Spanish p2p lending marketplace LoanBook announces a new partnership with Sage, provider of cloud accounting, payroll and payments software, to offer Sage’s Spanish customers a direct, in-product channel to alternative finance.

As part of the collaboration, Sage will offer its SME and accountancy customers access to LoanBook’s working capital loans, both in-product and within Sage’s wider ecosystem, stating Sage’s customers will benefit from a dedicated loan request portal enabling LoanBook to access customer data in order to improve the quality and speed of its loan underwriting.

James Buckland, CEO of LoanBook, commented: ‘We are excited to go a step further in our collaboration with Sage with a direct in-product integration. This partnership is based on the shared vision and commitment of Sage and LoanBook to support the SME community in Spain in becoming more competitive through improved access to finance and to innovative technology solutions.’

LoanBook has lent 21 million Euro to Spanish SMEs during the last 12 months and says it if providing a net annual return of over 5% for its investors.

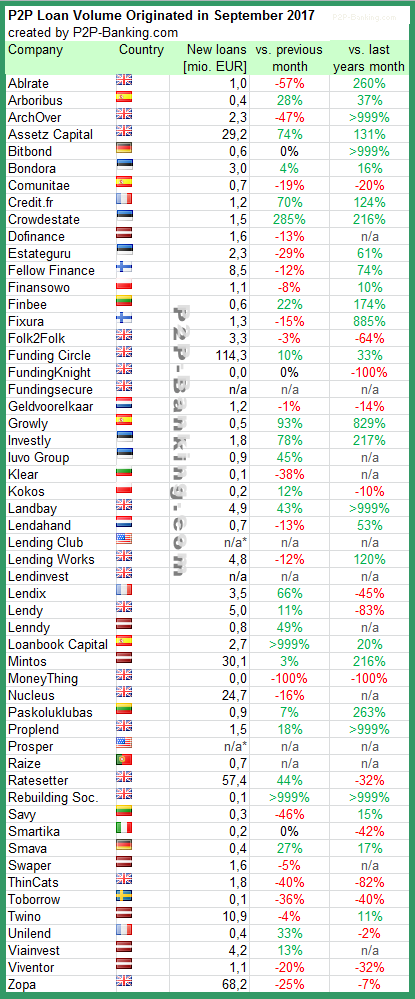

This p2p lending statistic table contains the loan originations of p2p lending companies for last month. Funding Circle leads ahead of Zopa and Ratesetter. The total volume for the reported marketplaces adds up to 404 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending services.

This month I added Raize, a marketplace in Portugal.

Want to meet representatives of many of the listed companies? Attend Lendit London in October – use discount code WiseclerkVip to get a 15% rebate on registration.

Table: P2P Lending Volumes in September 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

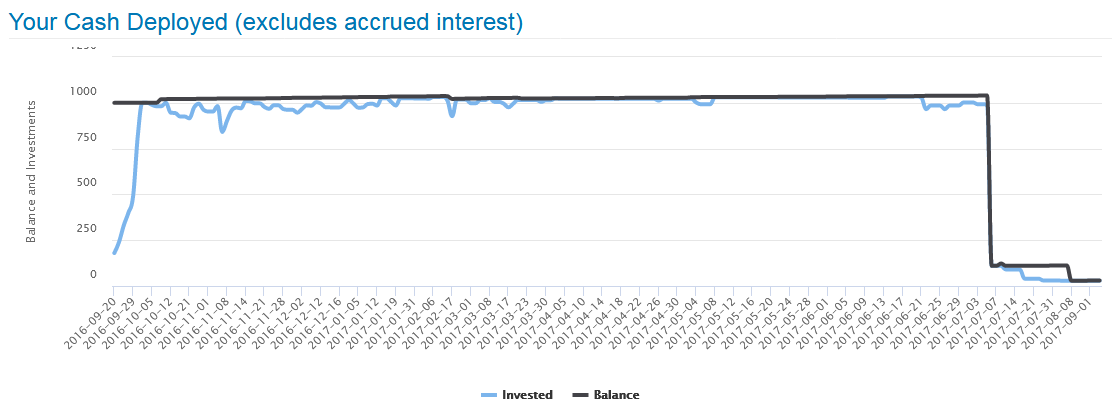

Last year in September I signed up at UK platform Bondmason in order to test first-hand how an investment of 1,000 GBP would develop. As described in the review article, I wrote when I started, Bondmason is an aggregator that automates the investment across many p2p lending platforms for the investor and takes a fee for that. Bondmason projected a target return of 7% after fees and bad debt.

Allocation of my deposited funds into loans went okay. There was some cash drag, but not as much as other investors have experienced.

Deployment speed of my investment on Bondmason – click for larger image

What was bad, was that it became clear to me, that the interest level in combination with the non-performing loans would make it very unlikely for Bondmason to reach the projected return – at least for my portfolio. Especially with the Invoice Discounting loans there were issues.

