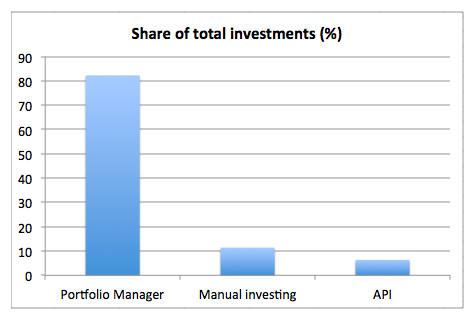

P2P lending marketplace Bondora announced that it will pull the primary marketplace from the user interface effective November 1st. This removes the chance for investors to manually invest on selected loans, leaving the options to either use the automated portfolio manager or to use the API.

Earlier this week Bondora provided this statistic showing that the majority of investments is done through the portfolio manager. This is another of the many changes the Bondora marketplace underwent in the past years.

The announcement email sent today, reads:

On November 1, 2016 we will remove the Primary Market view from the user interface.

What does this mean?

In recent months it has become clear that the Portfolio Manager offers greater efficiency through automation compared to manually investing. The increasing benefits of Portfolio Manager are the result of recent updates to the funding process, which optimize speed. Moving forward we will continue to focus efforts on further improving Portfolio Manager, Bondora API, Secondary Market and the reporting features available on the platform.

Why is Bondora removing the Primary Market from the user interface?

Bondora is removing the Primary Market from the UI because the speed of our popular automated option meets the investing and borrowing needs before manual investing can take effect. Our process improvements have created an environment where almost all loans are funded before they become visible in the UI. As a result, the Primary Market is most of the time empty.

This scarcity is due to the fact that when a loan enters the market it is open to bids for 10 minutes. After the 10 minutes expire the loan is closed. Our internal analysis and reporting shows that almost 100% of loans are funded within this brief window of time. Therefore, there is little reason to hold loans open any longer, as doing so would create unnecessary delays.

What should API users do?

Removing the primary market from the user interface does not change anything for Bondora API users. However, API users should review their settings for polling loans from primary market and reconfigure their settings to match the changes to the current funding process. We recommend that the polling of new loans be set to once a minute. Our API allows for speeds up to one query per second, however such rapid polling is also not recommended.

Finbee is a small p2p lending marketplace for consumer loans in Lithuania (see earlier coverage). I have been using it as an investor for a little over a year now. My strategy on Finbee is different than on other marketplaces. I invest loans mainly with the purpose of trading in mind, that means on Finbee I don’t plan to hold the loan parts to maturity

Finbee secondary market basics

Loans can be offered at a discount, par or premium

Seller pays 1% fee upon successful transaction

Only loans with at least one repayment can be offered. This means I cannot sell loans directly after acquiring them on the primary market (no flipping). I have to hold each loan for at least 30 days.

Late loans and loans in arrears can be offered. Loans that are 60+ days overdue cannot be listed for sale.

Maximum listing duration is 20 days; thereafter seller can relist

Buyers can buy instantly at ‘buy now’ price or make a bid, hoping that no other buyer overbids them in the remaining listing duration (or pays buy now price)

Finbee parameter UI for selling loan parts on secondary market

How I select loans on the primary market

I mostly invest in ‘D’ loans (that is the most risky rating) with long loan durations (>36 months) and high interest rates. The average interest rate in my portfolio is 32%, the maximum 35%. My reasoning for this choice is that these loans allow high markups and still offer an attractive buyer yield (XIRR value). The longer the remaining loan term is, the lower will be the impact of the markup on the calculated yield for the buyer. I mostly buy 40 Euro loan parts, sometimes multiple in the same loan. I selected this amount because larger parts might not appeal to as many buyers, as some investors only invest small amounts.

Why I select different values for the reserve price and the buy now price

Since the XIRR that is displayed to the buyer depends solely on the buynow markup, it would seem logical to set same markup prices for the reserve price and the buy now price, doesn’t it. If in the example above I would set the price to 8.4% for both than I would get 8.4% markup if the sale takes place. With 8% and 8.4% values, I most likely get only 8% (at these markups there are very rarely multiple bidders competing). So why would I forego 0.4% gain? The reason is simple. With buynow the sale takes place instantly. But if I get the buyer to make a bid, the transaction takes place at the end of the listing duration, and all interest accrued during this duration is mine. Note that the buyer can NOT back out. He is commited and the sale will take place if he made a bid. In the above case the 20 days on a 39 Euro loan part at 32% mean I earn an extra 0,68 Euro (39€*32%/365 days*20 days) interest. So in effect if someone bid 8% on this loan my gain is 8%+1.74% accrued interest = 9.74% gain (which is much better than the 8.4% buy now). Of course I have to deduct the 1% seller fee.

