On the p2p lending marketplace Mintos there is a very large and active secondary market. In my previous article I described that the YTM calculation shown on the secondary market is based on the assumption that the buyer holds the loan part till regular end of term and the buyer will achieve a higher yield, if he buys at discount and the loan is repaid prematurily.

In the article I will look into a possible strategy on the Mintos secondary market: buying overdue loans at discount.

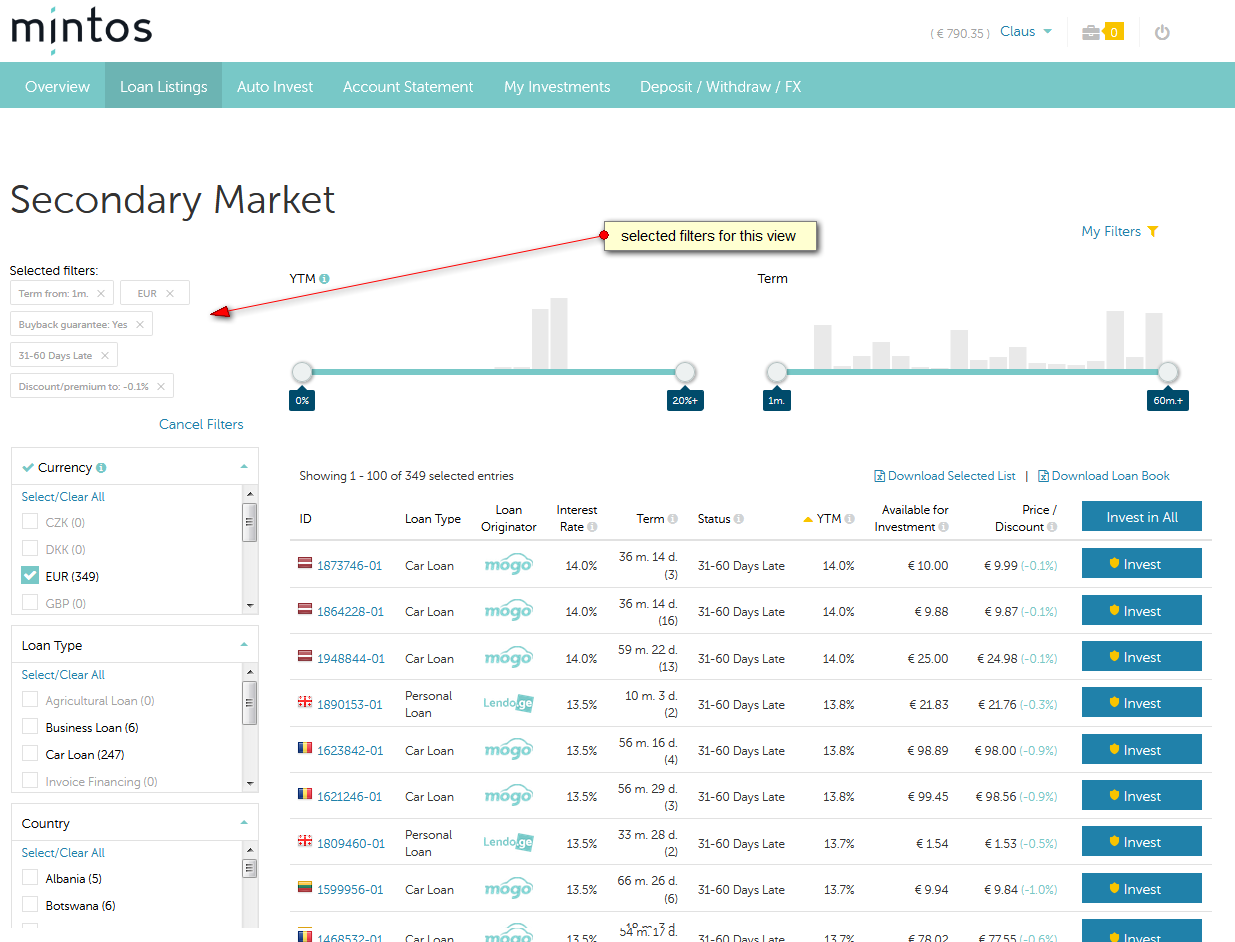

In a first step I sort/filter the buyback loans to only have those at discount that are very late (31-60 days overdue).

