Deutsche Börse Venture Network adds Swiss p2p lending marketplace Cashare to its program. The program by the German stock exchange is designed to aid innovatice companies to get better access to financing from investors.

Cashare was established in 2008 and facilitates loans to consumers and SMEs in Switzerland on its marketplace. According to the website 1,111 loans have been financed. Due to regulatory reasons each loan can be financed by a maximum number of 20 different investors.

Prof. Dr. Andreas Dietrich of the Lucerne University of Applied Sciences and Arts, Simon Amrein, Reto Wernli and Dr. Falk Kohlmann have published the study ‘Crowdfunding Monitoring Switzerland 2015‘. It analyses the development of crowdfunding in Switzerland giving special attention to the development of p2p lending.

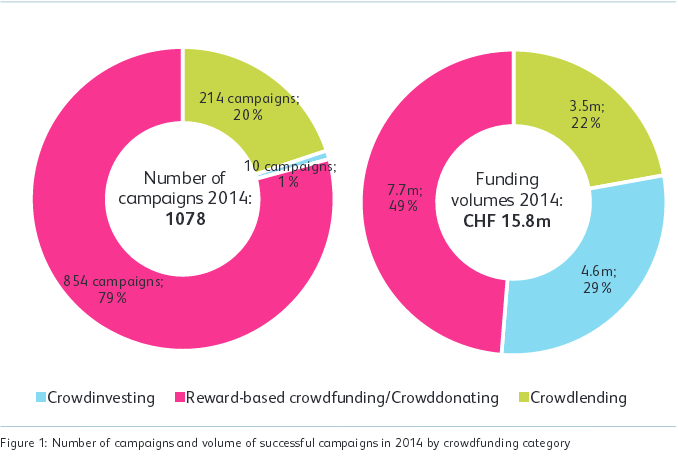

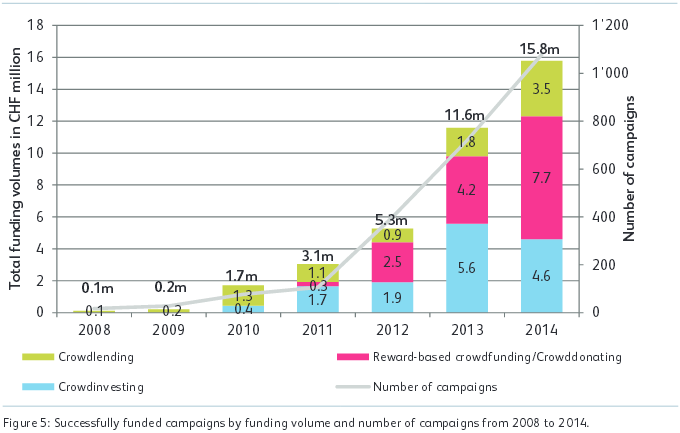

The Swiss market is growing fast; albeit on low absolute numbers compared to other European countries. The market is in a very early development stage. As the following chart shows the volume is mainly generated by crowdsupporting/crowddonating.

Source: Crowdfunding Monitoring Switzerland 2015 study

The total market for new loans to consumers in Switzerland in 2014 was 3.9 billion CHF. Via p2p lending 3.5 million CHF were originated in 2014, so that equals a market share of only 0.1%. But the p2p lending volume has nearly doubled compared to 2013 (1.8 million CHF). The authors state:

The crowdlending market has experienced the strongest year-on-year growth of all crowdfunding segments. … The number of campaigns rose from 116 to 214, and all of them were successfully funded. The current challenge of crowdlending platforms is not finding funders. On the contrary, it is (more) difficult to get borrowers on the platforms. Crowdlending campaign funders invested an average of CHF 1,100, which is substantially different from the figures in reward-based crowdfunding & crowddonating as well as in crowdinvesting. The average campaign amount was CHF 16,200, which was slightly higher than in the past year (CHF 15,000). The average loan amount in crowdlending is very similar to the average consumer loan as of the end of 2014. The crowdlending market is, however, still niche market.

Source: Crowdfunding Monitoring Switzerland 2015 study

Regulation limits that a private consumer loan cannot be financed by more than 20 different individual lenders.

