Linked Finance announced yesterday that it secured full approval from UK regulator:

I’m delighted to announce that we recently gained full authorisation from the Financial Conduct Authority in the UK. This approval is the culmination of a rigorous 2-year application process and a lot of hard work.

In the absence of any regulatory framework in Ireland, we originally began this process as a way to demonstrate our commitment to operating Linked Finance in line with best practice from the much more developed UK market.

This UK approval also opens several exciting avenues to us in terms of our plans for future expansion. It gives us the opportunity to attract lenders form the UK to support Irish SMEs. It would also allow us to start supporting SMEs north of the border, as well as paving the way for a full UK roll-out.

The P2P industry in the UK is the largest in the world on a per capita basis and platforms there are originating more than €1 billion in lending each quarter. It would be a logical next step in our evolution.

That said, our primary focus remains on Ireland and helping to grow the sector here as market leaders.

This authorisation in the UK won’t have any major impact on how you use Linked Finance but you may see some slight changes and modifications on the site, as we look to implement some of the various requirements, such as warnings and disclaimers, that would be required when operating in the UK.

The fact that we have gained full authorisation from the FCA should simply serve to underline that Linked Finance has developed the type of management processes and controls that are in line with industry best practice.

The timing couldn’t be better too.

This announcement comes as the Irish government have launched a public consultation in relation to regulating the sector here.

It’s a move that we wholeheartedly welcome. We believe that all platforms who want to operate in Ireland should be required to operate to the same high standards as Linked Finance.

Obviously, this approval from the FCA demonstrates that we are well ahead of the curve in the Irish market and we are encouraged that the Department of Finance is now considering a similar set of rules here.

We recognise that the development of P2P lending in the UK owes a lot to the introduction of government initiatives that promote the industry, including tax-free Innovative Finance ISAs and direct government lending to SMEs, via the British Business Bank, on platforms such as Funding Circle and RateSetter.

We would love to see the same type of support here and we will be using the current public consultation as an opportunity to promote similar initiatives in Ireland.

For our Irish lenders, this approval from the FCA in the UK should serve as further evidence of our commitment to developing a strong and stable platform that will continue to deliver healthy returns while providing much need credit to great local businesses.

DoFinance is a P2P platform for private individuals to invest in consumer loans.

We believe in finance for human –  DoFinance aims to become the most user-friendly, secure and accessible P2P lending marketplace possible, so that anyone can participate in seemingly complex processes and become his or her own financial director.

What are the three main advantages for investors?

Potential investment risks for investors are well-balanced and brought to minimum: all loans are secured with a BuyBack guarantee. If the borrower doesn’t pay back the loan, you don’t have to wait for an extra 30 days (after the investment due date) to get your funds back – your money is available right away;

You have access to your money at any time – if you decide to withdraw invested money before the due date, you can receive your money starting from 14 to 28 days after your request with (or without) accumulated interest, depending on your chosen investment plan and preferred withdrawal term;

Your money never sits still; it is always earning. Auto Invest program on DoFinance reinvests funds the moment the borrower returns the loan and the investor’s money becomes available.

What ROI can investors expect?

Depending on the chosen investment plan, investors earn up to 12% annual return.

DoFinance was founded by the Alfa Finance Group. Can you please describe what Alfa Finance Group does and why it decided to set up the DoFinance marketplace?

The Alfa Finance Group is an online lending and investment management company operating with consumer loans in Poland, Georgia and Indonesia. We are proud that in less than two years – since its launch in 2015 –  the Alfa Finance Group has attracted more than 150,000 registered clients and over €16 million in loans issued as financing loans.

Launching [the] P2P platform is just one of the steps toward expanding the list of available financial services of Alfa Finance Group. Our goal is to continue developing and offer more financial services in the investment management sector.

According to the press release Alfa Finance Group has invested 2 million Euro in launching DoFinance. Can you please describe what the money was used for?

The money was invested in technologies to create the platform and in building our loan portfolio.

