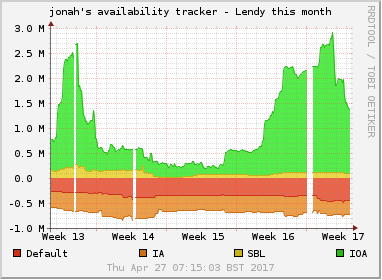

When I started in late 2014 the UK p2p lending marketplace Lendy was still called Saving Stream, but it rebranded this year. Lendy is a platform offering bridge loans secured by property. I last reviewed my portfolio performance here on the blog in January 2016. Since then the following major changes have taken place at Lendy:

Different interest rates Initially all loans had carried 12% interest. Now Lendy assigns different interest rates to each loan. Interest range for investors on new loans now are in the range between 7 and 12%.

Lendy sold the security of the second defaulted loan (Garden Center). While all lenders got principal and interest paid on this loan, the sale price of the security was below the loan amount. Lendy covered the shortfall from own funds (provision fund).

Since March 2017 investor can not buy loans on the secondary market and deposit funds afterwards (this still is possible on the primary market). This has reduced liquidity of the secondary market somewhat, but in general it is still pretty liquid for those loans that have a middle to long remaining term.

Since April 2017 there is a new default policy in effect. For loans more than 90 days overdue interest continues to accrue but will not be paid until Lendy has received payment by the borrower. All loans more than 180 days overdue are now automatically classified as default loans. The number of defaulted loans has risen to 14 at the time of this writing.

Especially the last point has triggered debates on the chances for recovery and there are concerns voiced among investors about to optimistic valuations. The secondary market swings from time to time between mosty empty (except for loans in default) and plenty.

