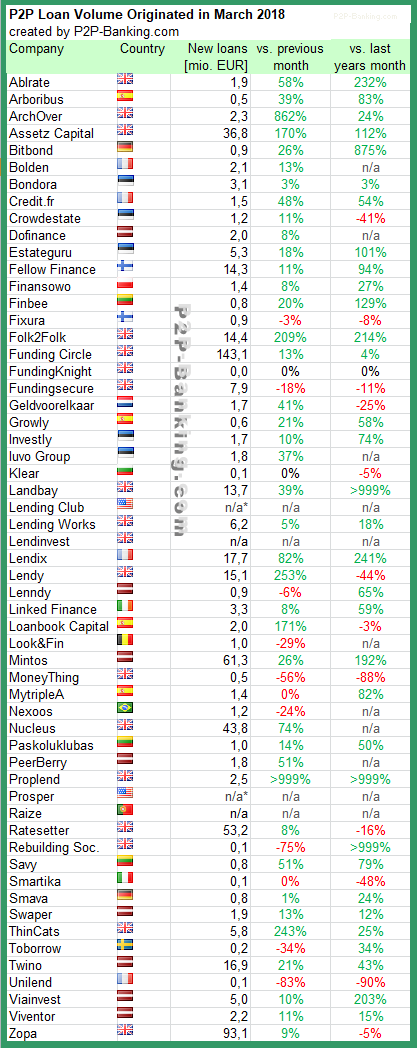

The table lists the loan originations of p2p lending marketplaces for last month. Funding Circle leads ahead of Zopa and Mintos, which is in the top 3 for the first time. The total volume for the reported marketplaces adds up to 599 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Milestones achieved this month (overall volume since launch):

Table: P2P Lending Volumes in March 2018. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

LendingCrowd has secured an external funding round of 2 million GBP following a strong 2017 for the p2p lending company, with the proceeds earmarked for ramping up its sales and marketing activities.

The round was led by angel syndicate Equity Gap and included a number of private investors from Scotland’s entrepreneurial and finance scene, and the Scottish Investment Bank. The company says it is on track to scale significantly during 2018 and intends to seek Series A funding over the next 12 months.

As part of its drive to build market position, LendingCrowd this month launched its debut television advert, designed to bring the opportunities available through P2P lending to a wider audience. The advert features Geoff, who decided to “Think Outside The Bank†and invest with the platform after becoming disillusioned with the low rates of return on other investments.

LendingCrowd has originated loan deals totalling 16 million to SMEs across Britain in the past 12 months period. For 2018, CEO and co-founder Stuart Lunn has set a target to more than double loan deals to around 40 million GBP. New clients in 2017 included Summerhall Distillery, producer of award-winning spirits brand Pickering’s Gin, restaurant chain Tony Macaroni and property lettings agency Umega Lettings.

Investor funds on the platform have grown rapidly, with much of the expansion attributed to the launch of one of the first Innovative Finance ISA (IFISA) products in February 2017. After a full 12 months of opening the LendingCrowd Growth ISA, 82% of investors have beaten the advertised 6% target return.

LendingCrowd, which is fully authorised by the Financial Conduct Authority, has over 4,500 investors signed up to its platform and is on track to significantly increase investor numbers this year. It now offers three IFISA products – the passive Growth ISA and Income ISA, and the active Self-Select ISA.

Stuart Lunn, LendingCrowd CEO and co-founder, said: “Having laid solid foundations for the business over the last couple of years, we now have a position in the market that is starting to pay dividends. We have a strong pipeline of both investors and SME demand and with such a strong trajectory, we are now actively speaking to the venture capital and private equity communities about our next phase of growth.â€

Jock Millican from Equity Gap said: “We are extremely pleased that our syndicate members once again backed LendingCrowd, with this raise being the largest single investment by Equity Gap to date. Existing and new investors in LendingCrowd recognise the progress to date and the potential for the business to scale.â€

Kerry Sharp, Director of the Scottish Investment Bank, commented: “We are delighted to provide continued support to LendingCrowd who have demonstrated real market traction with their innovative peer-to-peer lending platform in Scotland.â€

liwwa is a marketplace lending platform that provides funding to small and medium businesses in Jordan. Our mission is to support job and income growth in the region. To date we have underwritten about 10 million USD in loans. This has helped to create 475 jobs in Jordan, 1.77 million USD in income, and 13.05 million USD in economic output.

What are the three main advantages for investors?