The best warranty for the safety of investors’ funds, we believe, is effective risk management when it comes to the borrowers thereof big part of the money was invested in developing risk assessment tools that allow us to evaluate borrower’s behavior to detect their willingness to repay as precisely as possible. Our risk assessment tools as well as expertise in risk management permits us to evaluate the behavior of each potential borrower, hence minimizing the risk of failure to repay the loan and making the investment process as safe as possible.

Is the technical platform self-developed?

Yes. The technical platform is built on two pillars – creating a more secure and user-friendly P2P lending platform. During the development stage, we focused on smart risk assessment and platform that is handy, accessible and easy to use. We consider customer feedback carefully and, although a lot has been done already, we are still at the very beginning of our journey – the next challenge is to work on the planned improvements.

What was the greatest challenge so far in the course of launching DoFinance?

Obviously, the fierce competition in the industry challenges us to work faster and bring innovations to the marketplace, but it would be just fair to call it motivation and not challenge.

DoFinance is a marketplace, and it is vital for us to make sure the products we offer are entirely safe.

The greatest challenge was to develop a risk assessment tool that would minimize the risk of failure to repay the loan, be effective and secure. Risk assessment and management is our strength, and all our loans are secured with a BuyBack guarantee. If the borrower doesn’t pay back the loan, you don’t have to wait for an extra 30 days (after the investment due date) to get your funds back – your money is available right away.

Another challenge was becoming available also to Asian investors. DoFinance is the first European-based P2P lending platform to open customer center in Indonesia, bringing together European customer centered approach and Asian investors. We are happy to be the first ones to offer such individual approach to all our customers and give the chance to Asian investors to invest in Europe.

Which marketing channels do you use to attract investors?

Technology innovations are at the heart of our products hence we mainly use the opportunities digital marketing channels offer. It is a great channel to also reach important players in the industry – opinion leaders, investors, experts etc.

Finance for human stands behind everything we do, which means we look for creative ways to reach our audiences – not only fintech professionals, but also investors without a professional background in financial and investment management. Anybody who is at least 18 years old and holds a bank account can register at DoFinance and, by investing as little as 10 EUR per loan, become his own financial director.

Is DoFinance open to international investors?

Yes, DoFinance is available to private individuals holding a bank account in EU, EEA countries as well as Asian countries which are not included in the lists of high-risk and non-cooperative jurisdictions and international sanctions (Indonesia, Singapore, Vietnam etc.).

What is your opinion on the planned upcoming regulation in Latvia for p2p lending?

It is important that the Ministry of Finance includes industry representatives, when developing regulations on p2p lending platforms. Regulations developed without a throughout understanding of the industry can harm both investors and businesses.

Fintech industry has a potential to become Latvia’s success story which would contribute to both image and prosperity of the country, thus there must be healthy balance between industry regulation and its self-regulation. The entire financial industry and eventually the consumer will benefit from the development of FinTech as banks and FinTech companies will start cooperating when it comes down to providing financial services, customer service etc. Therefore, it is the state’s responsibility to create environment where these companies will stand and where intellectual capacity of labor will increase and taxes will be paid. At the same time, the regulation must ensure transparency and monitoring – simply because then dishonest entrepreneurs wouldn’t be able to harm investors.

Where do you see DoFinance in 3 years?

DoFinance will definitely expand geographically and continue working on developing new financial products for international markets. Our services just became available to Asian investors and now DoFinance looks even further – we don’t want to limit ourselves when it comes to geographical borders.

As we already mentioned, DoFinance is just the first step toward expanding the list of available financial services of the Alfa Finance Group. Most importantly, with every new development we make sure to keep our core principle – finance for human.

P2P-Banking.com thanks Janis Kulikovoskis and Viesturs Kulikovoskis for the interview.

Bitcoin based SME marketplace lender Bitbond has received a commitment from Obotritia Capital to fund loans worth 5 million Euro through its platform. Additionally, Obotritia invested an undisclosed amount of equity to acquire a stake in Bitbond.

With the debt commitment, SME loans from European prime borrowers will be funded instantaneously on Bitbond. This will reduce the time it takes for business owners to apply and receive a loan to 30 minutes.

The equity investment from Potsdam based Obitritia will be used by Bitbond for further product development and marketing. Bitbond plans to continue growing its user base with online sellers and small businesses who need working capital financing.

