The central bank of Germany, Deutsche Bundesbank, has published a discussion paper on the role of p2p lending in the consumer credit market written by Calebe de Roure, Loriana Pelizzon and Paolo Tasca. The study analyses data of German p2p lending marketplace Auxmoney.

Research Question

In recent years, we have begun to observe the growth of the internet economy, which has progressively led to “crowd-based†platforms and the direct matching of lenders and borrowers. Via peer-to-peer (P2P) lending platforms the decision process of loan origination is given into the hands of private lenders and borrowers. This paper investigates how the P2P lending market fits into the credit market and specifically aims to answer the following questions: Why do retail consumers look for P2P financial intermediation? Are the interest rates charged by P2P lenders in Germany higher than those of banks? Are P2P loans more risky than bank loans? Are internet-based peer-to-peer loans substitutes for or complementary to bank loans?

Contribution and Results

The paper shows that loans channelled via P2P platforms involve higher interest rates than loans channelled via the traditional banking sector. They are also riskier than those of banks. However, when adjusted for risk, the interest rates are comparable. Moreover, analysis of the different segments of the bank credit market and P2P lending shows that, after having controlled for interest rate and risk differences, the bank lending volumes are negatively correlated with the P2P lending volumes. Our finding suggests that high-risk borrowers substitute bank loans for P2P loans since banks are unwilling or unable to supply this slice of the market. Continue reading →

UK app Pariti has integrated loan offers by p2p lending marketplace Zopa into its app allowing users to check whether they could get a better rate for their debt. User can apply for a debt consolidation loan directly from the app. Pariti is using Zopa’s API to access data for the offers.

The Pariti app, which claims 70,000 users, connects to a user’s existing bank accounts, analyses their spending history, and helps them set a target for improvement.

The Zopa integration enables Pariti users to discover if they could be paying less for their debt without affecting their credit score, and to apply directly for a consolidation loan through the Pariti app.

“UK consumers are getting ripped off by credit card companiesâ€, Pariti founder Matt Ford comments. “Introductory offers, confusing fees, and unsuitable products have meant that people are paying far too much to borrow, and are getting stuck in high-cost debt. The product integration with Zopa allows us to proactively help reduce their cost of borrowing and pay off debt faster.â€.

Zopa’s CEO, Jaidev Janardana, says: “The API is already being used in online retail, and the implementation of our Pariti partnership marks its first use in a fully integrated, in-app application process. He added: “Our own research shows that many consumers could save money by swapping out expensive credit card debt for a lower-priced Zopa loan, and by working with Pariti we are able to offer this service to even more consumers.â€

The European online alternative finance market, including crowdfunding and peer-to-peer lending, grew by 92 per cent in 2015 to €5.431 billion, according to the results of the 2nd Annual European Alternative Finance Industry Survey conducted by the Cambridge Centre for Alternative Finance at University of Cambridge Judge Business School, in partnership with KPMG and supported by CME Group Foundation.

The report released today, titled “Sustaining Momentumâ€, had the support of 17 major European industry associations and research partners, and was based on data from 367 crowdfunding, peer-to-peer lending and other alternative finance intermediaries from 32 European countries – capturing an estimated 90 per cent of the visible market. P2P-Banking.com is one of the research partners.

The United Kingdom was by far the largest in Europe at €4.4 billion, followed by France at €319 million, Germany at €249 million and the Netherlands, €111 million. Other large European markets include Finland with €64 million, Spain at €50 million, Belgium at €37 million and Italy at €32 million. The Nordic countries collectively accounted for €104 million, while Central and Eastern European countries registered a total of €89 million.

Excluding the UK, the European alternative finance market grew by 72 per cent from €594 million in 2014 to €1.019 billion in 2015.

“Although the absolute year-on-year growth rate slowed by 10 per cent†(from the 82 per cent growth excluding the UK between 2013 and 2014) the industry is still sustaining momentum with substantive expansion in transaction volumes recorded across almost all online alternative finance models,†the report said.