My portfolio

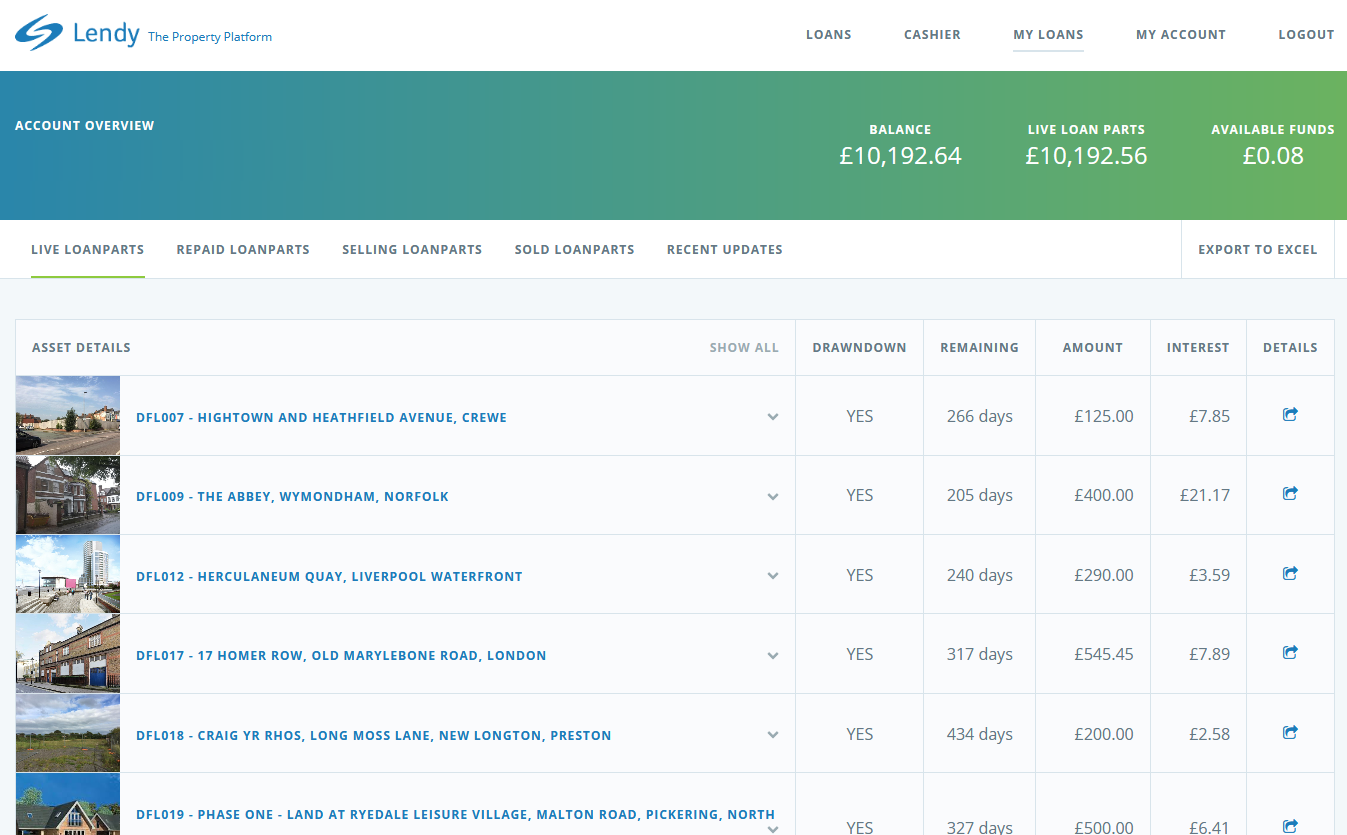

I have continued to ramp up my portfolio reinvesting returns and making new deposits via Transferwise and Currencyfair. This was before the Brexit decision. As for now I am simply reinvesting. My portfolio amount is 10K GBP spread out over 14 different loans. The vast majority is in 12% interest rate loans. I have made three exceptions in the past, but usually only with low amounts and when rebalancing the portfolio, I try to sell these lower interest loans first. So far I have not had any loans in overdue or default state – but there are many of those on the platform (see above). My loans have long remaining terms with the shortest being 147 days at the moment.

My yield (self calculated with XIRR) so far is 12.1% in GBP. Unfortunately I deposited most funds during the time when the pound was at a high, therefore calculated in Euro currency the yield is only 4.4% for me.

Lendy is still one of my preferred p2p lending marketplaces, due to interest rates, real estate as a security and liquidity. I do see the risks in the valuations, but I figure that at least the security will cover part of the loan amount and will with a high probability prevent total loss in a defaulted loan. I might get more picky in selecting loans, but so far Lendy for me is actually a platform that requires less management and monitoring than several other marketplaces I use.

Screenshot of top of my loan portfolio list at Lendy – click for larger view

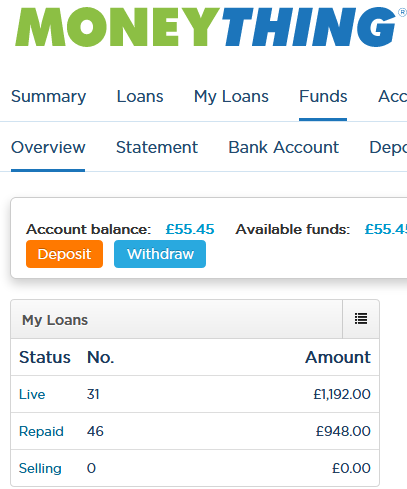

Last year I started investing on British p2p lending marketplace Moneything. Read my past article about opening a Moneything account. Moneything mostly offers property backed loans, with a few different asset-backed deals in between. I used Transferwise and Currencyfair to deposit money from my Euro account. Recently I also used the Revolut App to transfer money from another UK p2p lending marketplace to Moneything.

Looking back over the past year my experience with investing on Moneything has been very good. I am invested in 31 loans right now, mostly at 12% interest rate with small amounts also at 10.5%, 11% and 13% invested. I have had no defaults and there are no fees for investors. The website functions well and support is reported to be very responsive (I actually did not need it yet). The secondary market is extremly liquid, loan parts often sell within second. The only two minor downsides of the Moneything platforms for me are that investor demand by far outstrip loan offers. And there is no autoinvest, so usually it is necessary to login shortly after 4pm UK to invest into new loans. My yield (self calculated with XIRR) so far is 12.0% in GBP. However due to currency fluctuation in EUR it is only 7.2% at the moment.

So if all is great, why did I not invest more? Well, I planned to, but shortly after I started, Brexit vote took me by surprise and I abandonned my plans to ramp up my investment amount, due to the higher currency volatility uncertainty. Instead I am now mainly reinvesting funds and in addition add funds already in GBP, which I move over from other UK platforms via Revolut.

Earlier this month Moneything gained full FCA approval. This is the prerequisite for launching an IFISA product, which allows tax-free investing for UK investors (compare IFISA providers in our database). Surprisingly Moneything just said, they are in no hurry to launch an IFISA offer but rather wants to built loan originations first. This makes sense because the increased deposit influx by an IFISA offer would imbalance demand and supply even further.

