Swiss Cashare.ch recently launched as the first p2p lending platform in Switzerland. The company, owned by Michael Borter (link to German language interview) and Roger Mueller has partnered with the collection agency C&S Credit Management AG, which handles all monetary transactions. Interest rates and loan durations are set by borrowers and lenders bid in a 14 day auction (minimum bid amount is 500 CHF which is approx 500 US$). If the loan is fully funded further bids in the remaining auction period will cause the interest rate to drop in 0.1 percentage steps, while old bids are outbid.

The fee schredule includes:

For lenders and borrowers: 5 CHF fee for identification process

For borrowers: 19 CHF listing fee

For borrowers: 0.75% of the loan amount per year servicing fee

For lenders: 0.75% of the loaned amount per year servicing fee

This results in borrowers having to pay even if their loan does not fund.

An unusual point in the process is that lenders have to sign a written contract for each successful bid and send it via postal mail to Cashare. That seems a bit uncomfortable to handle.

As Cashare launched only recently there currently are only 4 active loan listings.

If you have used Cashare as a borrower or lender, please share you experiences in the forum. Thank you.

Surprisingly Lendingclub.com stopped signup for new lenders and existing lenders can not make bids on new loans (old loans are continued to be serviced). Borrowers can still obtain new loans – they are funded directly by Lendingclub. The announcement email sent out to members is quoted in this blog post.

Lending Club has started a process to register, with the appropriate securities authorities, promissory notes that may be offered and sold to lenders through our site in the future. Until we complete the registration process, we will not accept new lender registrations or allow new commitments from existing lenders. We will continue to service all previously funded loans during this period, and lenders will be able to access their accounts, monitor their portfolios, and withdraw available funds without changes.

The borrowing side of our site will remain generally unaffected by this registration process; borrowers can continue to apply for loans and new loans posted after April 7, 2008, will be funded and held only by Lending Club.

Until the registration process is completed, the company will undergo a quiet period and will not be able to respond to press and other inquiries about Lending Club or the registration process during that time.

On Techcrunch there is speculation that "Lending Club is looking to obtain a broker dealer license from the SEC that would legitimize its operations".

If this is the case I could not find a recent SEC filing connected to this. The last one I found dates February 13th.

Netbanker has a short statement from Prosper, essentially saying that Prosper believes itself to be in compliance with all state and federal laws.

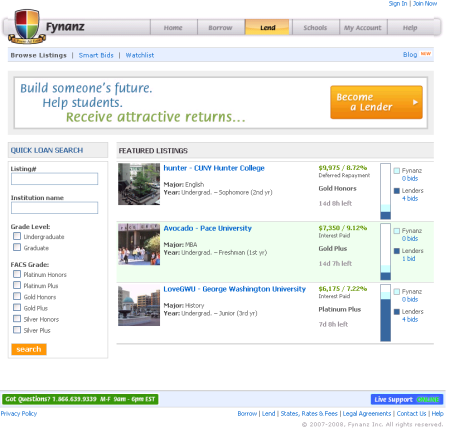

Fynanz.com, currently launching for borrowers in New York and Florida, offers peer to peer lending to students.

The service differs from other p2p lending service in many points.

The private student loans, also known as "alternative student loans", Fynanz offers have variable interest rates. Other p2p lending services so far operate only with fixed interest rates. At Fynanz interest rates are based on the LIBOR index, adjusted quarterly, plus a margin which is set by lenders. Suggested margins are 3 to 7.5% for a typical overall interest rate of 6 to 11% before fees. This is higher then federal student loans, but Fynanz still sees a large market, since federal student loans have borrowing limits and may not cover the entire costs of education.

Very long loan terms of 10 to 20 years. Again unsual, but lenders may offer to sell loans after one year at a discount to Fynanz. There also seems to be the option to transfer a loan to a different lender (allowing the sale to a different lender).

Students can select to defer interest payments while in school and for a 6 month grace period after leaving school.

Loan amounts range from 2,500 to 20,000 US$ per loans. Borrowers may take out up to four loans per year to a total maximum of 160,000 US$. That is an unprecedented amount in p2p lending.

The fees are pretty high in my opinion. Borrowers pay 2.9, 4.9 or 6.9% (depending on FACS) of the loan amount origination fee. Addionaly borrowers pay 1% guarantee fee into the guarantee fund until they have repaid 10% of the loan amount. Lenders pay a 1% servicing fee (not while loan is in deferment)

Guarantee for lenders. Not only in case of identity theft, but also in cases of defaults Fynanz protects 50 to 100% (depending on FACS grade) of the loan amount.

Fynanz applies it's own FACS grade (Fynanz Academic Credit Score) to rate borrowers. It not only relies on the credit history but also on academic charateristics.

Pledge bids allow lenders to bid without having funds in account. Lenders must transfer money within 5 days of bidding.

