3rd party service LendingRobot today announces a partnership with Funding Circle in the United States, expanding the reach of LendingRobot’s automated investment technology beyond consumer loans and into small business lending.

Through the integration, individual investors using LendingRobot can set automated investment strategies for Funding Circle’s marketplace based on an extensive set of loan filtering criteria, and leverage the unified platform to manage their investments across multiple marketplaces, including Funding Circle.

“Introducing Funding Circle to the LendingRobot family of platforms demonstrates that our algorithmic investment strategies are extensible beyond consumer credit,†said LendingRobot CEO Emmanuel Marot. “The growth of peer lending as an investment vehicle is naturally encouraging an increase in the number and size of focused, vertical marketplaces. What we are building with this partnership is a unified view of all the major aspects of peer lending for investors, …â€. Continue reading →

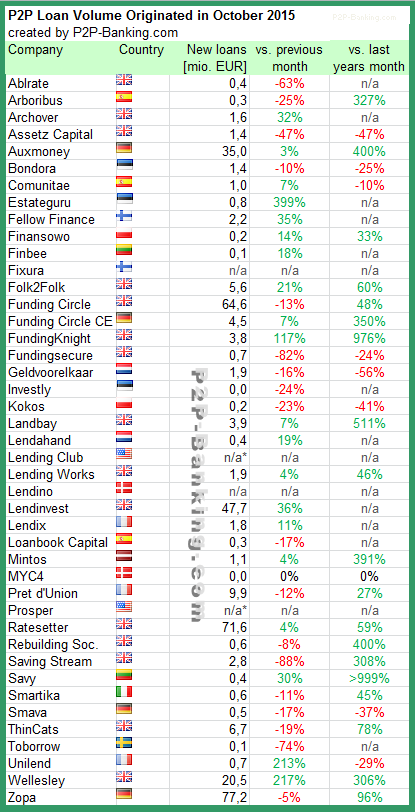

The following table lists the loan originations for October. Zopa is again leading by new volume followed by Ratesetter and Funding Circle. I added 1 new platform to the table. I do monitor development of p2p lending statistics for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in October 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Lending Club reported the results for the 3rd quarter today.

Financial Highlights are:

Originations – Loan originations in the third quarter of 2015 were $2.24 billion, compared to $1.17 billion in the same period last year, an increase of 92% year-over-year. The Lending Club platform has now facilitated loans totaling over $13.4 billion since inception.

Operating Revenue – Operating revenue in the third quarter of 2015 was $115.1 million, compared to $56.5 million in the same period last year, an increase of 104% year-over-year. Operating revenue as a percent of originations, or revenue yield, was 5.15% in the third quarter, up from 4.85% in the prior year.

Adjusted EBITDA – Adjusted EBITDA was $21.2 million in the third quarter of 2015, compared to $7.5 million in the same period last year. As a percent of operating revenue, Adjusted EBITDA margin increased to 18.4% in the third quarter of 2015, up from 13.3% in the prior year.

Net Income – GAAP net income was $1.0 million for the third quarter of 2015, compared to a net loss of $7.4 million in the same period last year. GAAP net income included $13.5 million of stock-based compensation expense during the third quarter of 2015, compared to $10.5 million in the prior year.

Earnings Per Share (EPS)– Basic and diluted earnings per share was $0.00 for the third quarter, compared to basic and diluted EPS of ($0.12) in the same period last year.

Adjusted EPS – Adjusted EPS was $0.04 for the third quarter of 2015, compared to $0.02 in the same period last year.

Cash, Cash Equivalents and Securities Available for Sale – As of September 30, 2015, cash, cash equivalents and securities available for sale totaled $918 million, with no outstanding debt.

“We had another spectacular quarter, with revenue growth re-accelerating from 98% to 104%, and EBITDA jumping 181% year-over-year to reach 18.4% margin ,” said Lending Club founder and CEO Renaud Laplanche. “With over 1.2 million customers, continuously high customer satisfaction, strong credit performance, increased marketing efficiency and lower customer acquisition costs, we are continuing to observe tremendous network effects and benefits of scale. Our results this quarter combined with our raised Q4 outlook lead us to forecast a near doubling of revenue again this year and look toward 2016 with high confidence.”

Lending Club opened to retail investors in nine new states, bringing investor base, which is very sticky, to over 100,000. Small business loans grew in line with expectations.

Traditional banks do not benefit from network effects. Lending Club on the other hand does benefit strongly from network effects. All these dynamics lead to lower acquisition costs and higher margins.

From the Q&A of the earning call:

Decrease in returns (approx 1%) is due to network effects allowing Lending Club to pass some benefits in form of lower interest rates to borrowers. This is also enabled by high investor demand.

Custom loans are stable quarter of quarter. Lending Club has not transferred loans to the standard product.

Customer acquisition costs have not risen as Lending Club has invested early into the product and now benefits from it, e.g. through good customer ratings driving traffic

On the question if there is an increase on fraud attempts, Lending Club responded that there was no increase in attempts or frauds committed. Laplanche is not surprised that new platforms might experience a rise of attempts.

Does Santander exiting consumer loans have any impact on the relationship between LC and Santander? Santander was a great partner and accounted for a single digit percentage of volume. Lending Club has replaced Santander with other institutional lenders. The very diverse investor base of Lending Club is seen by Laplanche as a competitive advantage over newer platforms.

Madden has no direct impact on the investor base of Lending Club.

Are whole loans growing faster than originations? The mix is a function of the mix and appetite of the investors behind it.