P2P-Banking launches a new IFISA database, that enables investors an easy comparison of offers by IFISA providers. UK taxpayers can invest up to 20,000 GBP per year tax-free in ISAs. This amount is per tax year, so a person could invest 20,000 GBP this tax year and invest 20,000 GBP in a different ISA next year. The Innovative Finance ISA, short IFISA, was introduced in 2016 with most offers becoming approved by HRMC only in the 2017/2018 tax year.

The new database of IFISA offers allows speedy selection and sorting to review IFISA products by different providers and then links to the provider’s website for in detail information. Investors can filter by interest rate, term, loan type, minimum investment amount, possibility of transfers in and out, flexible IFISA, bonus & cashback promotions and several other criteria. The comparison focusses on IFISAs by p2p lending marketplaces but also lists IFISAs investing in crowd bonds and other investment types. Currently more than 15 IFISA providers are listed and P2P-Banking will list new offers as they are approved by HRMC and launched in order to help investors get the best IFISA rates that match their investment strategy and risk appetite.

Several companies have reported huge demand in their new IFISA offers. Lending Works reported a huge spike in investor deposits after launch and last week the consumer loans marketplace said, it has recorded £8.8m of subscriptions into its IFISA in the first 3 months with 815 investors lending. CapitalRise has stated earlier this month that the IFISA product raised 900,000 GBP in the first 4 weeks. Crowd2Fund, said that 95 per cent of its investments are now made through the tax free wrapper. CEO Chris Hancock said the platform is experiencing 50 per cent month-on-month growth and is expecting to originate 2 million GBP in loans in April. ‘Last week, 58 IFISAs were opened from 115 investor registrations,’ he said. ‘I think the IFISA market has grown three-fold in terms of investor demand over the past year.’

More p2p lending marketplaces have gained FCA approval recently and are preparing to go live with IFISA offers in the next weeks. Readers of P2P-Banking can subscribe to the free notification service and receive an email whenever the database is updated and a new provider is added.

