This p2p lending statistic contains the loan originations of p2p lending companies for last month. Funding Circle leads ahead of Zopa and Ratesetter. The total volume for the reported marketplaces adds up to 539 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending services.

Thincats reached the milestone of 250 million GBP loans originated since launch.

Table: P2P Lending Volumes in October 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Assetz Capital is now the UK’s second-largest peer-to-peer business and property lender and also the second largest in Europe. Since 2014, we have been providing competitive loans to credit-worthy SMEs and attractive returns to investors. We provide fairer and more accessible business lending to small and medium sized businesses and property developers throughout the UK.

Since our launch, we have lent more than 350 million GBP to credit worthy businesses whilst providing returns of 30m GBP to our investors using a number of automated investment accounts that earn gross rates of return between 3.75% – 7% per annum and also permitting manual lending at rates often above that. Almost all funding to date has come from retail investors and maintaining support for retail investment is one of our business aims.

What are the three main advantages for investors?

Firstly, we only lend to businesses who we assess as credit worthy businesses with tangible assets. Tangible security is taken for each and every loan – which is unusual for peer-to-peer lenders – in order to reduce the risk of capital losses for investors, while also lowering the cost of borrowing for businesses. We also deploy traditional credit assessment techniques rather than rely solely computer-based borrower assessments, meaning our processes are fast, meticulous and human. As a result of our processes, Assetz Capital’s expected loss rates are amongst the lowest in the industry (currently standing at just 0.35% across our live loan book).

Secondly, we cater for all types of investors. In the past four years, we have experienced strong annual growth year on year, and have attracted a wide set of sophisticated and consumer retail investors, as well as attracting family office and institutional investment. We believe it is because we have demonstrated excellent credit skills and loan performance, while delivering strong net yields.

Thirdly, we are also the only major UK P2P platform to still offer a manual investment option. This allows investors to choose exactly which borrowers to lend to, allowing them to cultivate a bespoke investment portfolio and choose appropriate levels of risk in their investments. For those wanting automated accounts, we offer a wide selection ranging from our Access Accounts to a Green Energy Account, all of which cater to those with less time to invest. This combination of accounts offers the type of control that an individual investor may require, allowing people to pick and choose from a wide range of individual loan opportunities, and also the ability to automatically lend if they are time-poor.

What are the three main advantages for borrowers?

Assetz Capital has been providing small and mid-sized businesses with flexible and quick access to funding for future business and employment growth with competitive rates.

Rather than being just a website with automated credit assessments, Assetz Capital is run by finance, banking, credit and lending professionals with huge industry experience, alongside our large UK-wide network of employed Regional Relationship Directors who visit potential borrowers and help structure the loans. I believe that this is unique to the P2P industry, and is reassuring to both business borrowers and lenders that behind the technology and website there are actual, qualified humans with relevant experience to help structure good quality transactions. Borrowers really appreciate the ability to structure their loan requirements face to face with experienced professionals instead of encountering the “computer-says-no†problem of today’s banking industry.

We’re also a lean business, and as such we have lower overheads than traditional lending institutions. Coupled with the fact that we only lend to credit worthy businesses holding tangible assets, this means our cost of borrowing for businesses is kept low.

With the uncertainty that has come with Brexit, we have found that our platform is overcoming some of the issues which many UK businesses are currently facing. We believe that fixed rate loans offer businesses a stable way to predict part of their finances, regardless of external market conditions. Brexit may put pressure on banks to reduce loan availability or raise rates substantially, but alternative finance providers such as Assetz Capital are continuing to offer fixed rate loans.

What ROI have investors made on average on the platform in the past?

As a business, we are totally transparent with our top-line numbers, and these are updated live in a prominent position on our website. In just over four years, investors on Assetz Capital have collectively earned gross returns of around 30 million GBP on their investments, relating to more than 350 million GBP in loans to date. We have a big announcement at the beginning of November that further endorses these results.

Assetz Capital has succeeded in growing loan originations sharply in the past 12 months. How did you achieve that and were intermediaries like brokers a major factor?

