by Hungyi Chen, Ph.D. candidate at the Graduate School of Law, Nagoya University. He is researching alternative finance in East Asia.

1. Relevant Background

Internet finance, including (1) online stored payment by non-bank, (2) crowdfunding and (3) peer-to-peer lending becomes hotly debated issues in Taiwan recently. To boost the development of financial innovation, the regulation of online stored payments by non-banks was already implemented on January 2015 after discussions and debates between financial authority and platforms. Besides, a regulatory framework for equity-based crowdfunding has also been enacted in the end of April 2015 and amended in the early of January 2016.

In order to encourage and accelerate the development of fintech industry in Taiwan, the financial authority, Financial Supervisory Commission (FSC) of Taiwan, has published Fintech Development Strategy White Paper on May 2016[i]. One of main goals is evaluating the possibility of introducing the mechanism of P2P lending into Taiwan’s capital market and providing a regime for regulating this industry.

Some business models of P2P lending are forbidden due to conflict with The Banking Act[ii] in Taiwan. Recently, it is considered to be introduced in Taiwan and evaluated by the recently established project team of the financial authority in Taiwan, Financial Supervisory Commission (FSC)[iii]. Despite the fact that the attitude toward P2P lending industry of financial authority in Taiwan is still vague, as of July 2016 there are three P2P lending platforms already providing their services in Taiwan, including Lend & Borrow[iv], Wow88[v], XiangMinDai[vi]. They have tried to design their business model to avoid potential legal risks. For better understanding of the P2P lending industry, this article tries to provide a brief regulatory overview of Taiwan in following part.

2. Regulatory Overview of P2P lending

Currently, there is no any specific regulation toward this industry in Taiwan. Recent official document[vii], indicate that the business model of P2P lending in Taiwan should avoid to involve in any activities of accumulating capital from general public or issuing any securities. XiangMinDai, a P2P lending platform in Taiwan, has analyzed by FSC of Taiwan. The former chairman of FSC of Taiwan, Ms. Wang, has stated that ‘…the business model of XiangMinDai is majorly providing services of debt transaction, which does not involve in activities of depositing or charging fund. Accordingly, it is not the regulatory scope of FSC at this moment…[viii]‘

Although there is no any financial regulation of P2P lending in Taiwan, Banking Bureau of FSC has issued a statement[ix] on April 14, 2016, pointing out some legal compliance issues for P2P lending platforms, including (1) platforms should not involve in issuing any securities, (2) ensure privacy of customers, (3) activities of deposit and store-value business without licenses are forbidden, (4) illegal ways of debt-collection is forbidden.

Within 2 weeks, Banking Bureau of FSC, announced another statement[x] for supplement, indicating that (1) the interest rates of the case on the P2P lending platform is 30.15%, which may be illegal according to Criminal Act in Taiwan[xi], (2) legal concern of breaking the law of Multi-Level Marketing Supervision Act[xii] and Fair Trade Act[xiii]. Continue reading →