Over 1,700 loans worth 1.4 million Euro were originated through Bitbond since its launch in 2013. 90,000 users from 120 countries registered with the service to date.

Founder & CEO of Bitbond Radoslav Albrecht said: ‘The debt commitment by Obotritia brings Bitbond to the next level in our efforts to provide universal SME financing. The next step is to work with partners. Such partners could be online marketplaces who want to add value to their platforms by giving their merchants access to instant cash through Bitbond.’ Continue reading →

LandlordInvest is a UK-based peer-to-peer lending platform for residential and commercial mortgages. We launched in December last year after becoming fully FCA authorised. In January this year, we made bit of P2P history as we launched the first residential mortgage backed Innovative Finance ISA, ahead of major players such as LendInvest and Funding Circle.

What are the three main advantages for investors?

Security – we believe that loans should be asset-backed as it creates a form of security for investors if a borrower defaults. I personally would not invest in unsecured loans given the risks and the potentially very lengthy enforcement process to reclaim part of the capital, if any at all.

Returns – We offer returns of up to 12%, although we recently funded a loan with a rate of 19% to investors. The loan was arranged with a trusted bridging lending partner and is secured over a flat in Chelsea, one of London’s most prestigious areas.

Diversification – We offer investors the possibility to invest in both relatively low-risk buy-to-let mortgages and more risky bridging loans. Investors can build their portfolio according to their risk appetite and other considerations.

What are the three main advantages for borrowers?

Manual underwriting – we are more pragmatic in our underwriting than most high-street lenders and assess each loan on its merits. For us, the most important part of our assessment is that the borrower has a verifiable track-record and that the security is enforceable in the event of the default.

Speed – we recently assessed a loan, had it fully funded and completed in two days. It was for a borrower that was let down by his exiting lender for an obscure reason at the last minute and approached us.

Online application with a simple online control panel – A borrower may apply for a loan through a simple online form and keep track of the status of their application, loan schedule, loan payments in a easy to use control panel.

What ROI can investors expect?

We aim to offer returns between 5-12% per annum, depending on the product.

You recently launched an IFISA product. How has the investor uptake been so far and was it a big advantage to be in the forefront of approved providers?

The demand for our IFISA has been good. IFISA account holders, although only around 20% of the total registered investors, account for 50% of all funds on the platform. As such, IFISA account holders usually deposit more than non-IFISA account holders and also invest more.

I believe that the main advantage of being one of the first platforms able to offer the IFISA is that we have managed to establish a presence in the industry. If it was not for the IFISA, we would probably be less known than we currently are, given our relatively recent launch.

It remains to be seen what happens when the major players are able to offer the IFISA, but I believe it will be a benefit for us as it will make the IFISA a more mainstream product, benefiting everyone in the P2P industry.

Is the technical platform self-developed?

A prototype of the platform was developed overseas, but the final platform in use today was developed in-house by our tech team, led by our co-founder and CTO Joe Vallender. We continue to make all further developments in house, and are releasing new features regularly.

What was the biggest challenge in launching LandlordInvest and what have been challenges since?

The biggest challenge has been operating under a “real†P2P model, i.e. no pre-funding of loans. As we were one of the first platforms operating under this model, some investors did not fully understand how it works, as many were used to the pre-funding model operated by many players within our niche. One of the drawbacks with a “real†P2P model is that a loan does not start to accrue interest until a loan is complete. This means that there is a certain cash drag. However, one of the benefits with a “real†P2P model is that lenders lend directly to the borrower(s) and the servicing fee charged by us is usually lower than what platforms that operate a pre-funding model charge. This means that we pass on more interest to the lenders.

How is the company financed? What background does your team have?

LandlordInvest was initially entirely financed by the founding team and have recently raised financing from business angels. We’re currently in discussion with several private and intuitional investors to raise another round, which will help us to further ramp up our capacity.

Which marketing channels do you use to attract investors and borrowers?

We use a multichannel approach including, establishing good relations with the press, having an interactive presence on various forums and blogs, affiliate marketing programs and social media presence.

We still believe that the best marketing is doing what we set out to do as the best marketing channel is always word-of-mouth. If we are able to satisfy the platform investors, then there is a high chance that they might recommend us to someone else.

