The following table lists the loan originations for August. August was a slow month for many of the listed services probably due to the holiday season. Zopa crossed 1 billion GBP lent since inception (see infographic) and Giles Andrews stated he expects the next billion to be lent in 2016. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in August 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

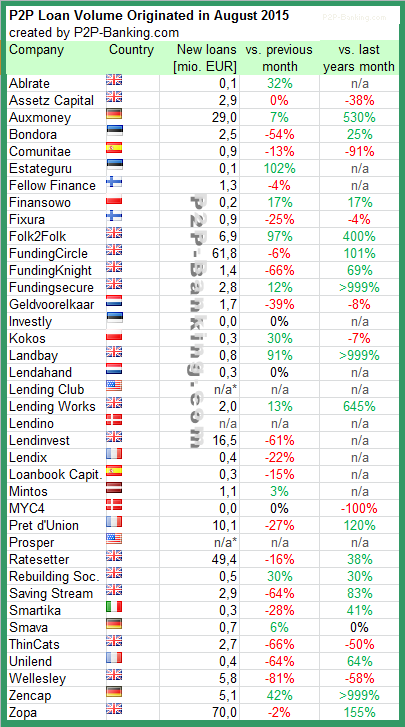

The following table lists the loan originations for July. Zopa originated 52M GBP and takes the lead for that month in Europe. Prosper reached 4 billion US$ in loan origination since inception. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in July 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

UK platform Seedrs has raised a 10 million GBP series A round led by Woodford Patient Capital Trust plc and Augmentum Capital. The capital raised will be used to launch Seedrs in the US market.

Furthermore, Seedrs is to launch a 2.5 million GBP crowd funding campaign to give existing shareholders and new investors the opportunity to participate in the round. The details will be announced later.

Seedrs plans to expand its marketing efforts in the UK and Europe, increase platform development activities and launch its business in the United States.

Today Lending Club announced that it opens to investors from Texas and Arizona. Lending Club is now open to retail investors from 30 US states.

“We are delighted to announce the addition of two key states today, which we believe will help drive more individual investors to our platform,” said Lending Club CEO Renaud Laplanche. “Our marketplace gives investors unprecedented access to consumer credit as an asset class, and empowers investors to diversify their investment across hundreds or thousands of loans. We are thrilled to be able to bring this access to investors in Texas and Arizona and appreciate the work done by the state regulators that allowed this to happen.”

When German p2p lending startup Finmar tried to register their logo as a trademark they were in for a negative surprise. The trademark office in 2014 forwarded them a 500 page objection filed by the FINRA (Financial Industry Regulatory Authority) which complained that the design of Finmar’s logo to closely resembled FINRA’s logo which was already protected by a European trademark filed in Madrid. Given the similarity of name and logo FINRA feared that there is a risk that both are confused.

Finmar was flabbergasted but tried to reduce the damage. They negotiated with FINRA that Finmar would change its logo but could keep its name. Finmar designed a new logo (see above), revoked the old trademark application, submitted a new one and exchanged the logo on the website and in all social media channels. In total this dispute took Finmar more than 15 months to settle.

When was the last time you stood in a long line outside your bank branch, patiently waiting to deposit money into your savings account? Imagining a scene like that seems ridiculous at a time with near-zero interest rates in an increasingly large number of developed countries.

But there where you would least expect it, in the Fintech world of fast-moving bits, some startups actually are imposing measures to throttle influx of investor money in order to balance it with borrower demand. Welcome to p2p lending (short for peer-to-peer lending). The sector is experiencing tremendous growth rates. With attractive yields for investors some platforms struggle to acquire new borrowers fast enough for loan demand to match the ever-rising available investor demand.

One challenging factor is deeply ingrained in the business model of p2p lending marketplaces: once a new investor is onboarded and found the product satisfactory, he is most likely to stay a customer for years to come and reinvest repayments received and maybe the interest also. On the other hand the majority of borrowers are one-time customers. They take out a loan typically just once. While it may take years for the borrower to repay that loan, in most instances there is no repeat business for the marketplaces. So the marketplaces have to constantly fire on all marketing cylinders to win new borrowers in order to keep up and grow loan origination volume.

This has sparked some outside of the box thinking, e.g. the partnership of Ratesetter with CommuterClub to win their loan volume, which is in fact mostly repeat business.

Winning investors has been relatively easy for many of the p2p lending services in the recent past. Investors are attracted typically through press articles or word of mouth. One UK CEO told me he never spent a marketing penny ever to acquire investors.

But what happens on the marketplace, when there are so many investors waiting to invest their money in loans, but loans are in short supply?

If the marketplace does nothing or little to steer it, then those investors that react the fastest, when new loans are available, will be able to bid and invest their money. This is the situation e.g. on Prosper, Lending Club and Saving Stream.

The marketplace has some kind of queuing mechanism. This is typically coupled with an auto-bid functionality. Examples of this are Zopa, Ratesetter and Bondora.

The investors are competing during an auction period by underbidding each other through lower interest rates. Examples of p2p lending services with this model are Funding Circle, Rebuilding Society and Investly.

The marketplace can lower overall interest rates to attract more borrowers while the resulting lower yields slow investor money influx.

The UK p2p lending sector is eagerly awaiting the sector to become eligible for the new ISA wrapper. Inclusion into the popular tax-efficient wrapper will attract an avalanche of new investor money to the platforms.

“That’s going to be a challenge for the industry,†said Giles Andrews, CEO of Zopa. “Once the dates are worked out, the industry will need to plan for that together, and we may have to do something we have never done before, which is to limit the supply of money. It’s not good to have people’s money lying around [awaiting new borrowers] or to lower standards of borrowers.â€[1]

So there is some speculation that UK p2p lending services could impose temporary limits on new investments.

The investor viewpoint

The aim of the investor is to lend the deposited money easy and speedy into those loans that match his selected criteria/risk appetite. Idle cash earns no interest and will impact yields achieved (aka cash drag).

For the retail investor none of the above mentioned mechanisms are ideal. The “fastest bidder wins†scenario means he would either have to sit in front of the computer most of the time or be lucky to be logged in just as new loans arrive. The queuing mechanisms are disliked as they can prove to be very slow in lending out the funds and can be perceived as nontransparent (see the lengthy and numerous forum discussions on the Zopa queuing mechanism). Underbidding in auctions does provide the chance to lend fast, but at the risk of setting the interest rate too low and this requires a strategy and can also be time consuming.Continue reading →