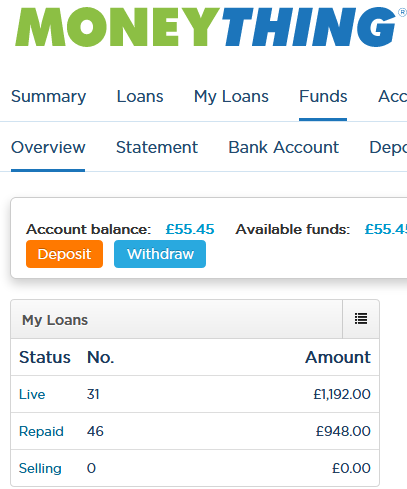

Last year I started investing on British p2p lending marketplace Moneything. Read my past article about opening a Moneything account. Moneything mostly offers property backed loans, with a few different asset-backed deals in between. I used Transferwise and Currencyfair to deposit money from my Euro account. Recently I also used the Revolut App to transfer money from another UK p2p lending marketplace to Moneything.

{kind=link}

So if all is great, why did I not invest more? Well, I planned to, but shortly after I started, Brexit vote took me by surprise and I abandonned my plans to ramp up my investment amount, due to the higher currency volatility uncertainty. Instead I am now mainly reinvesting funds and in addition add funds already in GBP, which I move over from other UK platforms via Revolut.

Earlier this month Moneything gained full FCA approval. This is the prerequisite for launching an IFISA product, which allows tax-free investing for UK investors (compare IFISA providers in our database). Surprisingly Moneything just said, they are in no hurry to launch an IFISA offer but rather wants to built loan originations first. This makes sense because the increased deposit influx by an IFISA offer would imbalance demand and supply even further.