Is LandlordInvest open to international investors?

LandlordInvest does accept overseas residents, subject to KYC and AML checks.

However, it is a requirement that investors must have a UK bank or building society account to be able to invest on our platform.

I hear you are planning a secondary market? Will that work with premium and discounts or at par? What other features do you plan to roll out this year?

We are indeed developing a secondary market and expect to launch it in the beginning of May this year. Investors will only be able to sell loan or loan parts at par. Investors will also be able to sell parts of loans.

We are always developing the platform as we want to deliver the best experience investors can have when investing our platform.

We welcome feedback from investors and have implemented a number of features following direct conversations with investors, and will continue to do so.

Where do you see LandlordInvest in 3 years?

We have established ourselves as one of the leading platforms within our niche and delivering good risk adjusted returns to the platform investors. This has also been our aim since we founded the company and we will do our utmost to reach that aim.

Flender, which recently soft launched a p2p lending marketplace in Ireland, received full FCA authorisation last week, saying it took two years of consultation with the FCA and the legal team to achieve approval. This will be needed for the launch in UK, planned for later this year.

Limited time offer: Cashback: 10% cashback on any investment over 1,000 GBP for P2P-Banking reader. Sign up to use. (Update Aug. 2017: the cashback offer has been extended to August 31st, the minimum investment requirement is now 2,500 EUR)

Flender offers both SME and consumer loans on the marketplace. The main points for investors are:

no fees for investors

50 Euro minimum bid

open to international investors (prerequisite is a bank account in the European Union)

interest rates of the currently listed loans range from 8.1% to 10.4%

reverse auction bidding (though at the moment, loan supply outstrips lender demand, therefore I don’t expect any underbidding soon). currently no autoinvest

Flender charges origination fees for business loans from the borrower. While there are no origination fees for borrowers for consumer loans, Flender does have a margin income on those (same with business loans).

Once the UK operation launches, investments can be made cross-border. An interesting aspect is that the borrower will take the FX charges.

Flender does have big plans. On the list are an IFISA offer, several features for investors and borrowers to customize the experience and mid term a secondary market. Flender currently has a team of 7 employees.

I published an interview with the CEO of Flender in the end of 2016, when they raised 500K GBP through equity crowdfunding on Seedrs. Flender will likely be back on Seedrs to raise another round later this year.

