For investors, that considered using the Lendy platform, but have not yet signed up, now may be a very good time to do so, as Lendy is offering 50 GBP cashback to investors that invest at least 1,000 GBP on the condition that this amount stays invested for at least 3 month. Lendy lists bidge loans secured by commercial property. The interest rates are typically in the range of 7% to 12% and the loan duration is typically 3 to 12 months. Currently a lot of loans are offered on Lendy’s secondary market, which will allow easy diversification into several loans upon signup.

Lendy is open to international investors. While a UK account is not mandatory, I suggest opening a UK bank account online via Transferwise – this will make things easier, if multiple UK marketplaces are used (my article on Transferwise Borderless account).

NEO Finance is the leading P2P lending platform „Paskolų klubas“ in Lithuania. The platform is an intermediary for consumer loans connecting lenders directly with borrowers. We believe that fintech company should be not only innovative, but also professional. This is why we gathered a strong team of senior experts from the banking sector with the expertise in consumer lending, bank management and risk control. Currently all of “NEO Finance†activities are supervised by the Bank of Lithuania due to obtained e-money license, P2P license and as a consumer lender status, to ensure that responsible lending criteria is enforced.

We have a unique platform that we developed our self to fit the needs of our investors. NEO Finance offers buyback and provision fund services, which minimizes risk for lenders. Moreover, partnership with Legal Balance, UAB enables platform’s users to experience the benefits of 7+ years of delinquent loans recovery know-how.

By transferring money to “Paskolu klubas†account investors deposit it into e-money IBAN account under their own name and hold all of the money under their control till the investment is made.

Our main goal is to ensure a sufficient supply of loans are listed in the primary market, so that our investors can cherry-pick the loans adequate to their investment strategy.

What are the three main advantages for investors?

Provision fund service. By voluntarily paying a provision fund fee, more conservative investors can be secured from delinquent or defaulted loans. If a borrower is late with the installment, provision fund immediately covers that installment. The fund holds largest amount of proceeds to cover late payments in the Baltics and holds more than 100 000 EUR at the moment.

Buybacks. Investors, who did not choose the provision fund service, can sell defaulted investments to “Paskolu klubas†for 50-80% of its face value. Instead of waiting for a relatively long recovery process they can reinvest their money into other loans.

Higher interests rates of return. In Lithuania, we operate in market of higher interest rate. Currently our average interest rates are as fallowed for each of the credit rating: A – 13 % B – 17% C – 20%. This creates opportunity for investors from all over the Europe to receive higher returns.

What are the three main advantages for borrowers?

Lower fees for borrowers. As our fees are one of the lowest for borrowers, therefore half of the borrowers choose “Paskolu klubas†loan as an alternative for a bank loan.

Possibility to get an instant loan. Since we developed in-house state-of-the-art IT platform ourselves we can offer unique features for borrowers and investors. One of them is instant loan service. Investors can set up their automatic investment tool and borrowers can see what amount they can borrow at what rates, as the system collects all automatic investment orders starting with the lowest rate and building it up to meet the needs of a borrower. This feature enables investors to invest their capital faster.

No upfront fees. Unlike other platforms Paskolu klubas does not charge upfront fee from borrowers. Borrowers do receive the exact amount they borrow. Platform fee is deducted from the payments, this way we take the risk together with investors and are able to offer barrows flexible barrowing.

What ROI can investors expect?

10-18% after taxes. One investor did an experiment with 4000 EUR initial deposit. Half of the investments were made using a provision fund service, 5 defaulted investments were sold to NEO Finance and some investments were sold in the secondary market with premium. ROI after exactly 1 year was 14% after taxes.

Is the technical platform self-developed?

Yes, this allows us to add various new features and to fit the needs of both – investors and borrowers. We are not only the peer to peer platform, but also a fully licensed e-money institution. This enables us to operate as an online bank with IBAN account numbers and SEPA MMS payments.

How is the company financed? Is it profitable?