Click on image for larger view

I get a result of 349 loans with various discounts and an YTM of up to 14%. Not surprising for me, many of the loans listed at the top are Mogo loans. These are less attractive for buyers with this strategy. Why? Because they actually have a lower probability of defaulting. The paradox of this strategy is that the buying investor actually wants a high probability that the loans he buys default because that will boost his yield.

So in the next step I sort/filter to exclude Mogo loans. I also exclude loans that have a low YTM. This, because there is a chance that they do payup and then the buyer might be stuck with the loans for longer than 30 days.

Click for larger view

Finally let’s change the filter to require a minimum discount of 0.3% and there are 21 results:

Click for larger image

What would a buyer get?

If these loans do pay up and then run till regular maturity date, then he recieves a yield of 12.4% to 13.8%. Decent, but not very high compared to other Mintos loans.

However there is a chance of at least 50% that these loans will default and are bought back within the next 30 days. If that happens to a loan, that a buyer bought at 0.3% discount, it will boost his yield very roughly by more 3.6% (0.3% for 30 days multiplied by 12 to get annual effect). Likely it is more because the next payment date will be less than 30 days away. But even taking 3.6% the yield will be around 17%.

Looking at it, it is obvious that discounts as high as possible are preferable. The loan with the 0.6% discount would mean a boost of very rougly 7.2% yield on top (0.6*12). So that could lead to about 20% yield.

I have taken the screenshots for this article just at a random point in time. Higher discounts do happen and discounts of around 1% are not a rarity.

This is certainly not a strategy for a beginner at Mintos and it requires time and monitoring, but it is a frequently used strategy when investing on the Mintos secondary market.

Not yet investing on Mintos? Get cashback!

Mintos is offering 1% cashback on all investments made in the first 90 days after registration if you use this link to signup: Mintos registration. Currently there is an additional cashback offer for new and existing investors of 4-5% cashback on Mogo loans with loan durations of 48 month or more. Need to enroll once (click banner in dashboard after you finished registration). Expires Feb. 16th. The 4-5% roughly equals 1% increased yield.

Investly is an invoice financing platform which helps businesses from the UK and Estonia release cash from their long payment term invoices. We’re a marketplace that connects investors to companies that need short term capital, which we issue against their receivables. We have offices in London and Tallinn.

What are the three main advantages when investing in the invoices?

Liquidity – Investly is quite different compared to most platforms because the investment period is only 30 to 40 days on average. This means you can convert your investments into cash within a month by simply halting further investments.

Return – Historically investors have earned 11-12% annually on invoices. I believe every investor should have a portion of their funds allocated to P2P investing because of the higher return and additional diversification.

Added value – Invoice finance is helping small businesses who are growing fast but fail to get the support they need from local banks. The direct impact is clear – invoice finance has helped our customers grow faster and create more jobs. This would not be possible without investors.

What are the three main advantages for companies selling the invoices?

Most of all, faster business growth. We discovered that Estonian customers who are leveraging access to working capital are able to grow their turnover by 18.3%, while turnover growth benchmark equals 7.6% (Investly internal analysis, growth benchmark from Statistics Estonia report 2017) But access to working capital is not just numbers in spreadsheet, but most of all it’s opportunities that business can take: hire more staff and win new contracts, get better supplier payment terms by offering early or up-front payment, ensure prompt payment for employees and subcontractors.

What ROI have investors made on average on the platform in the past?

On average investors have earned double digit returns in both markets. The net return on Estonian invoices has been 11.2% annually and in the UK it’s been 12.6% annually.

What is the procedure, if a company is late in repaying the invoice?

To ensure collection is as fast as possible, we rely on early action and automating notifications to debtors. If the debtor doesn’t pay within 30 days of the due date, we have the right to ask the seller to repurchase the invoice from investors. We also ask for a personal guarantee from one or several of the directors of the seller company. This means that if the company cannot pay, we can ask for payment from the directors.

Investly is the biggest p2p lending marketplace for invoice financing in Estonia. How did you achieve this position?

We use personal approach and always try to find the best solution for our customers and investors. That professional customer service constantly provides us a leverage over banks and competitors. Also, quick decision – we present an offer within one working day. This is something that many of small businesses can’t expect from traditional lenders. On top of that, we have flexible pricing, which we’re able to use thanks to loyal and engaged investors community.

