German credit broker Smava today announced that it has closed a 34 million US$ investment which was led by growth investor Runa Capital, with additional participation from Verdane Capital and mojo.capital. Runa Capital is a venture capital firm with other investments in Zopa, Lendingrobot and Lendio. Verdane Capital is a Scandinavian private equity firm. Existing investors including Earlybird Venture Capital also participated in the investment. This series C round follows the previous round in 2015 which was 16 million US$. In total Smava, which launched in 2007, has raised about 64 million US$ so far.

Smava connects private borrowers with a broad selection of banks and private investors on its marketplace. Smava offers personal loans ranging from 1,000 to 120,000 Euros. Continue reading →

P2P lending marketplace Prosper today informed investors via email, that it will close down the secondary market, effective October 27th. Prosper does not operate the secondary market itself, but uses FolioFn, operated and maintained by FOLIOfn Investments, Inc., a registered broker-dealer.

The announcement email reads:

A Message from Prosper and Folio Investing

Dear …,

We are writing to let you know that as of October 27, 2016, Prosper will no longer offer the Folio Investing Note Trader platform, the secondary market for Prosper Notes. Prosper has found over time that very few investors are using the secondary market and, as such, has made the decision to no longer offer this service. We apologize for any inconvenience that this causes. Prosper remains committed to its retail investor clients and to providing them a great experience.

Here’s what this means for you: The secondary market trading service will be available as normal until end of day (5:30 pm PST) October 19, 2016. After that time, any new orders to list Notes for sale will not have sufficient time to be completed and processed before the site becomes unavailable to users at the end of day (5:30 pm PST) on October 27, 2016.

Once the secondary market trading service is terminated, you will not be able to sell Notes that you own, and you will need to hold them to maturity.

If you have questions about your Notes or the wind-down of the Folio Investing Note Trader platform, please contact Prosper customer service at 877-611-8797.

Thank you.

Prosper and Folio Investing

Prosper has not disclosed usage numbers of the secondary market in the past, but volume traded is perceived to be low and this is also stated in the email. One speculation is that Prosper decided to close the secondary market to cut costs.

My feeling is that this will deliver a blow to the attractiveness of the Prosper marketplace for retail investors. Even if many investors have choosen not to use the marketplace (which several report does not have a very good user interface) the fact that there is a marketplace delivered some assurance that they could exit at least a larger portion of their portfolios should the need for liquidity arise. Also a one month notice seems to me rather short, given that loans can run up to 60 months and with the changed perception the prices could sink (lower markups, higher discounts) in the remaining month of trading as the number of investors wishing to use this last chance to sell will rise in my view, while the number of investors buying will at best stay stable. Continue reading →

I decided to try out another UK p2p lending service. Bondmason is not a marketplace facilitating loans itself, but rather acts as intermediary steering and automating investments for the users. Bondmason wants to offer an easy way to automatically invest and diversify. To allow this, I need to hand over full control to Bondmason. In return Bondmason projects a target return of 7% after fees and bad debt. Note that the target return is not guaranteed.

Getting started was easy. I deposited the minimum amount of 1,000 GBP. Since I am in the Eurozone I used Transferwise to do this in order to avoid high bank fees. For higher amounts Currencyfair can be cheaper. After two days Bondmason notified me via email that my money arrived. After login I saw that the service already invested 180 GBP in the first 9 selected loans.

Bondmason invests in sme loans, property loans and invoice discounting. Currently Bondmason is using 19 marketplaces, but does not disclose which ones are used arguing IP considerations. Some of them do not seem “typcial” p2p lending marketplaces, as one mentioned example is Fiduciam. As in investor I am only shown nominal interest rate, type of loan and term.