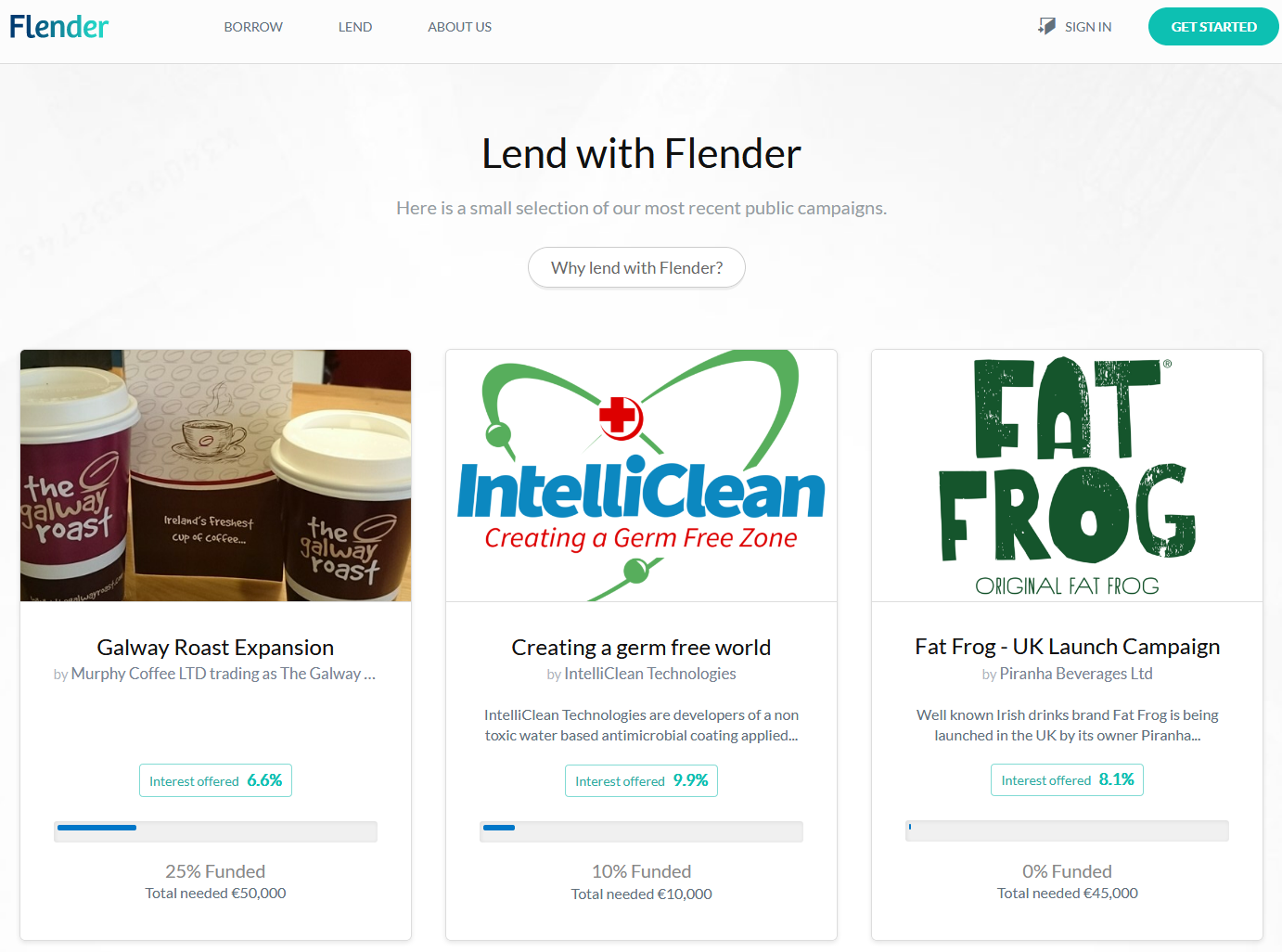

As my experiences with another Irish p2p lending marketplace are good so far (it has low default rates), I registered on Flender too. There are currently 4 business loans listed seeking a total amount of about 150K Euro.

Screenshot of Flender marketplace loan listings (excerpt)

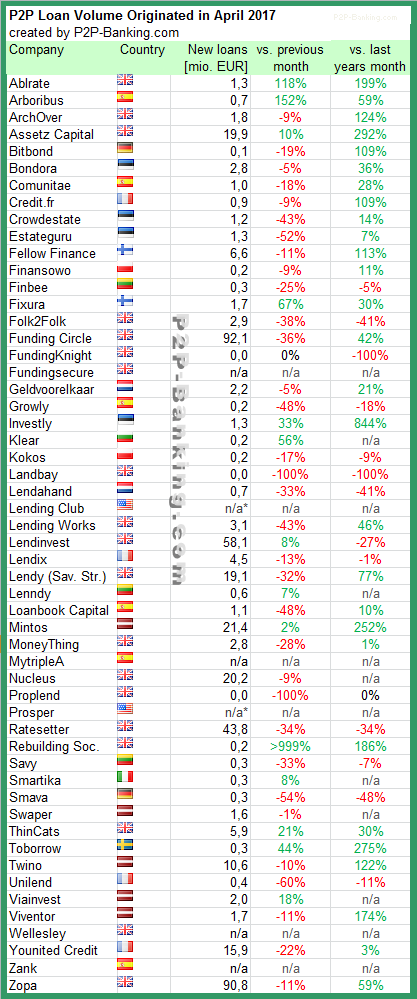

The table lists the loan originations of p2p lending platforms in April. Funding Circle leads ahead of Zopa and Lendinvest. The total volume for the reported marketplaces adds up to 445 million Euro. I track the development of p2p lending volumes for many countries. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms. This month I added Nucleus.

Milestones reached this month are:

Younited Credit crossed 500 million Euro loan volume since launch

Table: P2P Lending Volumes in April 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.