Investly is also operating in the UK. Is it complicated to operate in two different markets simultaneously and which of the two markets is more attractive for future growth?

UK is the largest factoring market in Europe with €327b worth of invoices financed every year. For comparison, France is second with €268b/year and Germany is third with €217b/year. This is where the biggest potential is. However, traditional sales and marketing channels towards our target customers are extremely crowded with thousands of B2B service providers trying to sell them products. We have to be more clever about acquiring customers there. Open Banking enables us to do that.

Estonian businesses finance only €2.5b/year, but due to the connected infrastructure of public and private registries, we can reach our customers much more easily. Also, there’s fewer providers in Estonia and we’re creating a lot of the market ourselves as factoring hasn’t been available for them in the past.

Having built Investly for four years, what do you deem the biggest assets of the company?

We have gained a detailed understanding about the problem we’re solving. It’s not specific to any geography. Businesses across Europe and elsewhere in the world are struggling with the lack of working capital. It seems that our product offering helps to solve that problem more simply than traditional lenders.

Four years is typically a good time to become an expert at something. We have also build a strong team to execute our mission. We’re experts at invoice financing.

Also, we’ve managed to get a good set of advisors on board to help us build the marketplace and secure future rounds of financing if needed.

What role does ‘Open Banking’ play in the near future for Investly’s further development?

Open Banking is a technical enabler. Businesses can now choose freely between their bank and 3rd party providers to solve their specific financial needs. It’s done in a secure and easy-to-use way.

This has gotten banks looking into how they can continue to be profitable in this new environment. Completely new types of business models are emerging and we’re proud that Investly is one of the early pioneers to set the path for others. Being part of the Open Banking sandbox in UK helped us to be one of the first ones to integrate with banks like Barclays, HSBC, RBS, Lloyds and Santander.

We’re going to use these integrations to form partnerships with traditional lenders so we can serve our customer without them necessarily having to change their provider.

You want to raise new funding on Seedrs. Why did you decide to use crowdfunding for equity rather than traditional routes?

Throughout the years we’ve received multiple requests from our marketplace investors to participate in our equity financing round. They’ve been giving us a lot of valuable feedback when we’ve developed our product and directed our credit model. We’d like them to get a chance to be part of Investly mission as we continue to grow.

With traditional equity financing, we’d be overwhelmed by administrative work to get the round closed and to manage those relationships later on. Seedrs has provided a good platform on which we can do that efficiently.

What is the value proposition for investors? Do you aim for a stock market listing? What is the likely time horizon?

Get to participate in our valuation growth. The interest you earn on the marketplace is quite stable, but the potential upside on the equity investment is much higher.

UK based investors can take advantage of the EIS scheme. It’s quite a big incentive on the tax side.

Seedrs provides a secondary market, which helps to create liquidity for our shareholders. This way, you don’t have to wait for years until the startup makes an exit or files for IPO.

Is Investly profitable? If not, when do you expect to reach breakeven on cash flow.

Operationally, we’re quite close to breakeven. The target is to get profitable in core activities in the next 6 months after fundraising round closes. But on a company level we will still be investing heavily into building out the integrations with banks to execute the momentum we’ve managed to build up.

For which activities does Investly intend to raise the used funds?

Partnerships and further automation. Few years ago, all the banks would turn us down when we approached them with suggestion of cooperation. But with Open Banking, this is window of opportunity for both of us: Investly provides working solution with better experience and price for customers, banks acquire competitive leverage on the market and are part of this fintech revolution. Therefore, funds from this round will be used on product developments which will allow us integrate with banks infrastructure and automate our processes even more with the increase in volume.

Where do you see Investly in 3 years?

Investly will be the major provider of invoice finance to businesses across Europe. It’ll be partly through partnerships (invoice finance powered by Investly) and partly through building out our own brand by continuing to deliver superior customer experience.

With that scale, we will have had enough data to build up a narrow AI for credit decisions. We have followed our roadmap for getting there. We’ll be better able to score companies and collect payments than competitors.

Investors will have access to debtors across Europe, which enables them to achieve a good diversification of currencies, countries and sectors.

Once we’ve received that scale, we will be able to deliver the best financing rate to businesses with our marketplace model, where banks are lending alongside with our investor community.