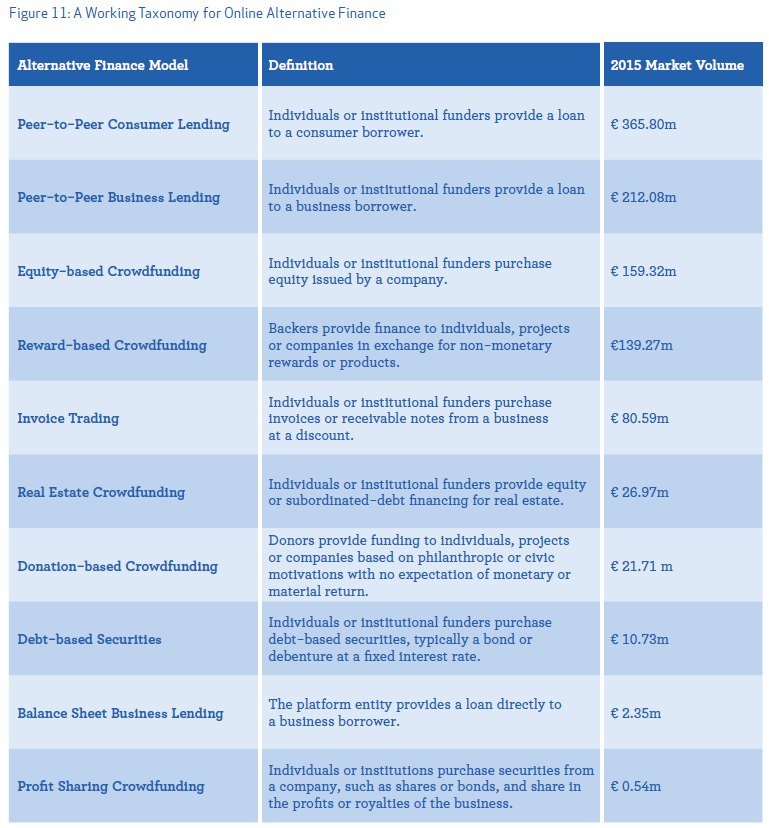

Peer-to-peer consumer lending is the largest market segment of alternative finance, with €366 million in Europe in 2015. Peer-to-peer business lending is the second largest segment with €212 million, with equity-based crowdfunding in third with €159 million and reward-based crowdfunding fourth at €139 million.

Table: Figure 11, page 31 of ‘Sustaining Momentum’, volumes by market segment in Europe 2015 (outside UK)

Among other findings:

Estonia ranked first in Europe in alternative finance volume per capita at €24, followed by Finland at €12 and Monaco at €10 outside of the UK.

Online alternative business funding increased by 167 per cent year-on-year to €536 million raised for over 9,400 start-ups and SMEs across Europe.

Institutionalisation took off in mainland Europe in 2015, with 26 per cent of peer-to-peer consumer lending and 24 per cent of peer-to-peer business lending funded by institutions such as pension funds, mutual funds, asset management firms and banks.

Across Europe, perceptions of existing national regulations in alternative finance are divided. About 38 per cent of surveyed platforms felt their national regulations for crowdfunding and peer-to-peer lending were adequate and appropriate, 28 per cent perceived their national regulations to be excessive, and a further 10 per cent said current regulations were too relaxed.

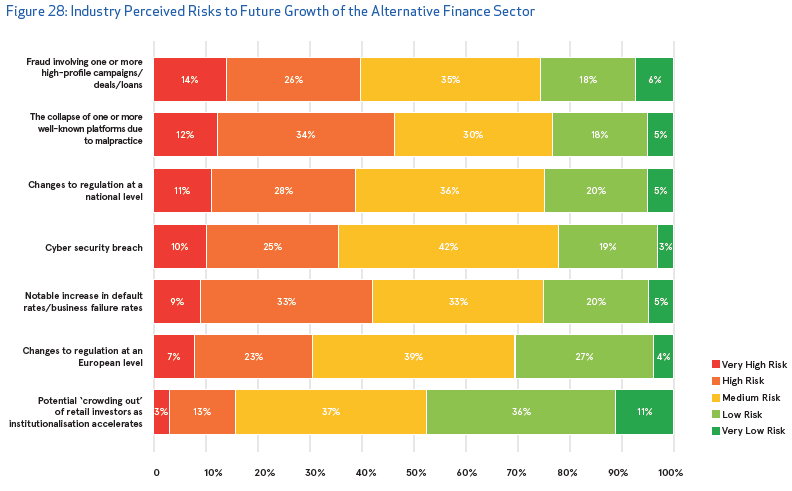

The biggest risks perceived by the alternative finance industry are increasing loan defaults or business failure rates, fraudulent activities or the collapse of platforms due to malpractice.