The company is financed from shareholder’s equity. It is not profitable yet, but we are in operation for only one and a half year. Our current goal is market penetration and market share.

What were/are the main challenges in the Lithuanian market?

When preparing for the launch, we spent a lot of time carefully analyzing Lithuanian and foreign markets. “Paskolu klubas†shareholders and employees have a lot of experience in the financial sector, we also cooperate with the best partners and agencies. This helped us to be prepared, therefore none of the challenges were unexpected.

One of the more significant challenge was financial literacy. Potential investors were not introduced to peer to peer lending before. Therefore, we started an event and training cycle where we educate investors about pros and cons of peer to peer lending.

You launched the company for residents of Lithuania quite some time ago. What prompted you to open up for international investors and launch an English version of the website right now?

From our experience, we knew that establishing consumer loan brand in a market takes at least a year. We focused our effort on becoming the number one platform in Lithuania for the past 18 months, but had strategic plans to open our platform to international investors from the beginning. Currently we can supply enough of quality loans for international investors.

Another reason was it took time to acquire full e-money license. For this we had to make sure we meet international anti-money laundering requirements and international identification requirements. Only after establishing processes, developing the system and meeting those international requirements we are ready to offer opportunity for international investors.

Which marketing channels do you use to attract investors and borrowers?

For investors, we mostly use educational channels where we try not only to advertise, but also to educate people about investment opportunities. In 2016 we organized over 30 events for our investors. We also use partnership of different financing experts who can provide feedback on our platform and receive bonuses for the investors they bring in.

Moreover, word of mouth perfectly works for us, because we have many satisfied investors, who are sharing their experiences and helping us grow.

For the borrowers, we have fully integrated marketing campaign. We use all traditional and digital channels. We invest in brand building and acquiring quality borrowers. This helps us to acquire valuable borrowers, who are worth to invest in.

Where do you see Paskoluklubas in 3 years?

We see Paskolu klubas as a global player in P2P lending sector. We may establish borrowing sites in other countries, but we will localize it as we did with Paskolu klubas in Lithuania. We see advantages of strong brand in each country we operate for borrowers. We are currently on a path of fast growth and we are not looking to slow it down. Our goal for next few years is to be the number one platform for investors in the Baltic states.

Investors can use the Paskoluklubas referral code P2PBANKING when registering and get 10 Euro for their first investments.

Property based p2p lending marketplace Proplend will launch its IFISA offer on May 30th at 9am. Initially the IFISA product will only be made available to those existing investors that had signed up to Proplend until May 26th. The new IFISA investors will have the same choice of loans secured by income producing UK commercial property and the same 1,000 GBP minimum investment opportunities as non-ISA investors. Depending on selected tranche, which differ by LTV, the interest rates range from 6.3% to 9.3%. The Proplend IF ISA will be flexible and allow tranfers in and out.

Since launching in 2014 Proplend has facilitated 11.7 million GBP in loans and has experienced no defaults so far.

P2P lending marketplace Zopa announed the plan to roll out the new IF ISA from June 15th to existing customers with target rates of up to 6.1% and also that from December 2017 new lending will not be subject to the Safeguard Fund.

Investors in Zopa Core will lend in the same risk markets as Access and Classic (A*-C) but will not be covered by the Safeguard fund. Zopa Core will offer a higher target return of 3.9% after fees and expected credit losses, as compared to 3.7% and 2.9% for Classic and Access.

The Classic and Access product offers will no longer be available for new customers, but existing customers can continue to lend through these products until 1st December, when they will be retired.

The Innovative Finance ISA (IFISA) will be launched in four phases: 1. The first stage (from 15th June) will be focused on existing customers who want to open a new IFISA (limit of 20,000 GBP) and lend through Core and Plus. 2. The second stage (1st July 2017 to 31st July 2017) will enable existing customers to sell their current loans and re-purchase similar loans in an IFISA wrapper. This will allow investors to retain Safeguarded loans in the IFISA. Any investing through new lending, or relending as capital is returned, will be onto Plus or Core only. 3. The third stage (from August 2017, but dependent on meeting demand for new IFISAs) will allow existing customers to transfer existing ISA investments with other providers to Zopa. 4. And finally, once we have met demands of existing customers, we will welcome investments from new customers.