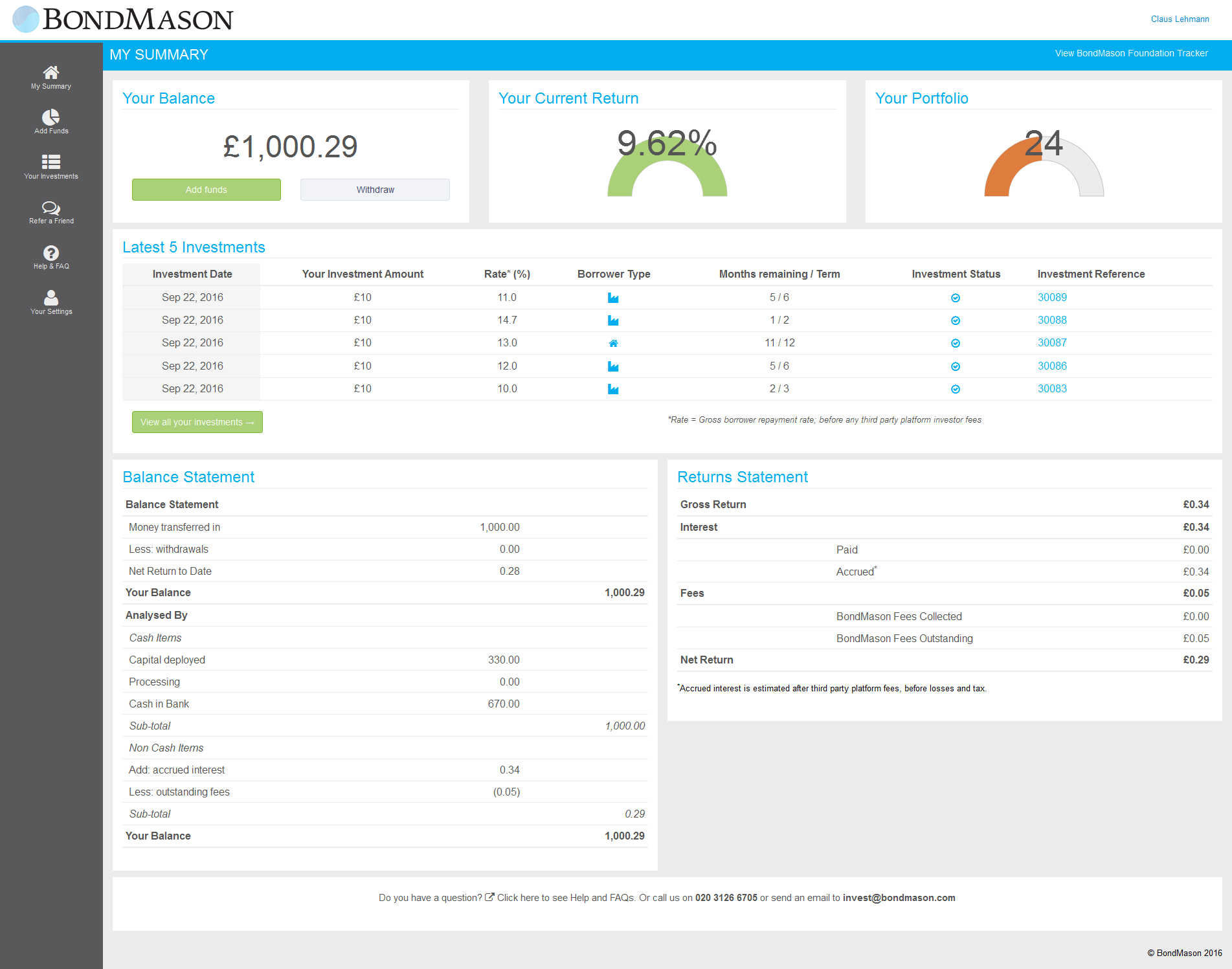

My Bondmason dashboard on day 6 after start (click to enlarge)

The information provided is rather minimalistic, there are really only two views. The dashboard view (see above) and the investment view (see below). Regarding parameters there is only the choice whether to reinvest and the diversification setting, which lets me select a maximum of 2% or 1% investment concentration. There is no account statement.

So far Bondmason invested 330 GBP (or 33%) of my cash. The selected loans have nominal interest rates ranging form 6.0% to 14.7% and terms between 1 and 13 months. As an investor I have to fully trust the loan quality and loan selection provided by Bondmason to deliver the promised target return. Since (so far) all my loans are bullet loans, it will take me even longer to find out how high bad debt levels will be in reality. But that’s what this test is for and I’ll continue to report on my Bondmason experiences.

This page gives some more information on the approach of the algorithm in loan allocation. Bondmason targets one third loans with less than 60 days, one third with up to 12 months term and one third over 12 months term for my portfolio. Continue reading →

Peer-to-peer lending platform RateSetter has published its 2015-16 accounts, showing that it increased revenues from 12.6M to 18.5M GBP over the year. The company made a pre-tax loss of 4.9M GBP, compared to a pre-tax profit of 476K GBP for the preceding year. The company’s results are in line with expectations set out at the start of the year and reflect the decision to charge more fees over the lifetime of loans rather than upfront and a planned increase in investment back into the business.

Loans under management increased by 70 per cent, from 341M GBP on 31 March 2015, to 581M a year later, while the number of active investors grew from 18,608 to 31,036 over the same period. Today these figures stand at 640M GBP and 36,310 respectively – with a 70 per cent increase in new active investors in the period since the EU referendum compared to the same three months last year.

RateSetter made a profit for the years ending 31 March 2014 and 2015.