While much of our loan origination is organic, brokers have also played a vital role in referring many small and medium sized businesses to us. To date, more than 350 successfully funded projects have come through brokers, and we predict that this will grow to approaching 1,000 by the end of the 2018 year. In fact, this has been so successful, we are actively working to increase our broker network significantly in the next two years, and have recently revealed a strategy to further support brokers through a number of methods.

For example, our network of nationwide Regional Relationship Directors is supporting more brokers locally. We are also offering new product and pricing improvements to further build our relationships with brokers. Our face to face approach is very much liked by brokers and their borrowers alike and this is also a factor in our success, as is the experience of our team.

What will the soon to be launched Assetz Capital IFISA offer? Will it offer the same range of investments and interest rates as currently? Will the IFISA be flexible?

Now that we have achieved full authorisation from the UK regulator, the Financial Conduct Authority (FCA), we are preparing to launch our Innovative Finance ISA (IFISA), which should be ready by the end of 2017. While I can’t reveal all the details at time of writing, it will be highly flexible as it is an extension of our very successful model.  There is no intention to have any ISA fees for normal transactions and we also intend for our main lending investment accounts to also be available at the same rates in the ISA. We also intend to release our next generation investment dashboard that we believe will keep it at the forefront of the industry.

Will you soft launch it to existing investors first or will it be open to all from day one?

We will open the account to all comers straight away, not just existing investors.

I heard Assetz Capital is profitable? Can you walk me through some of the key facts of the financial side of the company, please?

Very few FinTech businesses are even close to breaking even, so it was a momentous day this year when we proudly claimed we made a seven-figure profit (GBP) for the last financial year to March 31st 2017. I believe that this is a testimony to our business model where we refuse to believe fast growth should be at the cost of profit and cashflow. While several others built their loan books up quickly with a more lenient approach to credit and very substantial levels of outside investment to cover trading losses, we took a more cautious approach to credit risk and built our entire business on an initial seed funding round of 1m GBP and Series A equity raising of just 5m GBP more. We have now lent similar levels to the whole of 2016/17 year in the first six months of this year and also booked profits of around the same as last year in this period. We have a healthy balance sheet and have just announced a new Series B equity raise that will bolster it further.

We had a very successful raise of 3.2m GBP on Seedrs in 2015, and now we are looking to fund a number of short-term capital expenditure projects, which are aimed to help the company continue its substantial growth. We believe that this may well be the last one prior to an institutional investment round or IPO but we will keep this under review and are really pleased to have not just delivered thousands of people great levels of interest through our platform but also delivered hundreds of investors a strong equity growth also as a result of the Series B being priced at 250% approximately of Series A carried out two and a half years ago..

What are your views on Brexit, the impact on UK fintech in general and on p2p lending in particular?

With the many political, regulatory and economic twists and turns of 2017, uncertainty continues. While many of those involved in business and investment are nervous, there are others benefiting and seizing on opportunities. Since the Brexit vote, no one is really sure of what the longer-term impact will be on businesses, investors or the UK market in general, however from the P2P market perspective, this has been an important year to further solidify its stature and firmly place it as a viable alternative to banks for both investors and borrowers.

We see that Brexit has actually had a positive effect on P2P, and all indications signal that the industry will benefit further in 2018 as a result of banks seeming to entrench somewhat ahead of the outcome being more visible. The impact on wider Fintech is more varied and we see a disincentive to set up in London to some degree for some businesses but for those here I expect they will take a wait and see approach. The possible loss of the ability to ‘Passport’ UK regulatory permissions across Europe or vice versa could be the major loss for companies intending to operate both here and in Europe.

The main issue is that the result of the Brexit vote is still some way off and indeed it is entirely possible we could see a continuation of the recent economic strength if Brexit turns out well economically and some real challenges if it does not. It is too early to call but the former would be my expectation on balance.

Where do you see Assetz Capital in 3 years?