The authors analysed loan data of the Cashare marketplace. Examining who uses p2p lending as a borrower the study finds:

The average borrower age is 38. One fifth had at least one child under the age of 16 at the time the loan was raised. At 37 percent, married people were proportionally under-represented, although they make up 54 percent of the permanent resident population. 19 Homeowners (19 percent) and women (24 percent) are also under-represented. The distribution of nationalities is slightly more representative of the Swiss population. 71 percent of the borrowers were Swiss, while 29 percent of the borrowers were not in possession of a Swiss passport. The average proportion of the foreign-born resident population in Switzerland was 22 percent between 2008 and 2013. The age distribution of the borrowers leads to the conclusion that crowdlending is currently still primarily used by the tech-savvy Generation Y. 60 percent of all loans raised since 2008 went to people under the age of 40. Only 4 percent of the borrowers for successful projects were over 60 years of age.

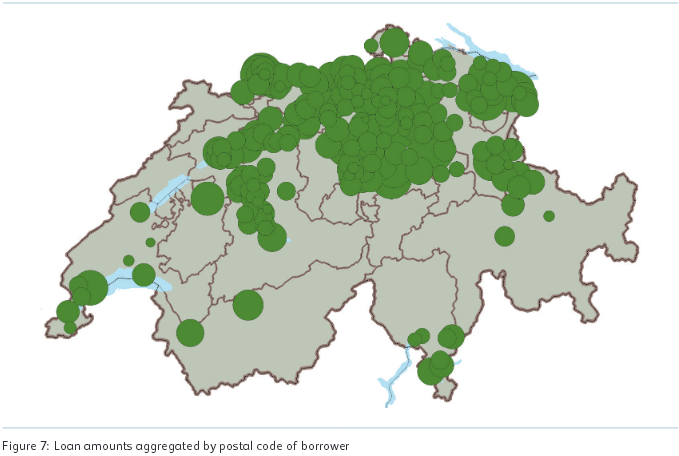

Also the borrowers regional distribution shows that use is much more common in the German speaking areas of Switzerland.

Source: Crowdfunding Monitoring Switzerland 2015 study

In Switzerland P2P Lending Service Cashare announced that it plans to be one of the web service pioneering the use of SuisseID a digital signature. Documents signed with this digital signature are as binding as a conventional signature on paper.

Opportunities for P2P Lending

Several European countries (e.g. Italy, Spain, Germany, Belgium) have enacted laws that equate digital signatures with conventional signatures.

P2P Lending can use digital signatures to

validate the identity (and depending on the signature card the address) of users

automate processes that otherwise would require a signature on paper and enable paperless process chains.

One of the biggest challenges for a new internet startup to offer an innovative financial service is to gain the trust of its potential customers. Consumers approach new concepts with legitimate caution.

The book ‘P2P Kredite – Marktplätze für Privatkredite im Internet‘ examines how p2p lending services can address the uncertainties and what measures can be used to build trust. After a short introduction of how p2p lending works and a look at Cashare, Smava, Zopa and Prosper the author covers the aspects credibility, safety, reputation, guarantee, sanctions, information and communication. Fabian Blaesi also describes how community features can help.

In an empirical study the importance of several factors for the perception and acceptance of p2p lending services by lenders is quantified.

Swiss Cashare.ch recently launched as the first p2p lending platform in Switzerland. The company, owned by Michael Borter (link to German language interview) and Roger Mueller has partnered with the collection agency C&S Credit Management AG, which handles all monetary transactions. Interest rates and loan durations are set by borrowers and lenders bid in a 14 day auction (minimum bid amount is 500 CHF which is approx 500 US$). If the loan is fully funded further bids in the remaining auction period will cause the interest rate to drop in 0.1 percentage steps, while old bids are outbid.

The fee schredule includes:

For lenders and borrowers: 5 CHF fee for identification process

For borrowers: 19 CHF listing fee

For borrowers: 0.75% of the loan amount per year servicing fee

For lenders: 0.75% of the loaned amount per year servicing fee

This results in borrowers having to pay even if their loan does not fund.

An unusual point in the process is that lenders have to sign a written contract for each successful bid and send it via postal mail to Cashare. That seems a bit uncomfortable to handle.

As Cashare launched only recently there currently are only 4 active loan listings.

If you have used Cashare as a borrower or lender, please share you experiences in the forum. Thank you.