Beehive has become the first peer to peer lending platform to set up offices in the Dubai International Financial Centre (DIFC) and become officially authorised and regulated by the Dubai Financial Services Authority (DFSA).

The new regulation is a first for the region and could catalyse growth of the fintech industry, says Beehive. Not only will it ensure clear governance for fintech businesses but will also provide added protection and peace of mind for peer to peer retail investors. Its introduction is particularly timely as peer to peer lending, is becoming an increasingly important route for small and medium enterprises (SMEs) to access finance.

Beehive was launched in Dubai in 2014 by serial entrepreneur, Craig Moore, aided by Rick Pudner, former Group CEO of Emirates NBD. Read an earlier interview Craig Moore gave P2P-Banking.com. Craig Moore, now said: “We’re delighted to be regulated by the DFSA. This regulation reinforces Beehive as one of the fintech leaders in the region and we feel this greatly expands the opportunity to further help SMEs and the wider economy.†Continue reading →

The table lists the loan originations of p2p lending marketplaces in February. For many companies it has been a slow month. Funding Circle continues to lead ahead of Zopa and Ratesetter. The total volume for the reported marketplaces adds up to 408 million Euro. I track the development of p2p lending volumes for many countries. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms. This month I added Klear, Viainvest and Bitbond.

Milestones reached this month are:

Funding Circle reaches 2 billion GBP in originations since launch

Fellow Finance crosses 100 million EUR since inception

Geldvoorelkaar hits 100 million EUR since inception

Table: P2P Lending Volumes in February 2017. Source: own research Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

P2P Lending marketplace Rebuilding Society just announced that it has received full FCA authorisation.

Rebuilding Society has been awarded full authorisation from the Financial Conduct Authority in recognition of our compliance with sector-specific regulations.

We are very excited to share news of this major achievement and important milestone with our community. Authorisation means that we meet the rigorous standards set by the FCA and that we can soon start to offer the Innovative Finance ISA.

Although we have been operating under FCA rules on Interim Permission since April 2014, being granted full authorisation helps us to continue building on the important relationships of trust we have with all our clients. We are proud to have achieved this milestone ahead of many other platforms, which we believe is testament to our small but dynamic team, systems, processes and controls.

It has been a long journey, consuming considerable energy and investment, since we applied for full authorisation in November 2014. We have continued to grow as a business and improve on our core processes throughout. The regulatory landscape is continuously changing, and we will make sure we stay abreast of developments that arise from our post-implementation review.

We are committed to delivering a top-quality service to all our customers, to assist investors by providing multiple investment options and to assist our borrowers in finding business finance that is more than just a financial transaction. We are now taking pre-registrations for the IF ISA and will confirm once we can on-board new accounts. Please look out for further updates; we know that many of you are keen to benefit from frequent, compounded returns.

Since my p2p lending investments are heavily concentrated on UK and Baltic services, one of my New Year’s resolution for 2017 was to diversify into other markets. Therefore in January I opened an account at French p2p lending service Lendix. Lendix is a p2p lending marketplace offering loans to SMEs in France and Spain (read earlier articles on Lendix). It is one of the larger players in continental Europe. Signing up was straightforward. While the minimum bid on loans is just 20 EUR, the minimum amount for deposits and withdrawals is 100 EUR. Investors can deposit either via bank transfer or via credit card (limited amount). Depositing via credit card is a nice feature which is rarely offered by p2p lending services. I like it because I can react within a minute to new loan announcement emails. This is necessary too, as many new loans are fully funded within an hour – and there is no autoinvest. Nearly all actions require two factor authorisation by a code sent to my mobile.