On the Mintos p2p lending marketplace the majority of investors invest on the primary market into loans, either manually or via autoinvest. But for the 29% of investors that do invest on the secondary market picking loans presents them with a huge choice of about 125,000 offers (no typo, really 125K loan parts on offer!).

Main characteristics of the Mintos secondary market:

no transaction fees

selling at discount, par or premium, adjustable in 0.1% increments

no minimum amount for buying, a buyer could make a partial buy of 0.01

seller and buyer each get credited interest for the amount of days they hold the loan; that means seller continues to accrue interest for an offered loan until the part is sold

good filtering

Sorting on the secondary market is preset to YTM (yield to maturity). This figure shows the yield the buyer would make (taking into account the discount or premium), if he would buy the loan and hold it to regular (!) maturity. Emphasizing regular is important since many of the buyback loans end prematurily, which would result in a higher than shown yield for loans listed at discount or lower than shown yield for loans offered at premium.

Generally YTM is a very good criterion for sorting an filtering on Mintos the secondary market and it is my most important criterion.

However there are exceptions, when taking the shown YTM at face value is not advisable.

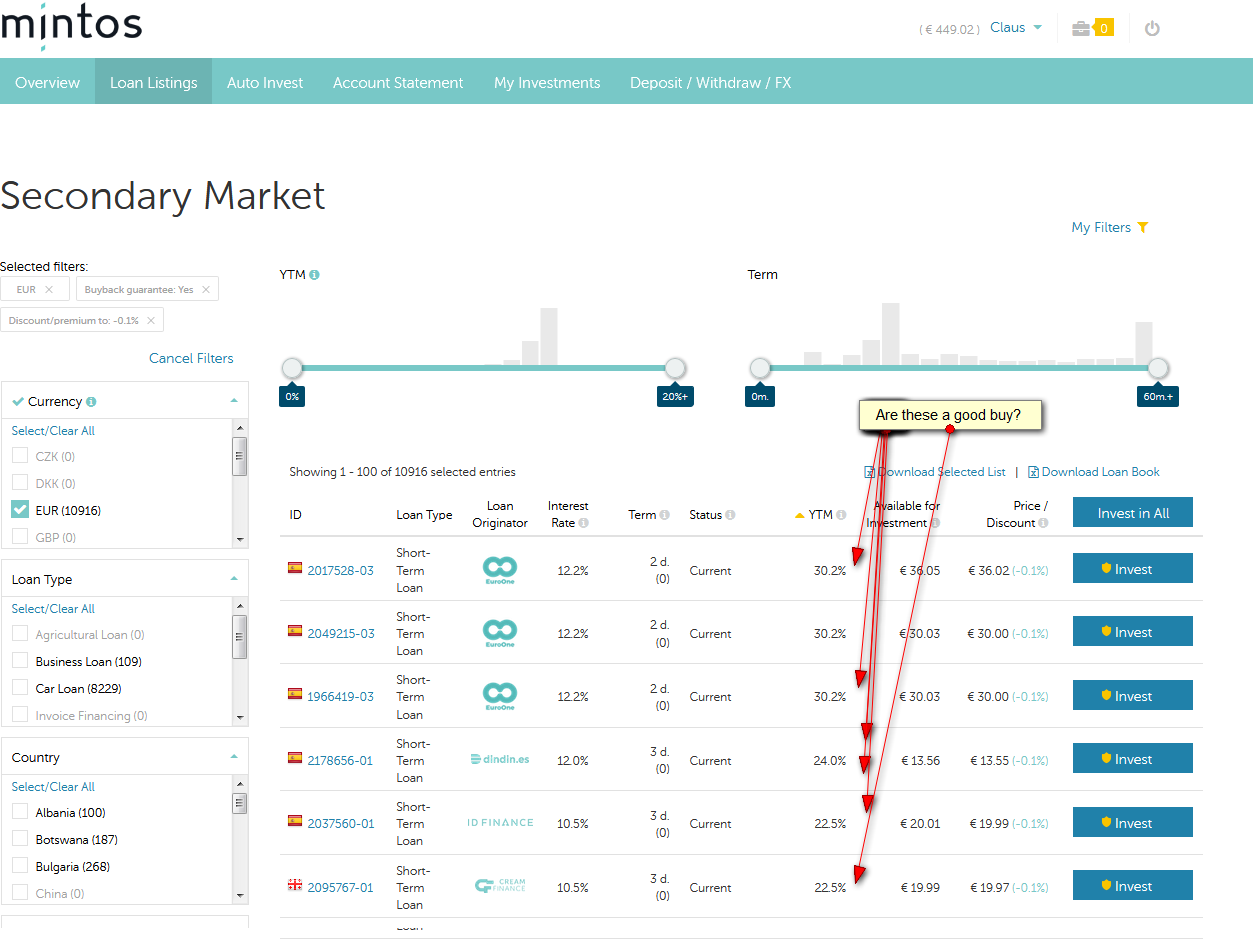

Click on image for larger view

Look on the loan offers in the screenshot above. All are offered at 0.1% discount and the YTM is very high with 22.5% to 30.2% Let’s neglect for the moment that picking these loans would cost the seller time, which if he puts a price tag on time spent would not be worthwhile as these loans are very close to maturity and he would only earn interest for a few days.

The high YTM is caused by the discount in combination with the fact that there are only 2 or 3 days left to regular end date of loan (term is 2d or 3d). The calculation is correct, but there is one caveat. For the shown loans there is a very high probability that they will miss the payment and therefore run an additional 60 days until they are repaid under the buyback guarantee. If that happens the remaining actual loan duration would be 62 or 63 days and the impact of the 0.1% discount on the YTM would be much smaller. The resulting YTM would be somewhere around 11 to 13%. So they would not be a good buy and there are much better offers on the secondary market.

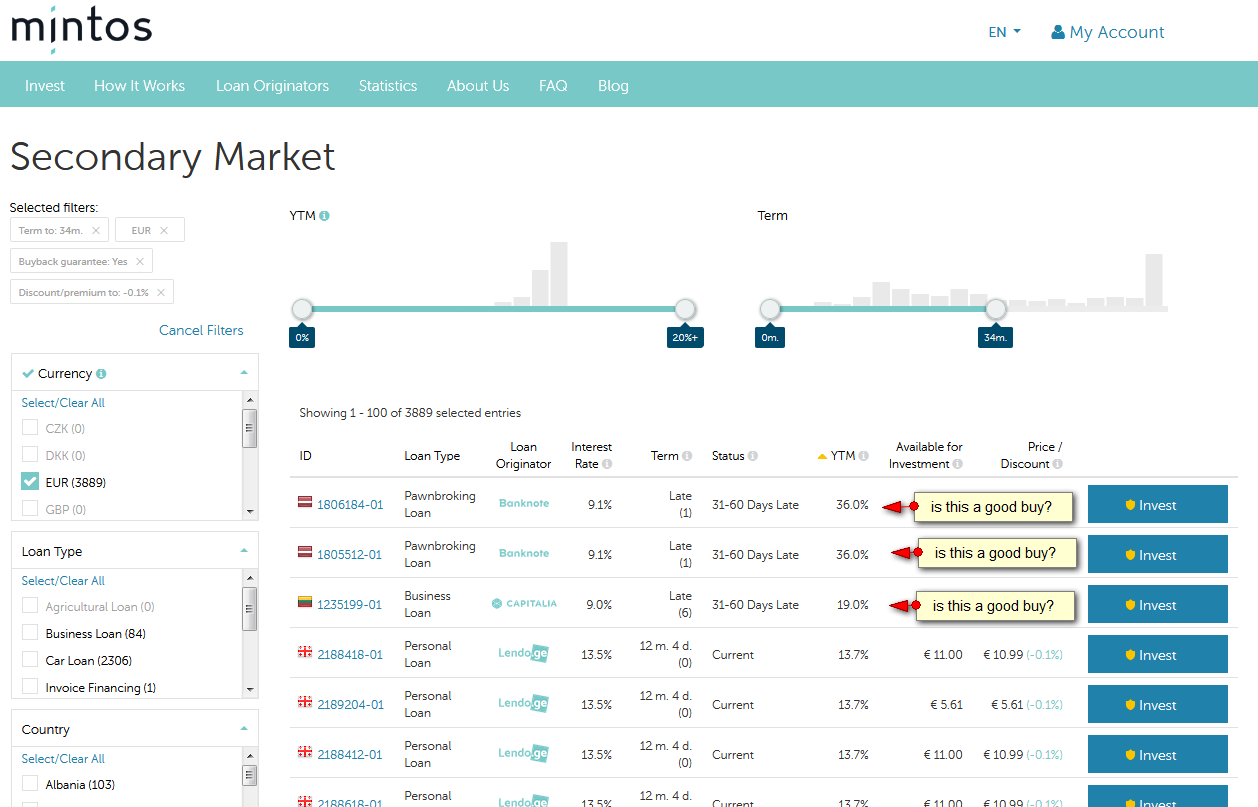

Another example to look at:

Click on image for larger view

These loans are shown with an even higher YTM of 36% and offered at a discount of 0.1%. They are late, but with a buyback guarantee, so aside from the originator risk there is no default loss risk. But for these late loans Mintos calculates the duration to the regular end of maturity with only one day, which in combination with the 0.1% discount results in the high YTM (simplified: 0.1% per days * 360 days results in 36% yield)

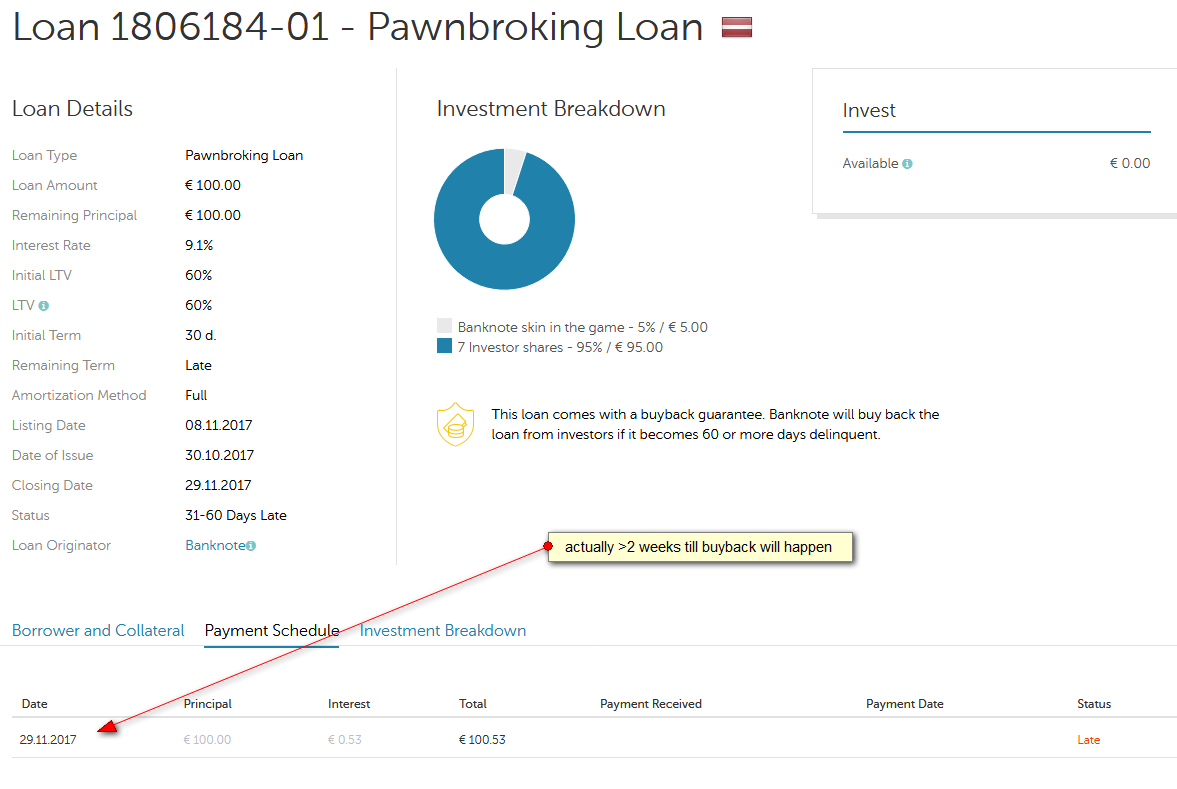

If I look into the details of one of these loans, I see that the next payment is actually scheduled in two weeks. So the loan will be repaid then since it is already in the status of 31-60 days late (there is a very low probability that it will repay earlier if the borrower repays).