In April 2017 Bondmason announced it would require a larger minimum investment amount of 5K (previously 1K) and raise fees for small portfolios to 1.5% (previously 1%). Dang. I was in no way interested to deposit more money. So my portfolio did not even get to celebrate 1st anniversary. In July I gave them notice to liquidate my portfolio/account. Since then I withdrew 1,013.94 GBP – only slightly more than I deposited. My account still exists as there is 20 GBP stuck in two property loans in default and also 1.41 GBP in cash.

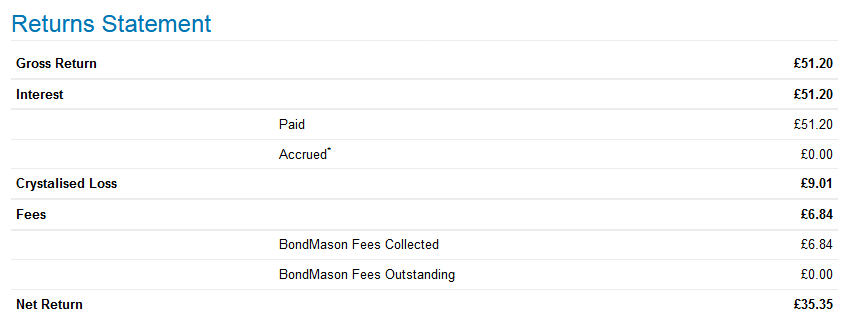

My Bondmason result (1) – click for larger image

My Bondmason result (2) – click to enlarge

Regardless of which way I look at it, the result is clearly bad. Obviously Bondmason by far missed the targeted return of 7% in my case. If I take an optimistic view and just assume, my 2 defaulted loans would recover today and the outstanding amount is paid to me, then my self-calculated yield (XIRR function) would be 4.3%. If I need to write off the 2 loans in default then my self-calculated yield is 1.9%. And that is before tax – as a German resident I cannot offset bad debt against interest earned for tax purposes. And on top of that the pound has been detoriating against the Euro value in the past 12 months (not Bondmason’s fault).

So to sum up: I liked the idea of an aggregator and the Bondmason setup allows passive investing in a diversified mix of p2p loans. But my returns are among the worst I ever experienced on p2p lending platforms and I am certainly happy I conducted this test with 1,000 GBP only and did not risk more.

If you want more details about the development of my portfolio throughout the past year there are more snapshots with screenshots over time in this thread.

Peer-to-peer lending platform Fellow Finance is now open for borrowers in Germany. Wirecard Bank supports the Finnish FinTech company Fellow Finance to enter and provide a digital infrastructure for the German financial market. Wirecard Bank will place their German full banking license at the Fellow Finance’s disposal and in addition enabling a completely digital credit process.

Under German regulation (KWG) only banks are all allowed to make loans, meaning all p2p lending platforms need to partner with a transaction bank.

It is not a full p2p lending offering as investors cannot invest into the German loans on the platform. And Fellow Finance states in their TOC that they do not advise borrowers regarding the loans. So it looks to be an attempt to capitalize on the reach of the brand. The website for the German market is running on the national domain Fellowfinance.de. Update: While the German website explicitly states that retail investors cannot invest, the wording might be misleading and actually might mean only that investors need to go through the Finnish site in order to invest. On the Finnish site the ability to filter for German consumer loans and to set up allocators (autoinvest) for German loans is present.

Jouni Hintikka, CEO at Fellow Finance, says: “We are looking forward to working with advanced Wirecard Bank as a co-operation partner in the future. We are proud of the entry into the German market after having already proven our business model in Finland and Poland. This is again one step of making Fellow Finance the biggest consumer and business lending platform in Europe and proves the scalability and flexibility of our platform.â€

Thorsten Holten, Executive Vice President Sales Financial Institution and FinTech Europe, adds: “Gaining Fellow Finance as a customer means that we can expand on our collaboration in the area of alternative lending with the aid of an international partner. With our expertise in the areas of banking and regulations, we help FinTech companies such as Fellow Finance to enter the market in the best way possible as well as to quickly and easily internationalise their business.â€

In future, Wirecard Bank will support Fellow Finance in the scoring of potential borrowers and carrying out payment transactions. This means that end consumers in Germany will be able to quickly apply and raise a loan in competitive interest rate.

The German market is very competitive and so far p2p lending marketplaces have found out it is not easy to compete with the banks. In Germany Auxmoney is the largest p2p lending marketplace offering consumer loans.

The table lists the loan originations of p2p lending marketplaces for last month. Funding Circle leads ahead of Zopa and Ratesetter. The total volume for the reported platforms adds up to 391 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Milestones reached this month are:

Bondora reaches 100 million Euro in financed loans since launch

Want to meet representatives of many of the listed companies? Attend Lendit London in October -use discount code WiseclerkVip to get a 15% rebate on registration.

Table: P2P Lending Volumes in August 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Today I gained another 1,7% after selling an investment that I did held only a few days. I started using the Spanish property platform Housers in the beginning of August. On Housers investments into property in Spain and Italy are listed. Mostly the offered structure is that investors will benefit from rent income from the property and also capital gains achieved, if the property is sold at a higher price at the end of the investment period. The concept will sound familiar to those that are using the British platfrom Property Partner. But there are other offer types too, including fixed interest investments. The minimum investment is 50 Euro and terms range from 12 months to 5 years and longer.