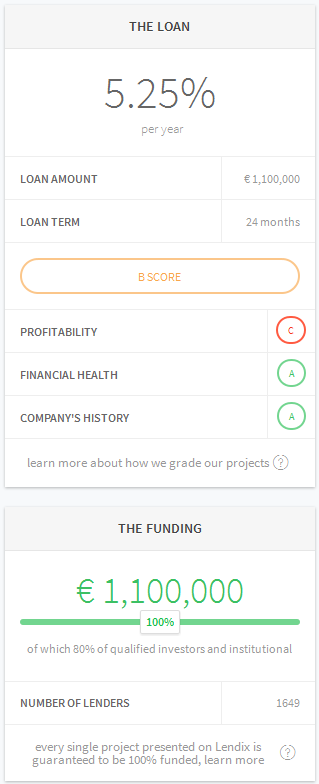

Lendix loans carry interest rates from 4 to 9.9% and are for loan terms between 3 and 84 months. There is no fee for investors and no withholding tax for foreign residents. Each loan is assigned a rating score of A, B or C by Lendix. There is also a detailed loan description for each loan. While most of the site is available in English language, loan descriptions and contracts are in French language only.

So far Lendix has done a very good job in vetting borrower applications. The default rate to date is low – only 0.11%. However the marketplace is young and growing and I expect the default rate to rise with time. Also it remains to be seen, if the perfomance of the Spanish loan will be comparable to the French loans.

As there is no secondary market, investors are bound hold the loan to maturity.