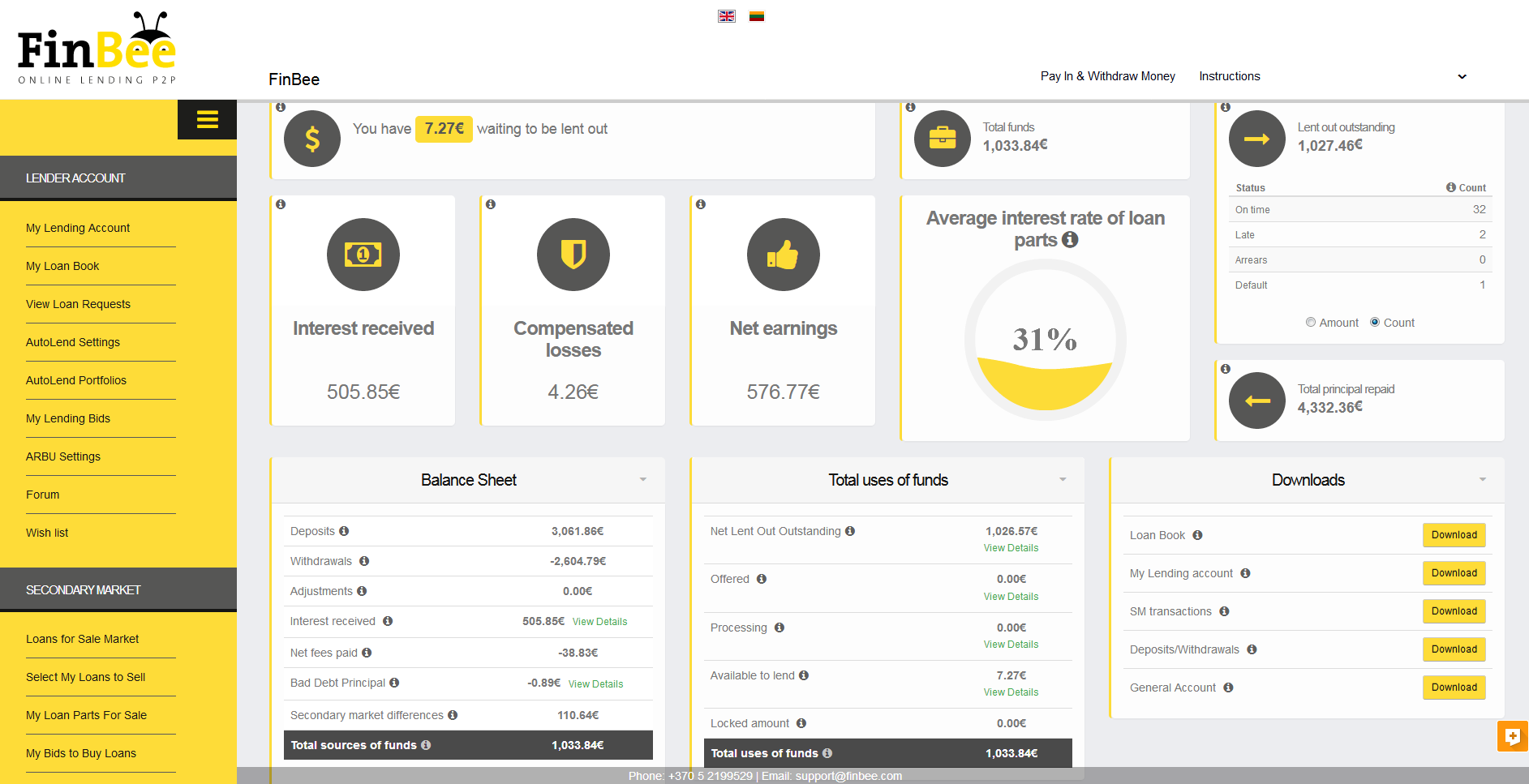

A year has passed since I last wrote about the portfolio I built on Finbee. For a detailed description of this Lithuanian p2p lending marketplace see my earlier review. As described there, I invested mostly in the highest risk grade loans (‘D’ loans). Currently I have invested 1,027 Euro in 35 loans. 32 are current (965 Euro), 2 are late (23 Euro) and one is in default (38 Euro), but rates for this loan are paid to me by Finbee’s compensation fund. The average interest rate of my loan parts is 31%. Interim I had grown my portfolio to up to 3,000 Euro invested, but interest rates have decreased due to high investor demand that was not met by comparable growth on the borrower side, so I have withdrawn 2,604 Euro meanwhile.

My results so far

My self calculated yield (XIRR) is 31.5%. This is the highest I achieved on any p2p lending marketplace over a longer duration of time. This includes the 110 Euro capital gain caused by sales of loans on the secondary market with premiums (see my article on trading on Finbee’s secondary market). Calculating the result again, this time with assuming a full write-off of the defaulted loan gives a yield of 29.4%.

Screenshot of my Finbee dashboard – click to enlarge

There are 19,930 Euro (as of March 13th) in the Finbee Compensation Fund. Current estimate is that the fund is paying about 9,000 Euro per month on defaulted loans and has decreased about 2,000 Euro from February to March. To grow the amount in the Compensation Fund Finbee will need to increase the volume of new loan originations. I looked into the list of open loan requests this morning and there are currently only 3 consumer loans and 2 business loans open for funding.

This article is a must read for non-residents, investing on British p2p lending marketplaces from abroad. You will learn two advantages that will make the process easier for you and save you money by using the free Revolut App.

What is Revolut?

Revolut is a free app for money management. To register you need:

An Android smartphone or an iPhone with front and back camera

to be a resident in the European Union, Norway or Iceland and your ID document (e.g. passport)

the ability to receive SMS messages

Just download the app in the Google Play store or the App Store on iOS.

After that, I suggest to first follow the steps described that are needed to verify your identity, as this is a prerequisite for some of the features described further down. This took me about 10 minutes.

Usecase 1: Free transfer of money from one UK p2p lending marketplace to another

I have invested on several UK p2p lending marketplaces, but there was no free way to shift money from one UK marketplace to another as I do not have a UK bank account, since I am not a UK resident. Up to April last year I could use a free Monese account, but Monese started charging 5 GBP per month, so that was no longer an option.

Every Revolut user can get an own UK bank account number for free. Important update: Not true any more for new accounts – see comments. It is important to note though that technically Revolut is regulated as an electronic money issuer and is not a bank. This means that money in your account is not protected by the UK deposit protection scheme (FSCS)! However that is fine for me as I just use the account to pass the money through on the way from one platform to another.