From December 2017, new lending will not be subject to Safeguard. All loans that currently have this coverage will continue to receive it.

Zopa today says it initially introduced Safeguard in 2013 to deal with a tax anomaly that unfairly penalised peer-to-peer lenders. The fund was designed to ensure that investors only paid taxes on the net income they received from Zopa borrowers: and not bad debt. In 2015 the tax laws were updated enabling investors to claim for relief on losses from bad debt. As a result, the primary reason for Safeguard was removed. However in 2013 the Zopa website claim differed: ‘Zopa has created the Safeguard in order for you to get back all your money plus interest – without having to worry about a borrower paying you back. The Zopa Safeguard was created to step in and give you back all the money owed to you.’

Last year, based on customer demand, the company introduced Zopa Plus product without Safeguard coverage. Plus has proven popular and since March 2017 Zopa have been operating a waiting list for new investors due to the very high levels of demand. Zopa says that retiring Safeguard will allow the platform to provide greater target returns than Access or Classic (2.9% and 3.7% respectively, versus 3.9% in Core and 6.1% in Plus).

Andrew Lawson, Zopa’s Chief Product Officer, said: “We’re proud of our 12-year track record of prudent lending and have always provided positive returns to our customers. Safeguard was introduced in 2013 to deal with a tax anomaly that had led to peer-to-peer lenders being unfairly penalised. Since winning our campaign to change the tax rules, we no longer need Safeguard – as customers have proved by flocking to Zopa Plus. Now it’s done its job, retiring Safeguard, allows us to provide greater expected returns to our investors (because on average we over-fund Safeguard) whilst making the investor products even easier to understand. We’ll continue to maintain Safeguard for the rest of its life, and continue to build on our reputation for world-leading credit risk management.â€

P2P lending platform Relendex today launches its Innovative Finance ISA (IFISA). Relendex is fully-authorised by the Financial Conduct Authority (FCA). Â The UK Government introduced the IFISA in April 2016 and was created to sit alongside existing Cash, Stocks & Shares and Lifetime ISA products.

The Relendex ISA will work in a similar way to its regular accounts. Â Lenders will decide which loans to invest in and can build their own diversified portfolio of loans. Through this IFISA, lenders will enjoy tax-free returns on loans secured against UK property.

Michael Lynn, founder and CEO of Relendex explains why the Relendex IFISA is a viable alternative to other ISA products on the market: “Many people have built up a significant nest-egg in their tax-free ISA but in the low-interest environment Cash ISAs are only earning around 0.5% pa and Stocks & Share ISAs are potentially quite volatile and therefore investors’ capital is at risk.  A secured lending P2P ISA is the best of both worlds. The yield is good at between 6 and 10% pa, tax-free and there is considerable capital protection in the form of security over independently-valued UK property assets. Of course property values can fall, but since our average Loan-to-Value is around 60%, the property concerned would need to fall 40% on average before any loss would result.

So if ISA investors are thinking of using this year’s Annual ISA Allowance or transferring existing ISA funds to a Relendex IFISA Account, they can build a diversified portfolio of good quality loans and achieve a good yield. They can also reinvest the gross interest, to achieve compound growth and build their capital.â€

The Relendex ISA is a non-flexible ISA. This means that all new subscriptions made during a tax year will count towards your subscription limit for such tax Year and cannot be replaced. Michael Lynn, explains:

“Our lenders see us as a longer term investment, although we do provide a secondary market if they decide to sell on early.  A non-flexible ISA recognises this longer-term demand and allows us to offer the ISA without any fees. Also, ISA holders are responsible for adhering to the HMRC annual ISA Allowance, so we track their subscriptions so they don’t inadvertently exceed their annual allowance with us.â€