Assetz Capital will continue to grow, to offer new and innovative products to investors and borrowers, and to hold true to our founding principles of fairness to all our stakeholders including investors, borrowers, shareholders and staff. We have already seen growth of around 100 percent year on year since 2014, and we believe that this rate will continue. We have very ambitious plans for the business, and certainly we see ourselves in three years as becoming one of the leading secured lenders to creditworthy businesses looking for additional funding as well as one of the top few P2P platforms for investors looking for choice, flexibility and fair, risk-adjusted returns.

We want to be recognised as being a real contributor to the economic success of the country, on several levels including helping house building volumes increase to address the housing shortage, helping businesses grow and increase employment, helping private investors earn more from their hard-earned capital, helping institutions deploy capital on market-leading risk return ratios and finally helping incentivise and contribute to a greater quality and breadth of financial education in today’s society.

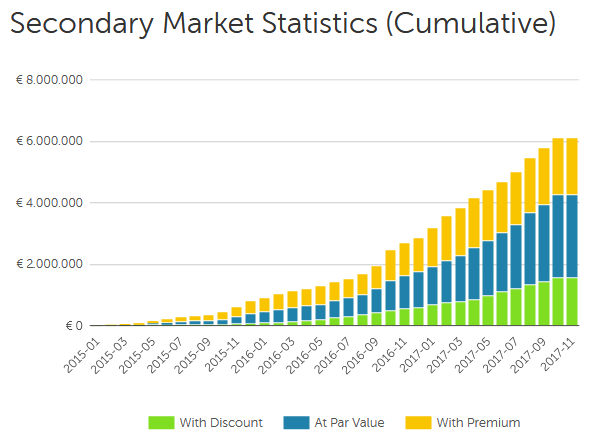

Latvian p2p lending marketplace Mintos announced today that all transactions on the secondary market are now free.

Exciting news! Starting from today, November 1, 2017, we have removed the 1% fee for selling loans on the secondary market of the Mintos marketplace. This means from now on, there are absolutely no fees for investing through Mintos.

“A secondary market with no fee will greatly benefit our investors. We expect the secondary market to become even more liquid now. This is especially good news for investors who want to pursue a long-term investment strategy and invest in loans with longer maturity. In the case investors will need the liquidity before the loan matures, they will be able to sell their investment with no extra fee added,†says Martins Sulte, CEO and co-founder of Mintos.

The monthly volume of traded loans on the secondary market is about 300,000 Euro per month.

Baltic Bondora stopped charging fees on its secondary market in November 2015.

With the majority of my p2p lending investments I hold the loans I invest in to maturity. Observing the market over the years I have observed patterns on the secondary markets that can be used to actively trade loan parts with the hope to increase achieved yields and I sometimes tried these.

I never specialized in this, so I never used fully automated bots, but did in some cases use some automation (Selenium or third party browser plug-ins). This article is not meant to be a how-to guide giving concrete instructions, that readers could just follow, but rather a list of things to consider and look for, should investors want to start testing strategies on the secondary markets themselves.

This article does not name or link any specific platforms, as I believe the same patterns and chances could evolve on new p2p lending marketplaces, and can be used there, you just need to look for them. Nevertheless all of the examples are real examples observed at the past by me.

Required market environment

The marketplace needs to have a secondary market that allows investors to buy and sell loans parts at premiums and discounts. Ideally without charging any transaction fees, but some strategies can absorb moderate fees. Furthermore it is advantageous if specific individual loans can be bought or sold rather than just random from the market or the investor’s portfolio.

The effect of premiums on yield

One central piece to understanding why trading (or flipping) strategies can be highly attractive is the effect of even small premiums pocketed on the portfolio yield. Take an investor that invests into a 100 (whatever currency) loan part and sells that part for 100.40 after holding it for 5 days. That is only a 0.4% premium, but the annualized yield is 33.8%. There is a big IF to that annualized yield number – it is only meaningful if the investor can seamlessly reinvest all his money in similar trades without any interruptions. So cash drag (effects of not invested cash) are very important.