The important fact is that with the own account number it is possible to use that for withdrawals from UK marketplaces as no reference is needed for the transfer. I have done this a couple of times now and it takes only a few hours for the money to arrive and get credited. Likewise it only takes a few hours after I transfer it to another platform to be credited there. All without incurring any costs for me.

Entering the recipients bank details on a smartphone is a bit cumbersome, but it needs to be done only once, as the details are stored and can be reused for future transfers.

Note to UK investors: You cannot use the Revolut app likewise for transfering funds from on p2p lending platform in the Eurozone to another p2p lending platform in the Eurozone. At least not at the moment. The reason for this is that users don’t get an own IBAN account number. Warning: Revolut will block Euro transfers that come from a third party and return them and deduct a fee and return the funds to the sender.

Another potential benefit might be, that foreign investors could gain access to those UK platforms that don’t require residency but do require a UK bank account. But I haven’t tried if that works with a Revolut account. If anybody checks this out, please post your experiences in the comments.

Usecase 2: Best exchange rate for changing Euro into Pounds

Conventional bank transfers are not a good option for moving money from an Eurozone bank account to a UK p2p lending platform due to fees and bad exchange rates applied.

Instead I used Transferwise and Currencyfair so far and have been happy with these services. However there might be issues with platforms not supporting withdrawals via these.

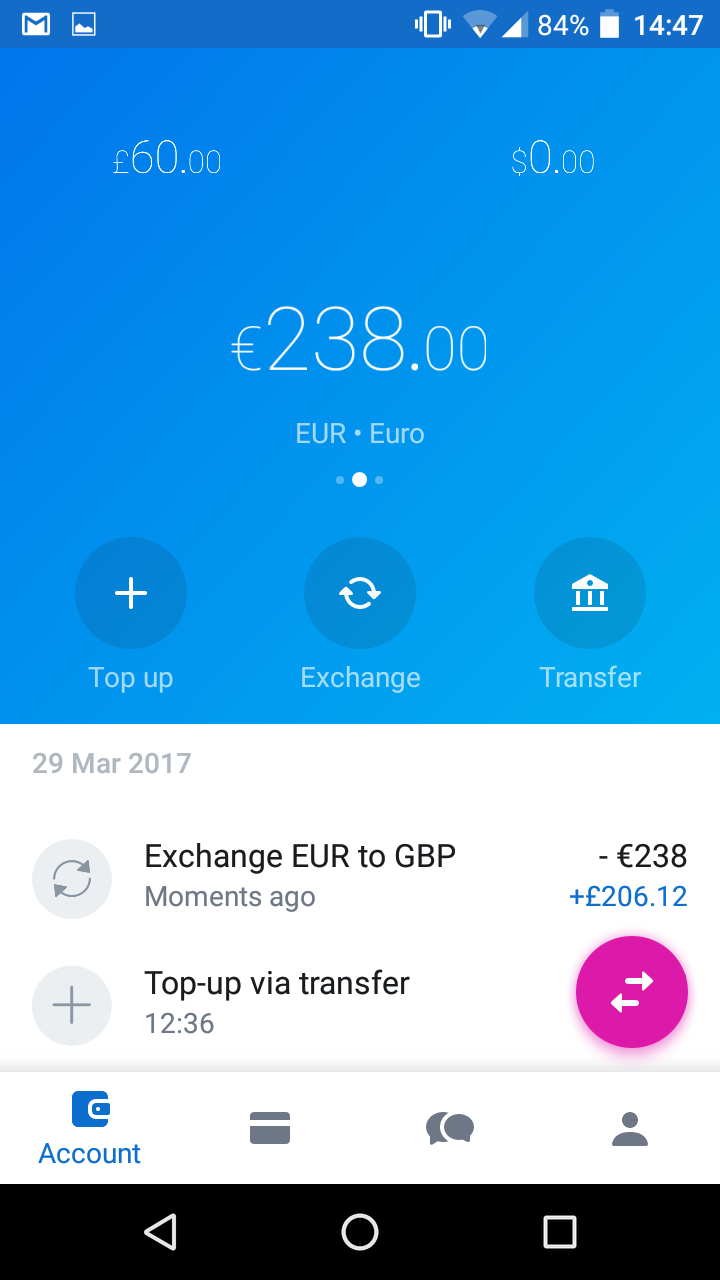

And when I did a comparison of exchange rates at the time of writing this article, I found that actually Revolut offers a much better exchange rate. This is what I got when I compared:

Revolut: 238 Euro gets 206.12 GBP

Transferwise: 238 Euro gets 204.92 GBP

Currencyfair: 238 Euro gets 202.91 GBP

Quite a difference, though it will be smaller for larger amounts and you can actually influence the exchange rate on Currencyfair by setting a desired rate.