While there is an annual limit for new ISA subscriptions of £20,000 (for 2017-18 tax year), there is no maximum statutory limit to the amount that exitsing ISA money can be transferred across to a Relendex IFISA account (although we set a £10,000 minimum transfer value).  Transferring ISA investors will need to complete a Transfer Authority Form.  There is no need to get in contact with your existing ISA Manager as the Relendex specialist team will handle the entire process for you.â€

Asked by P2P-Banking.com about the sales expectations regarding the IFISA product Lynn replied: ‘We will be disappointed if we don’t bring in at least 1 million GBP in the first month subject to how fast transfer-ins of existing ISAs will flow through from ceding managers. Longer term it’s difficult to put a hard number on it but our conservative target is at least 10 to 15 million GBP in the first year.‘

Further questiones whether he expects deposits to come mainly using this tax year’s allowance or rather as transfers from amounts from the previous years, Lynn answered ‘The high base of existing ISAs (with over £200 billion sitting in Cash ISAs alone) strongly favours transfers.   But we also expect all transferring holders to utilise their current year annual allowance.’.

P2P-Banking also asked: ‘Should investors consider moving money from an S&S ISA to the Relendex IFISA?’. Lynn said: ‘We are not in the position to advise on individual portfolio allocations but do believe that we offer an attractive product on a risk/return basis. Obviously secured lending at relatively conservative Loan to Value and diversification does provide a good degree of capital protection for investors and a good yield. The good news is that S&S ISAs and IFISA are not mutually exclusive, so investors may consider allocating to both.’

To date Relendex states it has experienced no defaults and has maintained an average yield of 8.78% pa.

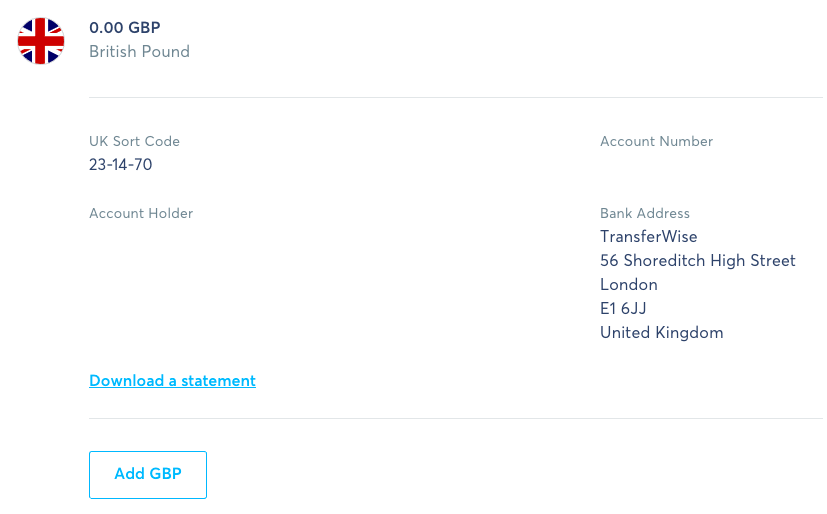

I have written several times about how useful it would be for international p2p lending investors if they can setup a free UK bank account or a free EUR account in the SEPA zone. My last article on this topic was here. Now it seems the final solution has arrived. Transferwise just announced that they offer a new Transferwise borderless account which will hold up to 15 currencies and offers local bank accounts in GBP, EUR and USD. The account is advertised as free (no setup fee) and without any monthly fees. See below though.

This is a viable solution for p2p lending investors that are investing on p2p lending marketplaces outside their home currency and seek an account to withdraw money to in order to transfer it to a different p2p lending marketplace without converting the money in the process.

Screenshot: Transferwise borderless account

Transferwise does charge fees per local transfer. 0.50GBP or 0.60EUR for each transfer.