The type of investors we target are financially-savvy professionals who already have a portfolio of investments. They are attracted to our service because it is a way for them to further diversify their existing portfolio. The other advantage is that there are no big barriers to testing out the platform – provided he meets certain basic criteria, anyone can register and there is no minimum amount required in order to start lending. Once an account is activated and the investor is ready to get started, the power of choice is in his hands. He is able to browse the various campaigns, read through the credit scoring and business information and select which ones to participate in. A final advantage to using liwwa is the relatively high returns; our Internal Rate of Return across the liwwa portfolio stands at 9.45% for the last 12 months.

It is important to note that the investment is unsecured and therefore a high risk one. This means that if a borrower defaults on his loan then the investor stands to lose any money that he has funded to that particular business and not yet been repaid. We aim to disclose as much information on this risk as possible throughout our website. We also keep investors regularly updated on progress to recuperate the funds in the event of a late payment from the borrower.

What are the three main advantages for borrowers?

There is a 240 billion USD capital access gap in the MENA region. For borrowers, we provide a much-needed alternative to bank financing. The liwwa financing proposition is attractive because we do not require collateral, and because we offer an extremely swift process. We are aware that most borrowers are in need of purchasing supplies or assets rapidly to continue growing their businesses. We commit to reviewing all applications within 48 hours. If an application is approved, the borrower is able to access funding straight away. And finally, we are transparent and we do not charge any up-front or additional fees. A Murabaha rate that an approved borrower is offered is directly related to the riskiness of his business, as determined by the credit assessment and the resulting credit score. Our friendly customer service team ensures that applicants are well informed throughout the process.

What ROI can investors expect?

The return on investment that investors can expect is directly dependent on their risk appetite. Generally speaking and assuming no defaults, an investor who puts all of his funds in low-risk campaigns is likely to make a lower IRR* than an investor who funds only medium- or high-risk campaigns. We encourage investors to diversify as much as possible across risk level as well as sector and loan tenor. Our current liwwa index stands at 9.45% for the last 12 months.

*The liwwa index reflects IRR, or Internal Rate of Return. More information on the Internal Rate of Return can be found at the following link: https://www.liwwa.com/help/irr

Is the technical platform self-developed?

The technical platform is self-developed to the extent that the proprietary data is all owned and managed in-house. There is a large focus on predictive modeling, and on collecting enough data to leverage this more in the future as a means for building efficiencies into the credit assessment process.

How is the company financed? Is it profitable?

The company has raised 5.55 million USD from investors and 6 million USD in debt to date. Our investors include Silicon Badia, Bank Al Etihad, DASH Ventures, and Samih Toukan. Our investors include a number of banking partners Bank Al Etihad, Capital Bank, Arab Bank, and Ahli Bank.

We will achieve profitability in 2018, and we are currently working to close a Series B round of investment.

What were/are the main challenges of the market you address?

IFRS 9, with its provisioning rules, is one of the main drivers of banks’ reticence to lend to SMEs. The market demand for loans hasn’t appreciably changed, and one could argue that market risk has stabilized in many MENA economies – so the accounting rule change is having an outsized impact. Companies like liwwa are poised to fill a need because much of the debt that liwwa manages is treated on an off-balance sheet basis. Retail lenders and non-bank institutions can contribute to filling the SME lending gap given a difference in risk appetites and a more generous perspective on solvency ratios.

Is Liwwa open to international investors?

liwwa is currently open to investors from the MENA region and Malaysia. We cannot unfortunately on board investors from other regions at this time due to strict compliance regulations imposed by some countries like the United States. We are working to be able to offer our services more widely in the future.

Which marketing channels do you use to attract investors and borrowers?

Our investors and borrowers are two vastly different audiences, and our marketing strategy reflects this.

For investors, marketing is varied and a combination of word-of-mouth, digital and more traditional forms of ATL advertising, the latter something we have recently started scaling up. We recognize that investors will want to know more about the company and want to trust in it before they start actively investing, and this make take time. Through all forms of advertising we encourage potential investors to learn more about us and we provide a lot of transparency to facilitate this. For example, anyone can read through our portfolio results www.liwwa.com/help/stats, or our blog blog.liwwa.com where we provide insights into how we work and articles on technology and investment.

For borrowers, social media marketing has been an important and cost-efficient tool for us. We also rely on a Sales team to spread awareness and build relationships with potential customers. As a result of our investment in maintaining customer satisfaction throughout the whole application journey, repeat borrowers currently make up nearly 50% of our portfolio.

Where do you see liwwa in 3 years?

The medium- to long-term focus is on continued improvements to our credit assessment process using technological efficiencies. In the next few years we will have a vast amount of data on the market that we can better leverage for predictive modeling. This means that we can gradually rely more on a combination of predictive modeling and manual credit assessments, minimizing the latter part as the former increases in accuracy.