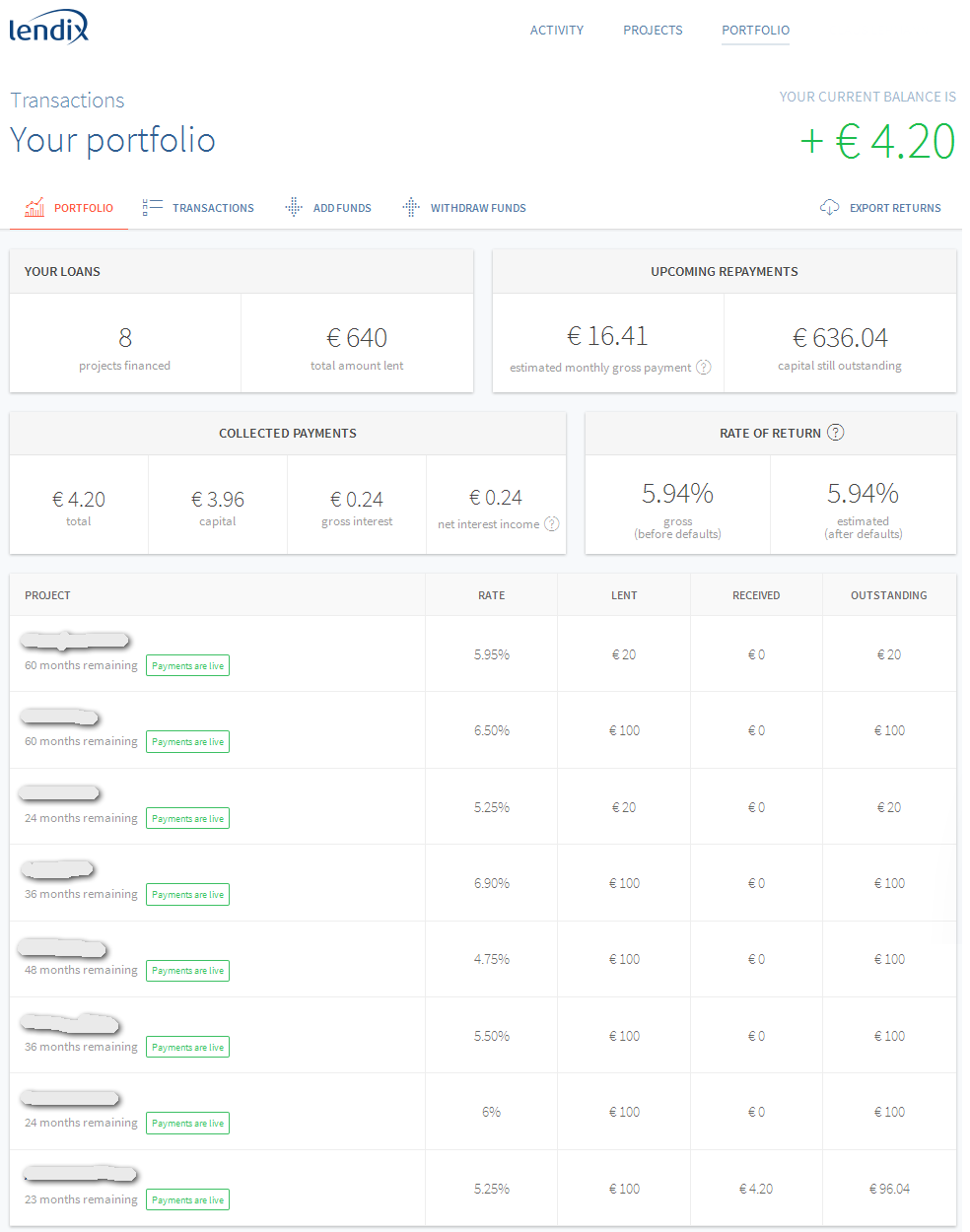

Review of my Lendix portfolio

I only just started in January. I concentrated on A and B grade loans, putting 100 EUR in most of them and 20 EUR in those that seemed not as convincing to me (e.g. a loan to a hotel that, when I looked it up on a hotel booking comparision site, had less satisfied customer reviews than the four other competing hotels in the same village). I skipped the new spanish loans.

Right now I have invested 640 EUR in 8 Lendix loans. I would have invested more, but I found the dealflow to be rather sparse in January and February. My average interest rate is 5.9%. This month I received my first repayment rate. Experiences of more seasoned investors report that repayments are usually on-time.

New investors get 20 EUR cashback bonus from Lendix when signing up via this link, once they have invested at least 500 EUR.

Screenshot of my Lendix loan portfolio – click for larger view

P2P lending marketplace Finbee has so far offered consumer loans only. Now Finbee is extending the product range to SME loans. Finbee sources the applying companies through a separate website and will focus on small loans up to 15K EUR and a term of 12 months. For most business loans rates will be fixed without an auction (which Finbee uses to set interest rates for consumer loans). Different to consumer loans, investments into business loans will not be covered by the Finbee compensation fund (CSF), if the loan defaults. Each loan application will be individually assessed, by assigning risk grade from A+ to D, where A+ is a low risk loan, D – high risk loan, based on reputation of the management (20% of risk grade), financial sustainability (60% of risk grade), market situation (20% of risk grade).

Audrius Griskevicius, head of SME lending, told P2P-Banking: ‘SMEs in Lithuania have very limited access to financing. As result of this, the government issued a law, allowing p2p lenders to issue loans for small business. Finbee took an active role in development of necessary regulation and we are very proud to be the first one to receive a license of p2p lending to SMEs.’

The first business loan listing is online. Magava wants to borrow 10K EUR working capital for 12 months at 15% interest rate. Investors have to complete a self assessment survey before they can invest into business loans.

SME lending platform Bitbond today announced the closing of an equity funding round of 1.1 million EUR. This round brings Bitbond’s raised equity capital to a total of 2.2 million EUR.

Led by mobilike founder Şekip Can Gökalp, a number of business angels contributed to the round. Among them were Fyber founders Janis Zech and Andreas Bodczek as well as Kreditech co-founder & CEO Alexander Graubner-Müller.

Bitbond will use the additional funds for further product development and to grow its user base in markets which are underserved by traditional lenders. Over 1,600 loans worth 1.2 million USD were originated on Bitbond since its launch. 76,000 users from 120 countries registered with the service to date.

Founder & CEO of Bitbond Radoslav Albrecht said: “The additional resources will help us to continue realizing our mission which is to make lending and borrowing globally accessible. We are happy to have such experienced investors supporting us on this exciting journey.†Albrecht contributed a guest article on bitcoin p2p lending in the past on P2P-Banking.

In October 2016 Bitbond received their own regulatory licence by German financial services supervisor BaFin. This makes the service one of the first and only regulated blockchain based financial services providers.

The startup from Berlin connects investors who look for above average fixed-income investment opportunities with small business owners who need a loan. To make global cross-border lending possible, the platform uses the bitcoin blockchain for payment processing. Continue reading →