The psychology

One would think that investors would always use rationale when investing into loans. However, I feel that a significant number of investors show one of these behaviors and the question an investor with a trading strategy should pose himself, is whether he can use that to his own advantage:

Scarcity If there is little left / available of a loan, investors fear of missing out

Unusual collector’s passion P2P Lending investors are told everywhere that diversification is vital (I tell them too). But especially on platforms with few loans, it seems that some investors strive to have a COMPLETE collection of loans in their portfolio and in pursuing that aim pay higher than average prices to acquire loans they ‘miss’ in their portfolio

Herd behavior Happens for example when investor (over)react scared by a news bit on a loan. In p2p lending that mostly effects the selling side rather than buying

Investors overvalue the realization of small gains Many investors are very happy to sell at small premiums –it just gives them a sense a positive achievement, not realizing that the market conditions for this specific loan part would have allowed selling at a higher premium

Blended by high numbers High nominal interest rates, and high YTM (yield to maturity) figures displayed by the platform overly attract investors

Two main strategy approaches

Investors can A) Invest on the primary market and then sell the loan later on the secondary market or B) Buy loan parts on the secondary market which they deem underpriced and then sell at a higher price. Be it buying at discount and selling at a lower discount, or already buying at premium and selling at an even higher premium.

While yields achievable in strategy B might be higher in percentage, this strategy is much harder to execute, as the competition will most likely use automated bots. Also the total market size for attractive loans will limit the scalability. I never tried strategy B on a larger scale myself. For example I was never found of buying already defaulted loans at a huge discount. Nevertheless I know of some investors that fare quite well buying defaulted loans and selling them at a lower discount, pocketing any payments and recovery that occur while they hold them as an additional bonus.

Following I will concentrate on strategy A) Invest on the primary market and then sell the loan later on the secondary market – as I have used this myself on several platforms over time.

One important point, is that market conditions change, usually good opportunities will stop working after a few months or weeks either because too many investors try to use them, or more general  the demand/supply ratio changes or the marketplace itself changes the rules how the market functions.

First an investor will want to look how loan information is presented on the primary and secondary market. Especially what sorting and filtering mechanisms there are on the secondary market. It is highly desirable that the loans the investor wants to sell later, will be listed on top of the list of all loans on the secondary market with either the defaulted sorting, or with an obvious choice of filtering (e.g. sort by descending YTM)

Understand the allocation mechanism on the primary market. How does the autoinvest feature work exactly? If there is no autoinvest, then are there chances to heighten the probability of investing in attractive new loans? Either through automation, or just because new loans are released at specific times?

When is interest paid? Does it accrue for each of the day held, or does the investor holding the loan at the date of the interest payment gets full interest credited. This is important, because if in the example at the start of the article the investor not only makes a 0.40 capital gain but also collects interest for the 5 days he held the part, it will have a huge impact on yield

Usually for this strategy longer duration loans are more attractive. This is simply because they will allow higher premiums without making the YTM value unattractive for the potential buyer

Usually smaller loans are more attractive. As there will be less supply it will be more liquid on the secondary market and more sought (see collector’s passion). No rule without exception. On one platform the biggest loans were the most attractive to be invested in on the primary market for the trading strategy. Why? Because this platform used dutch autions to set the interest rate and the bigger the loan the less the interest rate would go down. And of course loans with higher interest rates could later be sold at higher premiums

Usually the time span a trading investor wants to hold on to a loan part, will be as short as possible (days). However there might be patterns observed where it could be desirable to hold for longer time spans. For example if on a marketplace there are repeated alternations between lots of new loans and time without any new loan, it might make sense to hold the loan parts till there are no loans available on the primary market and only then offer them on the secondary market

Strategies that allow to hold parts only at a time when the status of a loan cannot change can be attractive. For example there was a time when it was possible to invest into very high interest, extremely high risk loans on the primary market of a specific platform and sell them at a premium BEFORE the first loan payment was due. Most parts sold within days, and the ones that did not sell at a premium, could be sold at par shortly before the date of the first loan repayment (this strategy worked due to a combination of factors: sorting by YTM, blended by high numbers (see above), and platform design – instant selling of loans offered at PAR).