One of the main investment considerations for the money raised in 2015 from a consortium of investors including Woodford and Artemis was to alter the timing of receiving income: in 2015 RateSetter started to charge a greater proportion of its fees over the lifetime of loans rather than purely up front when loans are written. This creates a more sustainable recurring income stream as more money comes in over the term of loans, reducing pressure to lend in order to generate revenue when credit conditions are poor. Importantly, it also aligns RateSetter’s interests with those of its investors as it provides a financial incentive to only approve loans which perform. If all fees had been taken upfront when loans were written, rather than charged over the lifetime of loans, RateSetter would have recorded a pre-tax profit in 2015-16. Continue reading →

BLender, a p2p lending company from Israel, today announced its global expansion, beginning with new offices in Milan, Italy and Vilnius, Lithuania that will serve customers in Italy and the Baltics. The Israeli-based company delivers a P2P lending platform with a proprietary consumer credit rating system designed for territories without credit bureaus or traditional consumer credit information. BLender is a cloud-based platform that was built to work in a wide range of markets and languages.

In Italy the platform charges borrowers a 4.5% origination fee and investors 1.5% of each repayment (principal and repayment). Compared to other marketplaces these fees are in the higher price range. The fee for selling a loan on the secondary market is 0.45%.

BLender has experienced exponential growth since its launch in 2014 and has already provided approximately 12 million USD in loans. The company will continue expanding its global operations into territories that are craving consumer credit. In 2017, BLender plans to launch operations in Africa, Latin America and other European Union (EU) countries.

“Offering multi-national P2P lending has been our vision since BLender’s establishment,†said Dr. Gal Aviv, CEO, BLender. “Since our Israeli launch in 2014, we have built the foundation, infrastructure and technology to enable BLender to operate in the global market, so we will be able to face operating, cultural, technological, regulatory and taxation challenges.â€

With the expansion into Italy and the Baltics, BLender is enabling users to lend and/or borrow across countries, making financial borders a thing of a the past, says the service.

“BLender identified a credit gap in countries where the supply of consumer credit is insufficient for the populations’ needs and is priced very high, and a gap in other countries where the savings options have very low or even negative yield,†said David Blumberg, founder and managing partner, Blumberg Capital, a San Francisco-based venture capital firm that led BLender’s last funding round. “BLender’s multi-national lending options mediate this credit gap by creating a meeting ground between borrowers from countries that lack consumer credit, to lenders from countries where the yield on their savings in insufficient. We support and strongly believe in the vision, management capabilities and business potential of the BLender team.â€

Investors on the BLender platform will earn predicted interest rates of 5-6% annually. The safeguard fund acts as an additional layer of protection to the lenders in case of a default. BLender’s default rate is approximately 1% before activating the safeguard fund. Thanks to the SafeGuard fund, the effective default rate is 0% says the service. BLender also offers ReBlendTM, BLender’s secondary market that offers the lenders the option the trade their loan portfolios and enjoy liquidity.

Recently BLender was chosen to participate in the exclusive ELITE program of the UK Stock Exchange that finds and nurtures companies with the potential for an IPO. As part of the program, BLender receives the guidance of the program’s experts for two years that help promote the company’s activity.

Furthermore, the company was selected as one of the most promising Fin-Tech companies in the world for 2015 by the accounting firm – KPMG, and also by the United Kingdom Trade and Investment Department.

The multi-national expansion was done in collaboration with KPMG.

LendIt Europe (use discount code Wiseclerk16VIP for 15% rebate) will be held in London on October 10-11, 2016. LendIt is the major conference for the p2p lending industry with venues in New York, San Francisco, China and London. I attended Lendit London the last 2 years and can recommend it to anybody in the p2p lending industry. You can read my Lendit Recap 2015 here.

This year the location is the InterContinental London – The O2. For the second year running, LendIt is partnering with the lending association of major UK p2p lending marketplaces – Peer-to-Peer Finance Association (P2PFA). More than 1,000 attendees are expected to join what is billed to be the most in-depth conference in the industry. 150 speakers across six tracks will be tackling all the biggest issues in the lending industry, including regulations, credit and underwriting, international developments, institutional investment, consumer lending, small business lending and property lending.

“LendIt is delighted to be back in London for the third annual LendIt Europe event and partnering with the P2P Finance Association again,†said Peter Renton, co-founder of LendIt. “As the lending industry changes rapidly, LendIt is committed to remaining the leading community where all lending platforms, investors and service providers can gather to network, learn and grow the industry together.â€

There are only a few days left to register for LendIt London at the current ticket price, before the price goes up. If you use discount code Wiseclerk16VIP at signup you get 15% off.

I’ll be staying at the Sunborn Yacht Hotel. If by chance you are there too, we could have a drink and chat. See you there!