Click on image for larger view

With two weeks remaining the effective YTM for a buyer is not 36% but rather around 12%. Again there are offers with better YTMs on the secondary market.

Conclusion

On the Mintos secondary market YTM is an important figure to regard for buyers. However, while it is calculated correctly under the definition, there are a few cases where the shown figure alone might be misleading especially in case of loans that have less than 1 month remaining loan duration. The shown YTM always applies to the case that the buyer would hold to the loan to the regular maturity date.

Not yet investing on Mintos? Get cashback.

Mintos is offering 1% cashback on all investments made in the first 90 days after registration if you use this link to signup: Mintos registration. Currently there is an additional cashback offer for new and existing investors of 4-5% cashback on Mogo loans with loan durations of 48 month or more. Need to enroll once (click banner in dashboard after you finished registration). Expires Feb. 16th. The 4-5% roughly equals 1% increased yield.

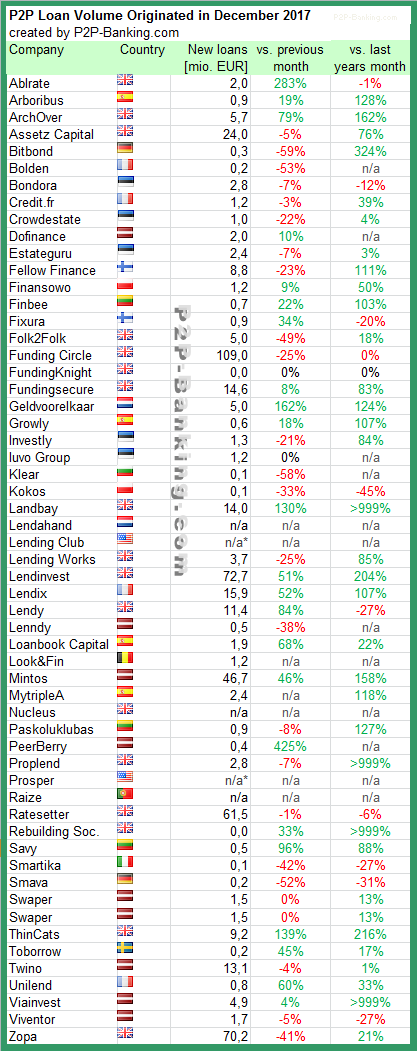

The table lists the loan originations of p2p lending marketplaces for last month. Funding Circle leads ahead of Lendinvest and Zopa. Mintos finished a remarkable month fueled by the cashback promotion. The total volume for the reported marketplaces adds up to 582 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in December 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Assetz Capital has launched the IFISA offer allowing UK taxpayers to use the 20,000 GBP tax-free allowance while investing on the p2p lending platform.

New and existing Assetz Capital investors can open an IFISA wrapper on the platform and then invest into any automated Assetz investment account in December. The IFISA is also set to include the popular Manual Loan Investment Account (MLIA) in the New Year.

The IFISA is flexible and offers investments into p2p lons with interest rates ranging from 3.75% to 12%.

Â

Stuart Law, CEO at Assetz Capital said: “Our IFISA …[is] great new tax-free investment choice for those that are new to peer-to-peer lending, but we also feel strongly about delivering a product that caters for our thousands of long-standing investors who prefer to choose their own loan investments within the Manual Loan Investment Account. That’s why we were determined to ensure that the MLIA will be allowed in our IFISA shortly after launch. … We will also shortly be releasing a queuing system in case we have excess demand for the IFISA that will allow our existing and faithful investors priority access to the tax free returns.â€

Today I take a look at how investor numbers are developing at several platforms. I chart relative numbers with the index set to 100 for October 1st, 2017. The advantage of using indexed numbers for this comparison is that platforms use very different definitions for their investor base size. Some count registered investors, some count investors with deposits, some count active investors, some count recently active investors, … .

The disadvantage of showing indexed numbers for growth is that it gives smaller, younger an advantage as their percentage increase of investor base is likely still higher because they come from smaller absolut numbers.

Indexed investor numbers (with Oct 1st, 2017 = 100). Reading example: On Dec 1st the index value for Mintos was 117, meaning Mintos had 17% more investors than on Oct. 1st