So why is all this possible. Mostly due to market inefficiencies and lack of transparency and experience. The marketplaces are young, selecting and evaluating loan parts on the secondary market is not an easy task. And on many marketplaces investor demand outstrips loan supply . Usually the yields achievable with trading strategies go down as marketplaces grow (but the volume that can be used in these strategies might grow over time).

The most prominent question is, if an investor can scale strategies he uses to a level that is worth the time invested and the inherent risks.

Lendit Europe time of the year again. My fourth time as a particpant of the London conference. It is now marketed as an ‘Event for Innovation in Financial Services’ and that means a wider scope of topics – and presenting companies – than in earlier years, when it had a single focus on p2p lending / marketplace lending. I truly enjoyed the conference, it had quality sessions and its high level attendants (more than 1100) allow great networking and making interesting contacts.

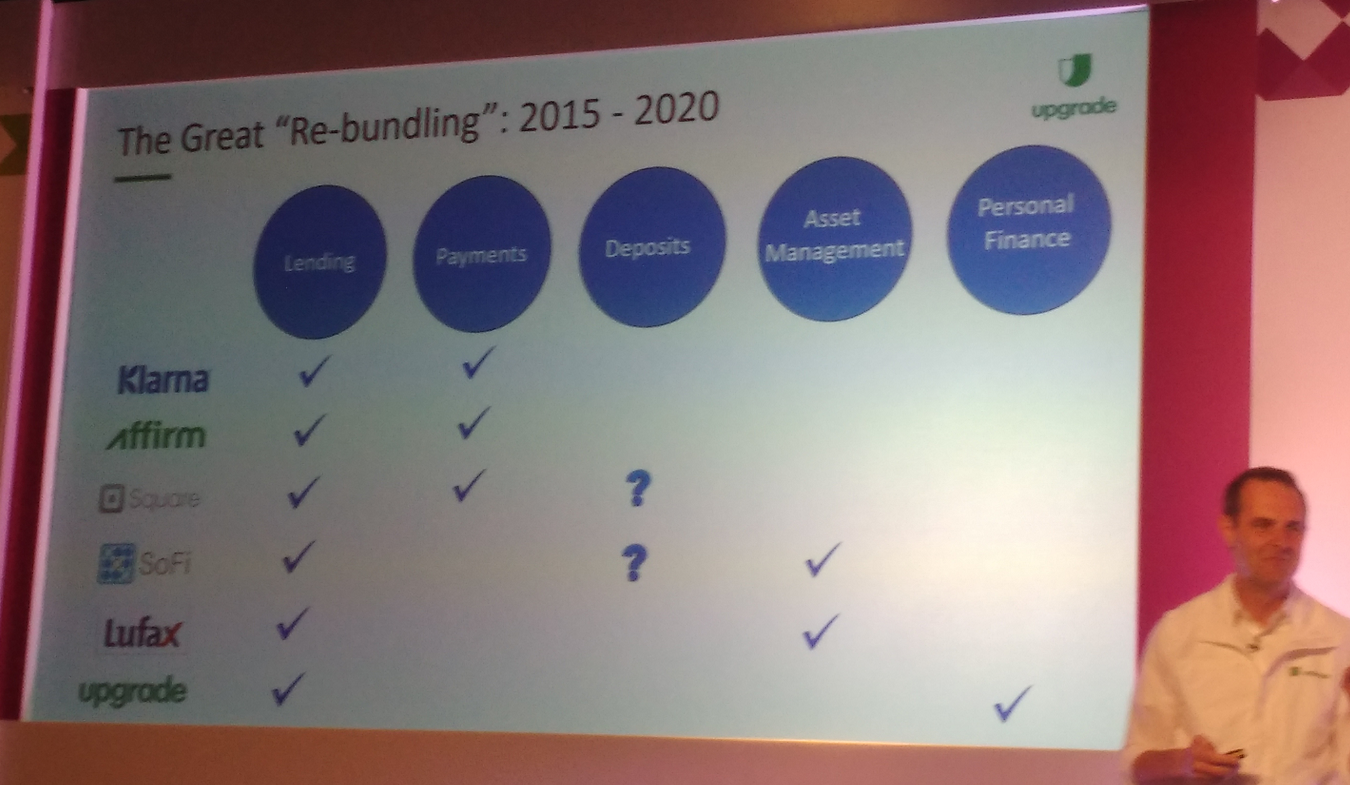

In writing this recap I find it much harder than in previous years to identify the main trends/topic that were discussed. There has been no single big announcement or issue happening that dominated the talks. So I’ll start with 3 predictions Renaud Laplanche, CEO Upgrade made in his motivating outlook on Online Lending 2.0:

Prediction 1: ‘The growth of online lending will accelerate in the next 15 months’

Prediction 2: ‘An organized secondary market for online loans will emerge in the next 15 months’

Prediction 3: ‘Continued re-bundling will give birth to at least one major consumer product innovation in the next 15 months’

From my viewpoint the first prediction is the one with the highest probability to come true, the second one is mainly important for the US market and it is actually the third one that is most interesting (but also most open).

His slide on rebundling examples

There are connections to another development that goes into the same direction and surfaced in several other sessions: More and more fintechs in this space are cooperating to better serve the customer and integrate multiple products into one user experience.

Furthermore there were several sessions around machine learning, artifical intelligence and automated underwriting with a wide range of opinions to what extend processes will be fully automated or whether human intervention or oversight is stll desireable for some specific decisions.