There is a lot of information and statistical data about the properties and the property market in that town and neighborhood. The platform is easy to use. After signup, the investor needs to upload scans to verify identity and to connect a bank account. Deposits can be by bank transfer or credit card. I made a small withdrawal of 0.50 Euro via SEPA transfer to test withdrawal and the money arrived after 2 days in my bank account.

Current bonus: Sign up via this link and get 50 Euro bonus when you invest 50 Euro. Ends today (August 31st)! The bonus can only be invested, not withdrawn. Additional cashback of 1% on all credit card investments (you see that after you select a property to invest into. Ends today (August 31st).

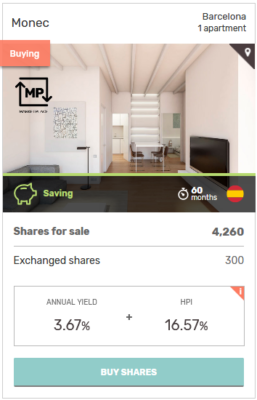

Housers has a secondary market. Only properties in the “Saving” category can be traded – with the “MP” logo style mark. Sellers can set a premium (or) a discount. When I started in the beginning of August I had 50 Euro invested in the Monec property (pictured right) and wanted to try out selling. So I listed that at 1.74% premium and was astonished that it sold quickly. I had exited that investment only 8 days after making the bid. Granted the absolute profit was not spectacular: 78 Cents (50.87 Euro sales price minus 0.09 Euro sales fee – Housers charges 10% of profits), but it was 1.56% profit in 8 days. Mathematically that is an (X)IRR of 102%, but of course one can not calculate it that way as a reinvestment without breaks will not be possible and not every time a buyer will snap the part that quickly.

Nevertheless I got curious, if I could scale that somewhat and employ a strategy of flipping, that is investing and then selling fast at a premium. I invested in more parts of an Italian property opportunity (“Breda” in Milan). Yesterday the secondary market for this opportunity opened, and today I sold the first 100 Euro part for a 1.89% premium. I have listed the next 100 Euro part for 1.99% premium now.

There are three main factors for selling in my view:

Premium (typically buyer will buy the part currently listed at the lowest premium)

Part size: only full parts can be bought. I would expect it to get harder the larger the part is (but the seller can list part of his total holding, as long as it is at least the 50 Euro minimum)

availability of other offers, especially on the primary market

I have yet to experience a time where there are no offers on the Housers primary market. It will be interesting to see how that effects demand on the secondary market.

The majority of investors is from Spain, but Housers says there is large demand from investors from Latin America, too. I like the platform interface, it is easy to use. The UI is available in Spanish, English and Italian language.

Another property investment platform in the Eurozone offering a bonus is Estateguru. If you register via this link, you get 0.5% cashback on all investments in the first 90 days. Investments on Estateguru are into secured loans, not equity.

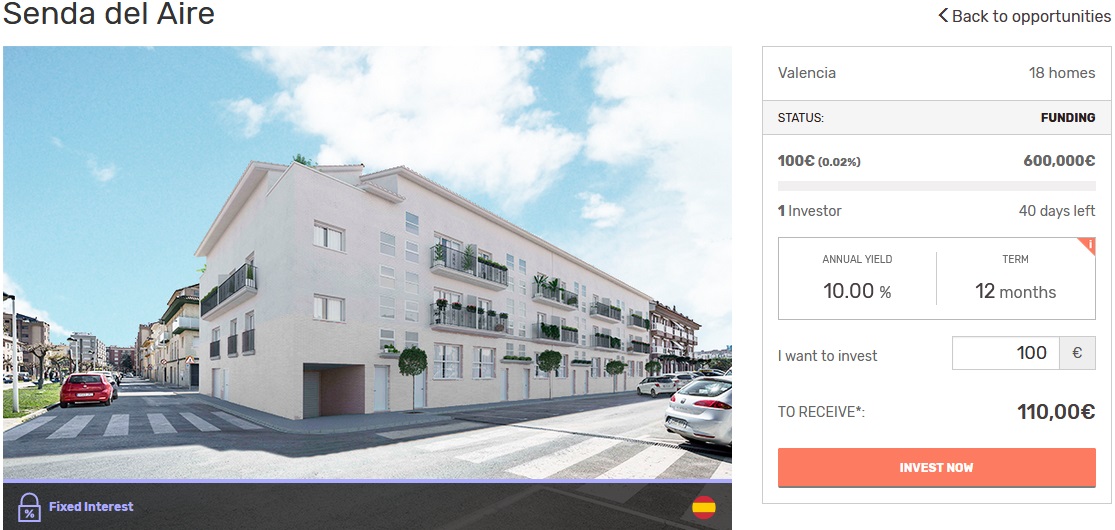

One of the property investments listed on Housers in the past