To exchange Euro into pounds I simply transfered money from a bank account in my name via a SEPA transfer to the Euro account of Revolut, stating my personal reference number the Revolut app showed me under ‘Top-up‘, ‘EUR‘ ‘Bank transfer‘. After two days Revolut alerted my via push notification (they don’t send emails) that the money arrived. Via the exchange menue point I can then see the fluctating live exchange rates and execute the exchange any time I want.

Important tip: Never exchange money on Revolut on a weekend, as Revolut will charge a 1% fee then.

Also note that there is a limit of 5,000 GBP /Â 6,000 EUR / 6,000 USD (or equivalent) per calendar month for the free foreign currency exchange. That is sufficient for my needs. Above that Revolut charges a 0.5% fee. If you invest really large amounts it might by worthwhile to consider upgrading to a premium account for a monthy fee as premium accounts do not carry fees even for larger exchanges.

To sum up: Revolut makes investing on multiple UK p2p lending platforms much easier for European investors and can save a lot of money during currency exchange for investors from the Eurozone. I have used the account for only a few weeks so far and I really like it and I do hope the basic account will stay free.

Fans will actually have the opportunity to invest into equity of the Revolut company and own shares of Revolut soon. This will be conducted through the equity crowdfunding platform Seedrs. The concrete date has not been announced yet, but if you are interested you should register at Seedrs now to complete the registration and verification process ahead, as I expect the Revolut campaign will be oversubscribed and filled within hours, if not minutes, once it is launched. In fact, when Revolut raised 1 million GBP last year on Crowdcube, the offer was massively oversubscribed. To see how pitches work at Seedrs have a look at the current pitch by p2p lending company Landbay or read my earlier articles about Seedrs. Notice:This article is not an investment advice. Investing in startups bears significant risks, including total loss of investment.

Revolut says it currently has 550,000 users. I expect that to rise fast with the advantages the Revolut account offers. Have you used Revolut in the context of your p2p lending investments? You are welcome to share your Revolut experiences in the comments.

Oh and I forgot to mention: There is even another interesting tie-in of Revolut with peer to peer lending. UK users can get a loan through Revolut which is actually handled by Lending Works funded though fellow p2p lenders. During AltfiEurope Summit a figure of 300 referred loan applications per day was given and that was only 2 weeks after launch.

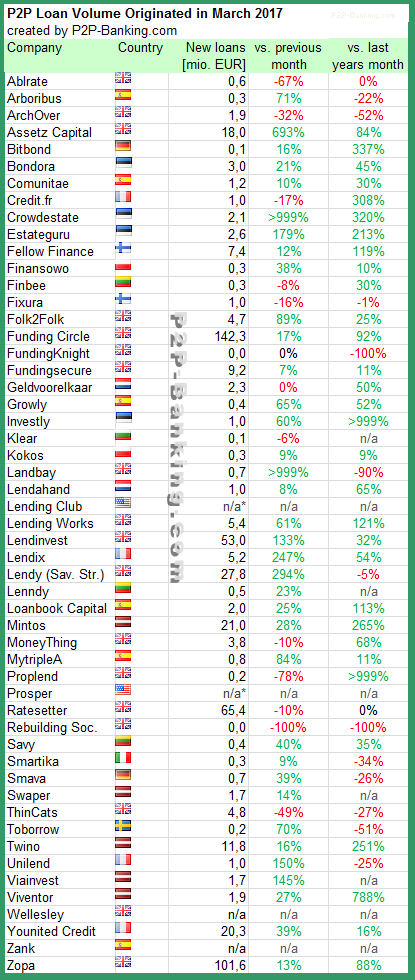

The table lists the loan originations of p2p lending marketplaces in March. Volumes picked up considerably compared to February. Funding Circle continues to lead ahead of Zopa and Ratesetter. The total volume for the reported marketplaces adds up to 532 million Euro. I track the development of p2p lending volumes for many countries. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms. This month I added Lenndy and Credit.fr.

Milestones reached this month are:

Mintos crossed 150 million EUR in originations since launch

Table: P2P Lending Volumes in March 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.