BTW, I wondered how Finbee manages the sales with the accrued interest. When the buyer makes the bid, as said he cannot back out. But it is not clear if he will win (another buyer could overbid him) or how much interest will accrue for I as the seller have the right to accept the bid anytime early (which would only make sense if my cash is zero and I urgently want to bid on a new loan with a much better interest rate). But Finbee can’t wait until the time of sale because at that time, there could possibly be not sufficient cash in the buyer’s account. I couldn’t figure it out, therefore I asked Finbee. The answer is Finbee reserves the maximum possible price (principal+premium+maximum possible accrued interest) at time of the bid in the buyer account. Once the sale takes place, if the actual accrued interest is lower than the reserved maximum accrued interest, part of the amount is freed up. Continue reading →

This is a guest post by Pawee Jenweeranon, a graduate school student of the program for leading graduate schools – cross border legal institution design, Nagoya University, Japan. Pawee is a former legal officer of the Supreme Court of Thailand. His research interests include internet finance and patent law in the IT industry.

1. Introduction : The Peer-to-peer Lending Industry in Thailand

Peer-to-peer lending which also known as social lending or crowd lending has drastically increased in the recent years in many countries over the world. The volume of peer-to-peer lending activities also has been grown rapidly, for instance, the volume of peer-to-peer lending activities in U.K. has doubled every year in the last four years.

Peer-to-peer lending might be used in many ways if it is properly regulated by the responsible authorities, this is one of the reasons which lead to the issuance of the consultation paper to regulate peer-to-peer lending industry by the Bank of Thailand.

For instance, due to the current situation, poor people and SMEs in Thailand normally face difficulties in accessing finance from banks or traditional financial institutions[i]. This affects the increasing number of informal loans outside the financial institution system which are normally illegal, specifically; the problem of informal loans currently stood at more than 5 trillion baht and covered around 8 million households in Thailand[ii]. Continue reading →

Lending Works announced that they received full authorisation by the FCA. It is the first P2PFA member to receive that status. Lending Works plans to launch their IF ISA offer in January 2017. Some smaller new entrants already had full authorisation, while the main players still operate on interim permission awaiting approval.

Lending Works writes:

We’re fully authorised by the FCA

We are thrilled to announce that we’ve today received official confirmation from the Financial Conduct Authority (FCA) of our full authorisation as a financial services provider. This is a momentous occasion for Lending Works, and also means we are the first of the peer-to-peer lending platforms operating under interim permission to receive this approval.

It marks the end of a thorough, 12-month review in which our processes, systems, policies, financials and levels of compliance and risk management have undergone intense scrutiny from the UK’s primary financial services regulator, and this green light from the FCA represents the ultimate stamp of approval. We hope that this news will further underscore your confidence in us, and all that we stand for.

Our ISA is coming soon

With this FCA approval in hand, it now paves the way for us to apply to become an ISA Manager with HM Revenue & Customs. Once this formality is complete, we’ll be eligible to deliver the Lending Works Individual Savings Account (ISA), a product we plan to launch in January. We are waiting until January to launch our ISA for a number of reasons, namely: the expected waiting period for obtaining ISA Manager approval, the fact that we have other major releases planned for the next couple of months, avoiding launching before or during the Christmas break, and to align the launch with the January-to-April ‘ISA season’.

New branding, website and user dashboard

In a few weeks’ time, we will launch new branding that we hope is befitting of our position as an innovative financial services technology firm. In addition, we will launch an easy to navigate, simple-yet-informative new website and intuitive new user dashboard. We will introduce you to the new brand, website, logo and lender dashboard closer to the time of launch, but we are confident it will further enhance your customer experience.

Partnerships

Finally, we have also got several new major partnerships going live soon too. These partnerships will bring more and more high-quality borrowers to our platform, which in turn will benefit you, our lenders.

But for now, we hope you will share in our delight at having made this significant step up with the FCA – a launchpad we believe will drive us towards even bigger and better things. …

I attended Lendit Europe in London the last days, an industry event of the p2p lending (or marketplace lending) industry. This was my third Lendit and it was not only bigger (904 attendees from about 180 companies) but again better than the previous year.