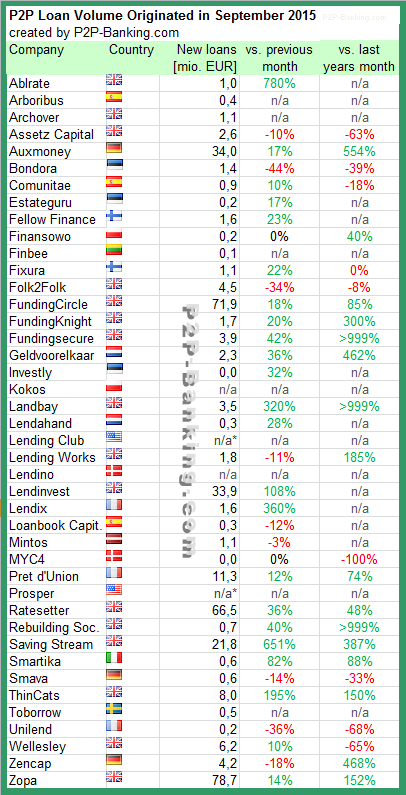

The following table lists the loan originations for September. Most marketplaces grew their loan volume compared to the previous month. Saving Stream had an exceptional month, with several very large loans. I added 4 new services to the table. I do monitor development of p2p lending statistics for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in September 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

GROUNDFLOOR is taking private real estate lending public. We’re paving the way to open a new $70 billion lending market to all – and that’s in single family home renovation and construction lending alone. You can read more about how we’re doing that here.

More broadly, we like to think of the company as an exposition on a theory of capital markets. We believe the broadest base of capital wins—because it’s faster, cheaper, more flexible and more efficient.

What are the three main advantages for investors?

GROUNDFLOOR makes real estate investing more accessible than ever before. We create new investment opportunities for non-accredited investors; a group of Americans that have never had access to these types of investments before.

Our typical loan term is dramatically shorter than what you see with P2P lending products like Lending Club. Our average term is 6 or 12 months, compared to 3-5 years for typical deals elsewhere.

We offer dramatically higher returns than traditional investments. During our one-year pilot in Georgia, the average annualized yield for our investors was over 12 percent. For context, that means that GROUNDFLOOR outperformed the compound average annual return of Charles Schwab’s mutual funds between 1970 and 2014.

What are the three main advantages for borrowers?

It’s fast and simple to get funded on GROUNDFLOOR. You can submit a project by checking your rate in less than 5 minutes. Projects have 30 days to fund, but most projects fund much sooner once they are posted. The closing process is quick and painless using the same closing attorneys you already use.

GROUNDFLOOR is a reliable source of capital. We fund construction, renovation and other loan types that are typically difficult to bank finance, and we offer low fixed interest rates starting at 6% (not including fees).

We offer terms that fit borrower needs. Most of our loans run from 6 to 12 months. Borrowers can repay their loan at any time to reduce borrowing costs, and personal guarantee and cross-collateralization is not required in most circumstances.

What ROI can investors expect?

GROUNDFLOOR backs independent builders with secured loans that pay 5-26% annually. During our one-year pilot in Georgia, the average annualized yield for our investors was over 12 percent.

What is the background of Groundfloor? Who are your seed investors?

GROUNDFLOOR was founded in February 2013 and is based in Atlanta. We have raised $2.5 million in seed funding from angel investors including Michael D. Olander Jr, Bruce Boehm, Tibor Nagygyorgy, Mark Easley Sr. and Inception Micro-Angel Fund.

Brian Dally is co-founder and CEO. He has spent his career building disruptive technology startups during stints in Silicon Valley, Boston, London and the North Carolina Triangle region. Previously, he led the launch of Republic Wireless to take on the big four cellphone carriers to international acclaim.

Nick Bhargava is co-founder and EVP of regulatory affairs. An expert in securities law, Nick was heavily involved in the JOBS Act as an early pioneer who advanced the concept of equity crowdfunding. Nick and Brian met through Groundwork Labs in the Triangle-area startup hub the American Underground. His years in finance have included work for the Financial Services Roundtable, SEC, FINRA, TD Waterhouse and RBC Financial Group. Continue reading →

The small businesses who already use H&R Block for bookkeeping, payroll, taxes and other accounting services now have access to a new online service: business loans up to 500,000 US$, thanks to a new referral partnership with Funding Circle, a p2p lending marketplace for small business loans.

Through the partnership, Funding Circle loans are the preferred solution for H&R Block Small Business customers seeking financing to grow.

The new agreement bolsters Funding Circle’s diverse strategic partner ecosystem, which has experienced a 313% growth in monthly originations since January 2015. Other key partners integrated onto the platform recently include Intuit, Tri-Net, LendingTree, Credit Karma, Creditera and the National Small Business Association.

“Funding Circle offers strategic partners across multiple verticals the opportunity to build value-added services by leveraging our core technology, strong underwriting and customer-first approach to deliver unique financing solutions for their small business customers,” said Funding Circle co-founder and US managing director Sam Hodges. “Building a rich and diverse partner ecosystem is a core part of our growth strategy, and we are proud to welcome strong brands like H&R Block onto our platform who share our values and mission to help small businesses grow and prosper.”

“The mission of our two organizations are very similar,” said Jeremy Smith, director of Block Small Business. “We both provide services to small businesses that enable successful, sustainable growth. Given that we do the accounting for service businesses with less than $20MM in revenue, our clients have found it difficult to get loans from traditional banks. Well, Funding Circle specializes in lending to these types of businesses; so now our clients have a go-to source for capital to grow their businesses.” Continue reading →