Chart: Figure 28, page 47 of ‘Sustaining Momentum’, risks to the industry as perceived by the polled platforms

Robert Wardrop, Executive Director of the Cambridge Centre for Alternative Finance, said: “European alternative finance transaction volume increased to more than €5 billion in 2015, with volume outside of the UK market exceeding €1 billion for the first time. The European alternative finance industry is still small, however, and the slowing rate of growth during the year is a reminder of the risks the industry must contend with in order to transition from a start-up to a sustainable funding channel within the European financial services ecosystem.â€

Irene Pitter, Global Executive, Banking & Capital Markets and member of the FinTech Leadership Team at KPMG, said: “This report shows that the alternative finance sector is set to continue to grow and mature. 2016 marks a significant year for ‘alternative finance’ in Europe as the market demonstrates clear signs of continued strong growth and increased maturation in the sector as a whole. European activity, excluding the UK, showed solid growth of 72 percent last year and demonstrated client demand for alternative finance solutions even in the smaller EU countries.â€

Rumi Morales, Executive Director, CME Ventures, said: “The prominent feature of financial technology is that it is truly borderless. No one country is harnessing alternative financial markets or business models to the exclusion of any other. Rather, from the UK to Estonia and from Finland to Monaco, the entire European continent is experimenting and expanding upon innovations that can provide greater access to capital and financial services to more people than ever before.â€

The following chart lists the loan originations of p2p lending marketplaces in August. Funding Circle leads ahead of Ratesetter and Zopa. Zopa yesterday announced an interest rate cut of 0.2% following the BoE decision to lower interest rates. Zopa warned that new deposits would be slower to lend out, and will take 10 days on average, as it faces a shortage of borrowers. Zopa used to accept 1 percent of applicants, but now approves on 20 percent.The total volume for the reported marketplaces adds up to 336 million Euro. I track the development of p2p lending volumes for many countries. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in August 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Finnish p2p lending marketplace Fellow Finance now also offers SME loans.

In the service, companies can apply for financing for growth and investments from Fellow Finance’s investors.. Fellow Finance has intermediated loans for consumers through its service for 40 million EUR during a period of 12 months. Opening a financing service for companies stems from the needs of Fellow Finance customers and with the new Crowdfunding Act established legal framework for the operation has been established.

I checked the marketplace. Right now there is one loan request for 70,000 Euro at 11% interest rate, 60 month term listed.

‘We have already received requests and inquiries from our clientele for a long time about whether we could also start financing companies. Many of our customers are either current or former entrepreneurs who understand the financing challenges faced by Finnish SMEs in different phases of business. They have a strong desire to finance other entrepreneurs and offer promising projects the chance to really take off’, says Jouni Hintikka, CEO of Fellow Finance. Continue reading →