Samir Desai, CEO of Funding Circle in his opening keynote sees it as the golden age of the industry. And that certainly is the sentiment that much of the British part of the market would agree with. However there is headwind to be countered. The P2PFA, the association of the UK marketplaces that co-hosts the event, comissioned a report on the economics of peer to peer lending. Christine Farnish, the Chair of the P2PFA said that they did this to rebuke assertions by facts and counter comments by the tradional industry about risks.

The new Oxera report is available for free download here. Reinder van Dijk presented the findings of the report which focuses on the eight members of the P2PFA. He showed based on data, that in general the platforms did a good job on assessing risk, as the actual defaults for the years 2013 and 2014 were mostly in line or lower to the predictions the marketplaces made beforehand.

Lord Turner, former head of the UK Financial Services Authority created a media stir earlier this year with a very critical remark on p2p lending. In his keynote speech Turner did a turnaround saying he had not fully understood the p2p lending model in detail at that time and that he thought the interview was over when he made the comment. His final message to the marketplaces is keep it simple and transparent.

Impression from Lendit 2016 (own photo)

One major topic for the UK players is when FCA approval and the launch of the IF ISAs will occur. There is a feeling – but no certainty – that it’s getting closer. Farnish says she expects IF ISAs to be available by spring 2017. I also asked several people whether they expect it to be a big bang event, meaning that all the big players get approval at the same time to launch their ISA offer. Again there is no certainty but most respondents said they feel it would be only fair to grant the approval simultaneously because otherwise the first starter would have quite an advantage.

By the way most of the sessions, panels and demos are available here as videos and can be watched free. I recommend Cormac Leech’s keynote as a data rich, not easy to digest, but highly informative appetizer. Then for a second course with some added spice injected by Kadhim Shubber, FT, watch James Meekings of Funding Circle, Giles Andrews of Zopa, Peter Behrens of Ratesetter, Christian Faes of Lendinvest and Anil Stocker of Marketinvoice here. And for a maximum of contradicting opinions during one panel you might finish here, where Cormac Leech suggests that p2p lending marketplaces should monetize by ‘bombarding’ users with cross selling offers, not only for fintech related offers but for example also selling holidays. He think the bombarded users would be receptive if only the marketplace at the same time gives them a better rate. (I might be compressing his argumentation, please watch it in full). This to me is a stretch. I think that p2p lending marketplaces should deliver what the investors expect from them: great returns. Surely there is some opportunity for cross-selling with related financial products. On the other hand I do believe that the challenger bank (Monzo) present in this panel has some merit with it’s plan to analyse data to make fitting offers based on the budget and the spending pattern of the customer. Will that appeal to everybody? Certainly not. But the customers that will sign up with them are looking for a change from their previous banking experience so they might be open to that.

Another argument was on ‘pure’ marketplace lending model versus hybrid versus balance sheet based lending. While there are different opinions and preferences voiced, several speakers thought that there will be players of each type that are succeeding.

I actually missed many of the afternoon sessions of the first day, because one main benefit of Lendit for me is the networking opportunity. I talked to many marketplaces I knew, to keep up with their developments and plans, and made contact with new marketplaces. My view is a bit biased on topics of interest of retail investors from the continent so I am overweighting platforms news that are revelant to these in the following paragraph.

I checked with Saving Stream and they confirmed that they will lower interest rates with the intention to win more borrowers. The one size fits it all rate will be gone which takes away some of the straightforwardness/ease of use. I wasn’t told how much lower rates will go and on my question whether rates will vary depending on the loan risk, the answer was that this is yet undecided. Ed of Moneything said progress to growing loan volumes even further is good. Investly will disclose a new UI for investors soon. Aurora Exchange from Finland says it will not only launch there but will be able to serve all of Europe (not only from the investor side but also on the borrower side).

I had so many conversations, that I missed most of the Pitchit, which I had really looked forward to see. But I was in time to see the pitch by Lendingwell which was very good and as it turned out the next day that was the pitch that won.

I had the pleasure to moderate a panel on up and coming European platforms, this year featuring Creditshelf, Giromatch, Finbee and Viventor. I am looking forward to next year and am curious which great event location Peter Renton and his team will scout next time.

The following chart lists the loan originations of p2p lending marketplaces in September. This month I added Crowdestate. Funding Circle, Ratesetter and Zopa had a record month. The total volume for the reported marketplaces adds up to 424 million Euro. I track the development of p2p lending volumes for many countries. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services. Milestones in total volume originated since inception:

Table: P2P Lending Volumes in September 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. The Wellesley volume is 0 for this month – this may be a reporting error. *Prosper and Lending Club no longer publish origination data for the most recent month.