This will contribute to making the liwwa model easier to replicate in other markets and, given the vast demand across the MENA region, we are targeting to roll out to other MENA markets.

We are still focused on our base of operations in Jordan, and the country will always be an important market to us.

Blend Network is an online property lending marketplace that focuses on lending to established property developers in high-growth areas across the UK but outside London. Since its official launch in January 2018, Blend Network has already lend £1.5 million GBP to 6 projects across Northern Ireland, Scotland and Norfolk with an average fixed return of 12.2% p.a. Lenders can join for free and manage their loans through a user-friendly dashboard. Borrowers are double-vetted by both Blend Network and a sponsor before being listed on the Blend Network platform. In addition, Blend Network loans are only made against security to help ensure the protection of lender money in the default scenario.

What are the three main advantages for investors?

Access to niche markets: While most P2P property lenders focus in the London market due to its convenience, we focus in less crowded markets outside London that are outperforming not only the London market but also the average UK market. We have done loans in Northern Ireland where according to the recent RICS UK Residential Market Survey Report the outlook is considerably more positive than in some other UK regions, with prices rising, a growing number of potential new buyers active in the market, robust demand and overall stronger sentiment. Similarly, according to the latest UK House Price Index data, Scotland was the only UK region where average year-on-year house prices in 2017 where higher than in 2016 (In England, Wales and Northern Ireland the pace of price growth moderated, although more significantly in England).

High returns: Our focus in high-growth, high-yield pockets of the UK property market outside London enables us to return up to 15% return p.a. – right at the top-end of the P2P lending marketplace. Our average return for the 6 loans since launch is 12.2%, significantly above the average of around 8% return across other P2P property platforms according to our own calculations.

Strong due diligence and credit risk assessment: We pride ourselves by the strength of our due diligence process. Borrowers are double-vetted by both Blend Network’s Credit Committee and a sponsor before being listed on the Blend Network platform. Our Credit Committee is chaired by senior banker Charles Lamplugh who has 35 years of experience successfully winning and running corporate relationships for Lloyds Banking Group. In addition, Blend Network loans are only made against first charge on the security as well as personal guarantee from the developer.

What are the three main advantages for borrowers?

Access to finance: Most property lenders pulled out in places such as Northern Ireland after the 2008 financial crisis and many haven’t gone back yet, but paradoxically Northern Ireland is one of the fastest growing UK property markets. For small developers in those markets, getting access to finance is simply not easy. Small and Medium Enterprise (SME) developers have the flexibility and the desire to build on brownfield sites, to redevelop derelict buildings and to maximise the potential of property which may no longer be viable for commercial use. Figures from the Federation of Master Builders (FMB) House Builders Survey 2017 suggest that a shortage of available small sites, combined with a lack of finance, top the list of barriers facing SME house builders.

We bring knowledge and understanding of developers’ true requirements: We operate in areas where the constrained nature of most mainstream lenders has led to many opportunities for small developers being delayed, frustrated or lost. In contrast, we pride ourselves for our understanding of the true requirements in the development process. As one borrower put it ‘It was very refreshing to work with a company that understood the process well so could recognise the opportunities available and thus able to finance accordingly.’

No exit fee for early repayments: If our borrowers are able to complete their project before the maturity, great! They can repay the loan with no exit fee. It’s a win-win.

What ROI can investors expect?

Between 8% and 15% fixed return p.a. Our average since launch is 12.2% fixed return p.a.

Is the technical platform self-developed?

The platform was developed for us, we own it.

How is the company financed? Is it profitable?

The company has been self-financed so far. It is profitable but we have just decided to take the whole team on an offsite to Miami, so we spent all our profit! J J

What were the main challenges when launching your platform?

Frankly, our main challenge so far has been trying to explain why the returns are so good! In today’s markets, there are not many investments that offer an average of 12% return p.a. with no volatility. One might think it is too good to be true. It is not. The simple answer is that the UK housing crisis and lack of available homes is at its worst since the 1970s, and small developers with tight access to funding are willing to pay a premium to get funding for redevelopment projects and bridge loans. This is why we can pay up to 15% return p.a.

Do you plan to offer an IFISA?

We will assess this later in the year and decide whether we want to implement an IFISA for the next financial year.

Is Blend Network open to international investors?

Yes, it is. Our current lenders on the platform include a range of nationalities across Western Europe, the Middle East and Far East Asia.

Which marketing channels do you use to attract investors and borrowers?