Fynanz has a "bid priority" that ranks four types of types of lenders in the following order: the highest priority lenders are friends and family of the borrower; then alumni of the borrower’s school; third are unaffiliated lenders; and fourth is Fynanz itself.

Hollowoak has some more interesting points from the lender agreement in his blog, which Chirag Chaman, Fynanz CEO commented on.

Prosper is America’s largest peer-to-peer marketplace with over 600,000 members,” stated Kirk Inglis, CFO of Prosper. “As credit markets experience unprecedented changes, institutional lenders, including hedge funds, are using Prosper to diversify portfolio returns without the lack of transparency and fees associated with structured consumer debt products.

Another recent Prosper related topic was the concern raised by lenders that in select states Prosper stops any collection activities on small loans, if the borrower sends a Cease-and-Desist letter (the example given is a 2,500 US$ loan in Texas). The author of the blog post argues that the risks for lenders rise, if this example really shows overall practise.

Moreover, they won't pursue legal action to recover small loans. So all small loans are now risky since the borrower has an easy method to halt payment, collections and legal proceedings. Prosper simply seems unwilling to go after small borrowers.

Finally, even for larger loans, it seems unsafe to lend, since Prosper will only sue in select states. I don't recall Prosper saying anything about selective enforcement in my many lender agreements, but before I put another penny into Prosper, you can be damn sure I will ask them what states they will take legal action in and what the minimum loan amount is for which they will sue.

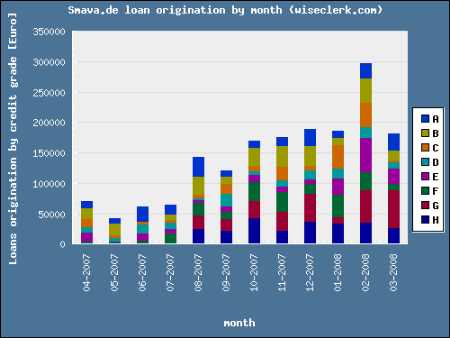

German p2p lending service Smava.de launched one year ago. Since the launch of Smava 393 loans were funded for a total loan volume of about 1.7 million Euro (approx. 2.6 million US$).

Lender’s viewpoint

In a february survey 33% of lenders answered to be very satisfied with Smava and 63% were satisfied. 48% said their ROI met expectations while 19% said it exceeded expectations.

So far a 7% ROI is realistic. Only 3 loans have defaulted and 11 are (less then 30 days) late. In the past Smava cured the majority of late loans. The Anleger-Poolmechanism spreads the losses of a default across all loans of a credit grade. Therefore when 1 in 100 loans in credit grade X defaults, the lenders invested in the defaulted loan still receive 99% of the principal, while for lenders in the current loans returns are lowered by 1%.

Technically and on the process level Smava functions as promised.

Borrower’s viewpoint

Provided the borrower has a credit grade of at least ‘H’ (95% of the German population have credit grades between ‘A’ and ‘H’ so about 5% are excluded) and he has a sufficient income, chances for obtaining a loan through Smava are good. About two third of the listings were funded. The fee of 1% of the loan amount that Smava charges borrowers is low.

Marketplace development

Smava’s growth has picked up in the last month (see chart).

So far Smava has not reached a broad appeal. While press release state 25,000 registered users, only 650 have invested money and roughly 450 wrote a loan listing. Looking at the distribution of lenders by amount invested, the top 50 Smava lenders funded about 700,000 Euro (or about 40% of total loan volume). Currently lenders are limited to a maximum of 25,000 Euro investment.

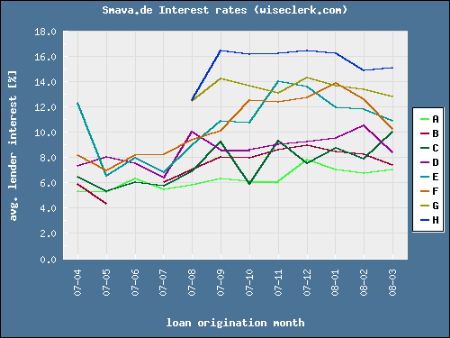

Attracting new borrowers has been the bottleneck for Smava’s growth so far. An increase of money supply by lenders with no matching demacnd increase led to slightly falling average interest rates in the last weeks (see chart). Before rates increased, especially for credit grade ‘F’ caused by sharpened risk awareness following several late payments.

Smava charges borrowers a fee of 1% of the loan amount. There are no fees for lenders. Total revenue of Smava in the first year therefore was 17,000 Euro (1% von 1.7 million Euro). Prosper, Lendingclub and Zopa have much bigger p2p lending volumes per year. Boober‘s loan volume in the Netherlands is about the same size as Smava’s but in a market with only one fifth the size (by inhabitants). First priority of Smava must be to accelerate growth.