Looking at the scene from a geograhical perspective, many panelists emphasized that there are still a lot of difference between regions. The Americas, Asia or Europe (or even areas inside Europe) show a lot of differences no matter if the specific panel discussed funding, risk, investor yield, regulation or banking. So while many (especially VCs) would love to see fintech innovations that work globally and (if they are consumer faced) reach billions – that is extremly hard to achieve and therefore probably not going to happen in the near future.

This touches several speakers commenting and speculating whether the big tech giants like Amazon, Facebook, Google or Apple have ambitions and plans to offer financial services as they cater to a global audience, and what impact that would have on banks and fintechs. I found some aspects of this interesting, but mostly those discussions are futile because I feel there is such a lot of speculation involved and no real indicators that any of these companies are making steps in that direction. (sorry if there were any hard facts presented, I might have missed them as I did not see all the sessions).

I enjoyed Pitchit, where 8 startups battled for the vote of the jury and the audience. Swiss Sonect won both by hoping to replace ATMs by a platform approach where merchants can become the point where cash is dispensed (this is actually in collaboration with banks as they want to reduce the costs for maintaing ATM infrastructure and not anti-bank as it might sound on first impression).

All sessions at Lendit were recorded and will be made available over the next days here.

Seems like next year Lendit might come to a different location. The exit survey asked attendees to rate how they would like Frankfurt, Berlin, Barcelona vs London again.

Spanish p2p lending marketplace LoanBook announces a new partnership with Sage, provider of cloud accounting, payroll and payments software, to offer Sage’s Spanish customers a direct, in-product channel to alternative finance.

As part of the collaboration, Sage will offer its SME and accountancy customers access to LoanBook’s working capital loans, both in-product and within Sage’s wider ecosystem, stating Sage’s customers will benefit from a dedicated loan request portal enabling LoanBook to access customer data in order to improve the quality and speed of its loan underwriting.

James Buckland, CEO of LoanBook, commented: ‘We are excited to go a step further in our collaboration with Sage with a direct in-product integration. This partnership is based on the shared vision and commitment of Sage and LoanBook to support the SME community in Spain in becoming more competitive through improved access to finance and to innovative technology solutions.’

LoanBook has lent 21 million Euro to Spanish SMEs during the last 12 months and says it if providing a net annual return of over 5% for its investors.