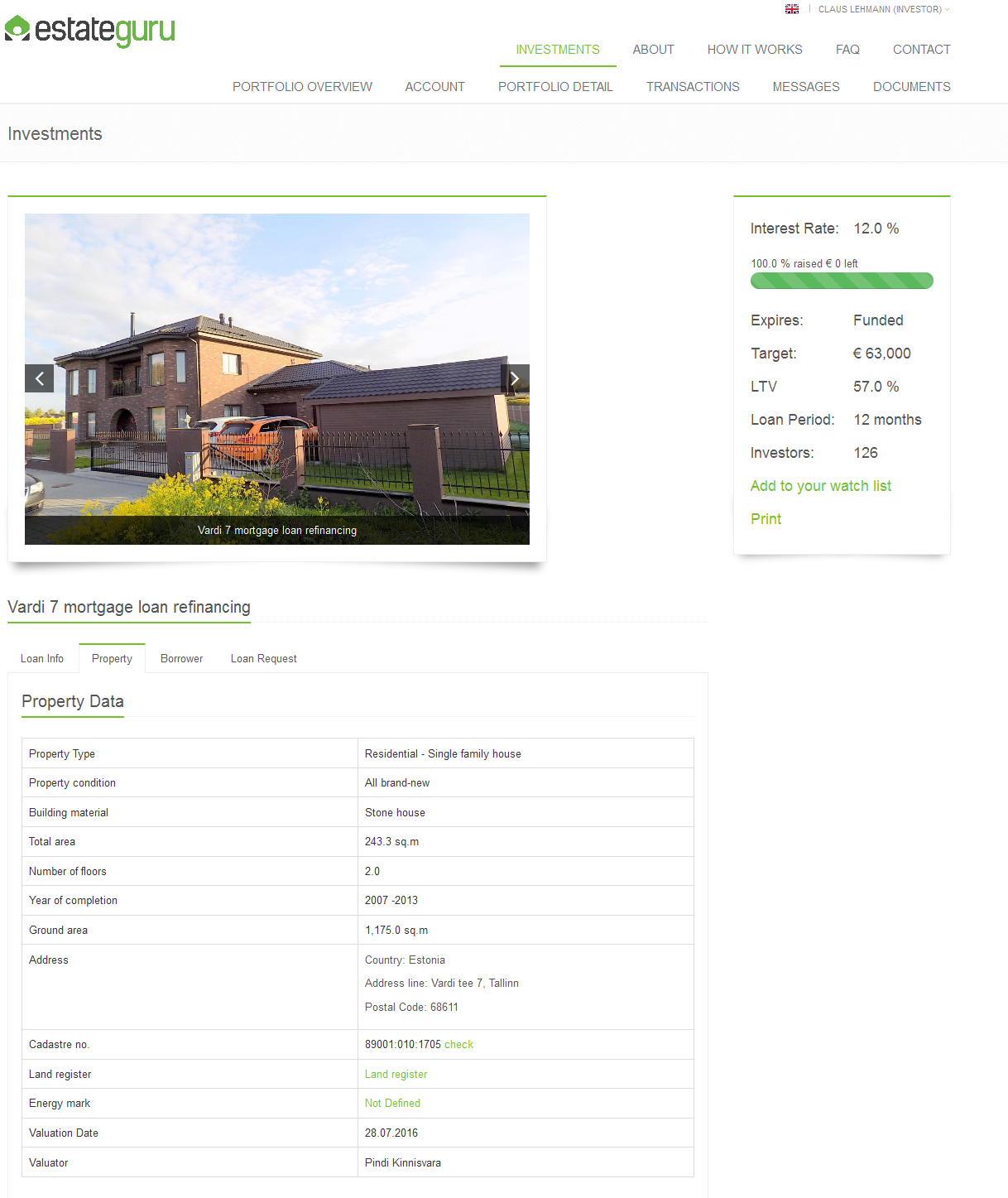

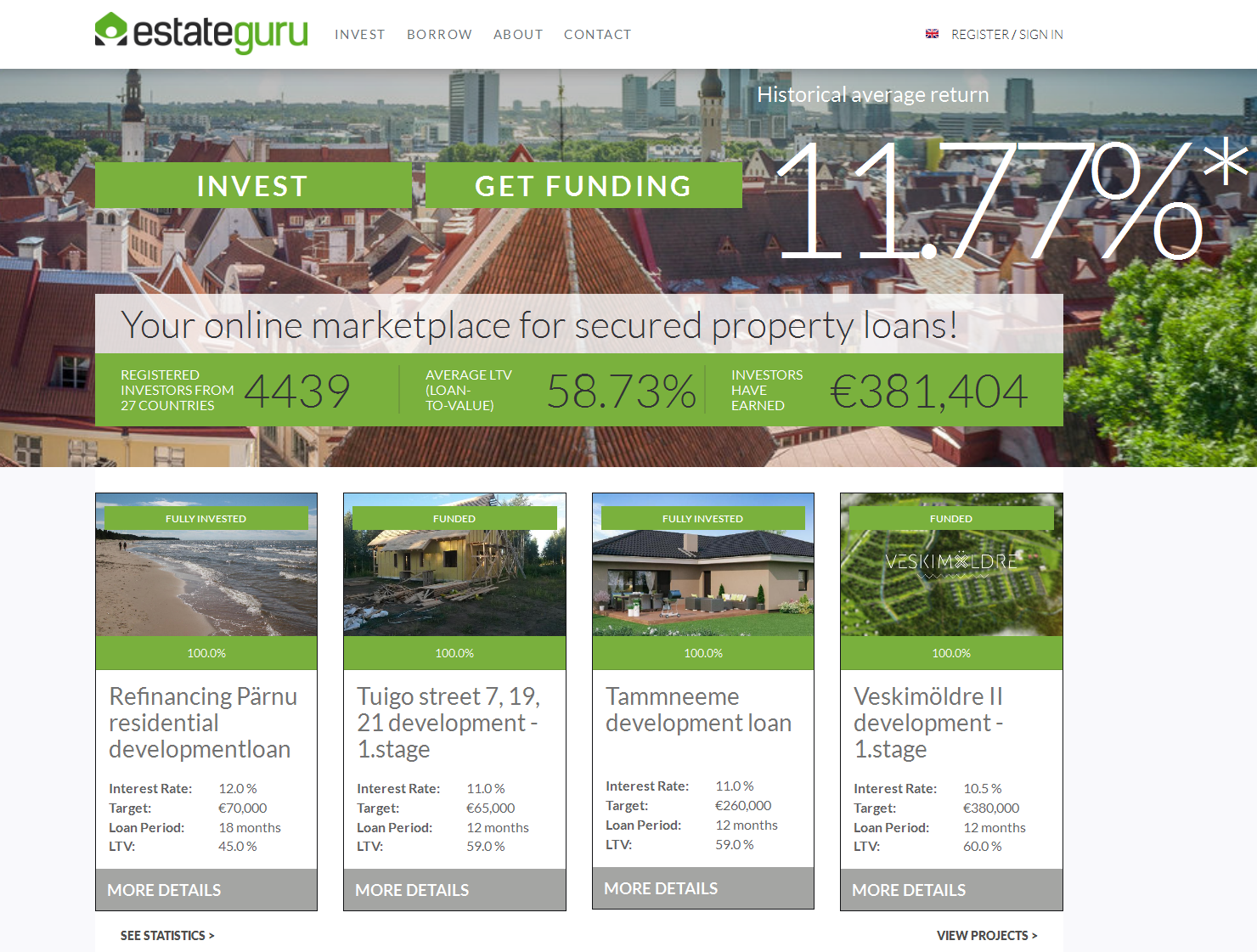

Estateguru is a p2p lending marketplace in Estonia focussed on bridge loans to property developers in Estonia. Since the launch in 2014 Estateguru has facilitated a loan volume of more than 10 million Euro in a total of 65 loans. The loans are secured by 1st or 2nd rank mortgages. Typical interest rates range from about 9% to about 12%. Some of the loans pay monthly interest, while for others the interest is paid at the end of the loan term. The minimum bid amount is 50 Euro.

Estateguru provides appraisal reports for the security. Estonia is highly advanced in digitization – this allows Estateguru to provide direct links to the official records in the land register for the plot.

Example of an Estateguru loan listing (shortened, click to enlarge image). There is more information about the loan, the security and the borrower in the other tabs

I have invested in a couple of loans over the past years and the handling is smooth. Two loans are repaid (one early) and the other loans are running on schedule. Other investors report that there have been no defaults yet, only some loans where the payment came in late for a couple of days (or a few weeks at max.). Unlike other platforms, Estateguru sends no updates about the loans.

Many investors keep some cash in the Estateguru account in order not to miss out, when new loans appear. Smaller new loans usually fill within hours. Investors can opt for a notification email, that is sent when new loans arrive. However tiny loans (< 40,000 EUR) are sometimes 100% funded by the time the email arrives. There is no autoinvestment feature / prefunding facility. Estateguru does not have a secondary market, but many loans are only for 12 or 18 months term.

Estateguru is open for investors from all over Europe (actually the EEA). If you are inside the Eurozone investments are fast via SEPA transfers. If you live outside you should consider using Transferwise or Currencyfair to avoid high bank fees and get a better currency exchange rate.

Bonus: If you sign up using this link Estateguru will credit you 0.5% cashback on all investments you make in the first 90 days.