Matt Flannery of Kiva.org describes in a blog post which obstacles Kiva has to overcome to make accounting not a too time consuming task for the local fireld partners (MFIs). With some MFIs having over thousand loans and slow internet connection Kiva needed to find a solution that saved time.

About a year ago, we realized that many of our Field Partners were having trouble doing so. The sheer number of page loads was making it prohibitively difficult for a Field Partner to register repayments on time, even when the actual borrower collections in the field were happening like clockwork. Thus, we introduced "exception-based" repayments. The idea, used widely in MFI accounting systems already, is to have regularly scheduled payment registered automatically in a system unless the loan officer marks an exception — an event signaling that something went wrong and the borrower did not pay the full amount. Since borrowers typically repay 95% (or so) of the time, loan officers only need to register something 5% of the time.

Kiva's first whack at exception based payments was very crude. The feature was written by me in late '06 in between blog entries and trying to keep the site up. Many of our Field Partners adopted the feature out of necessity and it saved them a lot of time. However, it was very difficult to mark an exception, so most of them never did. Thus, many of our Field Partners never mark exceptions and just repay all of their loans on time, even in the 5% case where the borrower defaults. This creates misleadingly high repayment stats on the site and we are working to correct that.

Kiva plans to have group loans. The post does not describe in detail, how group loans will work, but I am looking forward to examine this feature:

In addition to that, we are rolling out a number of features to further reduce the work required by our Field Partners and increase transparency. Group Loans will go live on the site this week. This will allow Field Partners to post up groups of up to 50 on the site as an individual loan application on the site. Group-lending is common practice in microfinance, but was not well supported by Kiva until now.

Also Kiva will change how currency exchange risks are handled:

we will be introducing local currency support for all of our Field Partners. This will allow the disbursement and repayment amounts on the site more closely mirror the actual accounting books of each MFI. This creates more transparency around financial flows. It also paves the way for a future reality where our partners will not need to bear currency risk. Hard currency lending has fallen out of favor in the microfinance world and we hope to soon be on the cutting edge of local currency lending.

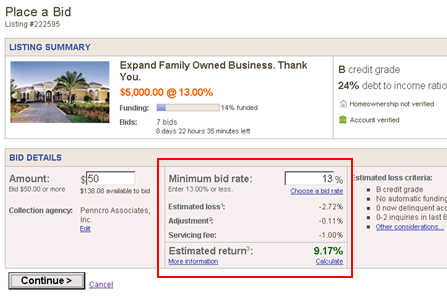

Note that on MyC4.com for most loans the borrower has to take the currency exchange risk. Loans with small amounts are paid out in local currency, while large loans are paid out in Euro.