The platform has already attracted a string of high-profile lenders among the high net worth bankers and hedge fund managers of Yann’s circle of personal connections. These have lent nearly 1.5M GBP since the platform launched and the proposal is attracting significant ‘word of the mouth’ attention among current lenders. In addition, we have prepared a 2-year strategic marketing plan highlighting the relevance of branding, social media, PR but most importantly word of the mouth by current lenders who are more than happy to recommend the product.

What factors do you see impacting the British property market in the near future?

We see Brexit as a key challenge (or in our case opportunity) for the UK property market in the next 2-5 years. The UK property market is a 2-speed market, with on the one hand the London market and on the other hand the rest of the UK market. We believe the London market is set to undergo a further correction due to being directly exposed to a number of sectors hit with Brexit: the financial sector and the global elite’s appetite towards prime London property ownership after Brexit. On the other hand, the rest of the UK suffers from an endemic housing crisis and lack of available homes: after decades of failure to build the homes the country needs, public concern about housing is the highest it has been for 40 years according to several heavyweight reports into Britain’s housing crisis.

Where do you see Blend Network in 3 years?

At Blend Network we are not trying to reinvent the wheel; we are simply offering an improved product for both lenders and borrowers. While we don’t want to be the only P2P property platform in the market, in 3 years we certainly want to be the best in terms of:

Returns – keeping our current position at the top-end of the P2P lending marketplace

Customer experience – continuing to enhance the functionalities on our platform to keep delivering top navigational and interface tools that our lenders love using

Access to deals – Continuing to source top deals for our lenders

P2P-Banking thanks Yann Murciano for the interview.

The table lists the loan originations of p2p lending marketplaces for last month. Funding Circle leads ahead of Zopa and Ratesetter. The total volume for the reported marketplaces adds up to 454 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Table: P2P Lending Volumes in February 2018. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Yesterday evening investors on the Collateral p2p lending marketplace were informed via email by a letter by Gordon Craig that he was appointed administrator for Collateral (UK) Ltd, the company running the marketplace.

The company is continuing to trade under his supervision, but will not be facilitating any new loans and the secondary market is closed at the moment. Reason for the company going into administration is given as ‘The Company was operating in the belief that it was authorised and regulated by the Financial Conduct Authority under interim permission. It has transpired that this is not the case and consequently the Company has ceased lending‘.

Most reassuring for investors into loans is, that he states: ‘Please note that your investment is safe and this is a procedural and compliance issue. … ‘

Investors into loans do not need to take any immediate action. ‘I have lent money via the Collateral platform do I need to do anything? No. Subject to the borrower continuing to make payments of interest and capital those will be returned to you in accordance with the Collateral terms and conditions.’

At a later point it was clarified that uninvested cash and money invested in loans without drawdown is also safe:’ I can confirm however that any monies that are sat on the platform and are not invested are ring fenced in a separate client account and the intention is for these to be returned to all investors after the Administrator has obtained control of the bank account and carried out a reconciliation.‘

As P2P-Banking has learned, the individual loans are bankruptcy remote, with security held by a separate security trustee – Collateral Security Trustee Ltd.

Collateral has lent about 17 million GBP since the start, most loans were secured by property.

So that are the positive points.

It remains unclear to me how Collateral could have misjudged the regulatory status? The interim permission seems to have lapsed on January 29th. Again it is unclear whether it was actively revoked by the FCA. Investors analyzed yesterday that Collateral had quitely removed references to FCA authorisation (e.g. from email footer) after January 30th. Worse yet the company seems to have changed T&C materially and investors complain they were not notified about any change of T&Cs.

There is also the question why it was allowed to continue to operate from January 29th to February 28th, if it did not have the necessary regulatory approval (anymore). And the lack of communication (prior to the letter of the administrator which is comprehensive) is a disaster (see my previous article). Putting up a server maintenance note for two days, when you are going into administration is not the right way to do it in my opinion.

The adminstrator has not decided if the website will go live again ‘We are currently looking into the website and the possibility of this being reopened in order for investors to view the balance of their investments, however this isn’t something that will be dealt with until next week at the earliest.’

Several other UK platforms have emailed investors and informed them about procedures in place to reassure them that they have taken all the necessary precautions to be prepared in case of a situation like this.

To sum it up, while it is very unfortunate that a platform goes into adminstration with a chance that eventually it will go out of business, it looks like investors into loans will get off fairly lightly.

According to the FT the FCA commented it was ‘aware of the issue and working with the firm‘. The role of the FCA in this happening leaves some questions open for debate at the moment.