In my calendar I had marked October 2nd as the launch date of Globefunder.com. Unfortunately the day passed – no launch. I found a recent press release, which says launch will be in October and states Globefunder will launch for US lenders and borrowers. This is somewhat different from my early perception of the service, which based on the interview with Globefunder's CEO Brian Mullally. But the claim "Online, no-wait funding for qualified borrowers" does sound interesting.

No news on the other p2p lending services that have yet to launch, like Communitylend or Loanio.

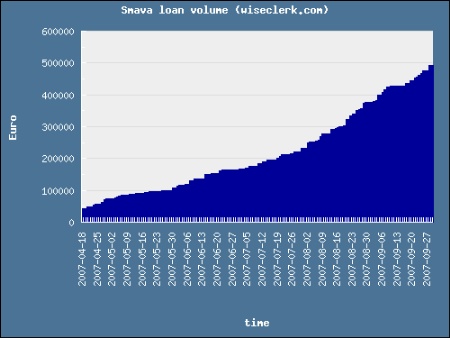

On March 24th Smava.de launched its peer-to-peer lending service in Germany. Time for a recap on how Smava fared in its first 6 month of operation. How Smava operates can be read in this earlier article. First the very positive news: So far in only 3 cases borrowers missed payment dates and in two of these cases the borrowers payed with only a few days delay. Therefore only one loan is currently late, resulting in that more than 99% of all loans are current. On the usability and interface side there have been no problems or complaints, the interface is working as expected. Thereis however room for improvement, especially in the account section where the handling gets a little clumsy once the lender has many loans.

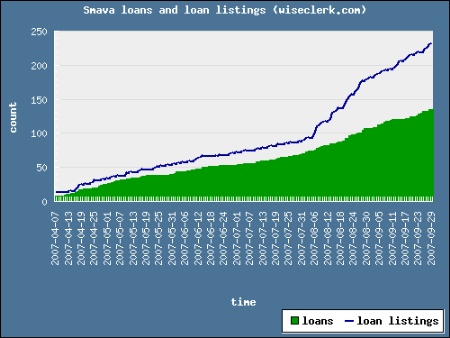

But despite receiving very positive and extensive media coverage Smava so far failed to achieve mass appeal. While Smava says it has over 13000 registered users, Wiseclerk figures show approximately 250 active lenders and 180 active borrowers.

In the 6 month Smava handled a loan volume of 500000 Euro (approx 0.7 million US$), rather tiny compared to the loan volumes Prosper and Zopa handle. One move to foster growth was that Smava opened to lower credit grades in the beginning of August. While this led to a rise of loan listings (see chart below), fewer of the new loan listings were funded. But still over 50% of loan listings do get funded. It is to early to judge how the low credit rate loans will impact the default ratio.

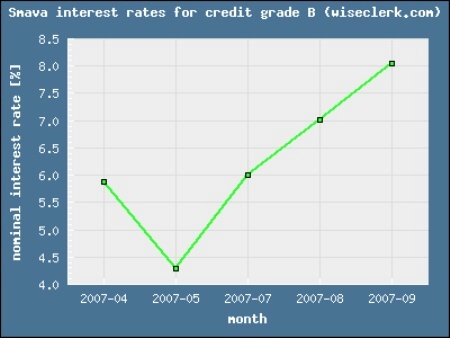

Possibly the main reason for Smava’s slow growth is the effficiency of German banking. German banks have automated the consumer loan process and small consumer credits have interest rates (APR) of as low as 4 to 5% (for best credit grade). At Smava the interest rates at which loans are funding have risen compared to launch date, voiding the argument that Smava offers better rates then a bank for many cases.

Smava is still faring well in the absence of serious peer to peer lending competion. With Dutch Boober troubled by regulation worries, the long announced plans of Boober to expand into Germany have yet to happen. Smava avoided regulatory problems in the first place because it partnered with a bank, which fulfils all regulation requirements.

Like Prosper Smava has yet to define the benefit of groups, which exist but have no plausible way of influencing/reducing the default risk.

MyC4.com switched today from closed beta to public beta. Now it is possible to browse the site without registering. For example click on one of the opportunities on the left of the screen and you get a good idea of the concept.

MyC4 allows lenders to do microlending to entrepreneurs in Africa. Lenders do get paid interest. Check the previous P2P-Banking coverage of MyC4.

Intruders TV did a long interview with James Alexander of Zopa.com covering the development of Zopa, regulation, market approach, lender and borrower advantages, the competition and other topics. The video starts of with polling passers-by on the street whether they heard of Zopa and would use peer-to-peer lending themselves.

(Source: Intruders.tv) P.S.: Noticed the bulletpoint on the whiteboard "Sell loan on phone".

Lenders at Zopa do not (yet) select an individual borrower but rather select a market and a rate at which they want to lend their money. This is matched to borrower demand and if a match is found, money is lend out.

There is a 3rd party site tracking the development of the Zopa demand volume and charting it (daily, weekly, monthly, yearly). Recently the amount requested has gone down in most markets.

Dutch Boober this week resumed full operations overcoming an imposed stop on lending. Lenders however now are facing even more restrictions. After a maximum amount of 39000 Euro was introduced for lenders earlier, a new rule now allows lenders to close no more than 100 loans. Since the minimum bid is only 5 Euro in the worst case that could mean, that a lender has to stop after lending out 500 Euro (100×5). Apparently this development means that the top lenders, responsible for 30% of Boober's total loan volume, are banned from lending more money. While lenders critizise this new development as overregulated forced by dutch regulator AFM, there is not much they can do about it. Theoretically each individual lender could apply for a license, but in practise license fees over 1000 Euro prohibit this move.

After a failed launch in May p2p lending service Frooble.nl now wants to lauch with a new concept. Borrowers can seek short term loans of 1 to 3 month duration for amounts between 50 and 500 Euro. Apparently these parameters have been selected to avoid falling under the regulation of the AFM. It remains to be seen if Frooble can thrive with this business model.