CommuterClub is a promising startup currently running a pitch to raise their 2nd round from the crowd. I really like their business model and have invested in both rounds.

Interview with Petko Plachkov, CEO and Founder

What is Commuter Club about?

CommuterClub delivers a new and innovative way to access public transport as a subscription service.

By bringing together a low cost loan with the existing annual ticket, CommuterClub can deliver the savings of an annual, in a far more convenient and attractive package as a monthly payment plan.

Our goal is to continue to bring new innovative products for commuters, delivering value for money and ease of use.

I really like the fact that your business model builds on long customer relationships. What do you do to achieve high customer satisfaction?

CommuterClub operates in a sector dominated by large slow moving monopolies who manage public transportation. Our proposition is to offer an alternative approach to commuters that begins with their needs. Our focus on a simple customer journey, great customer service and a simple product all deliver a fantastic outcome for consumers.

This is key in ensuring high customer satisfaction and providing a real alternative to the existing ticketing options.

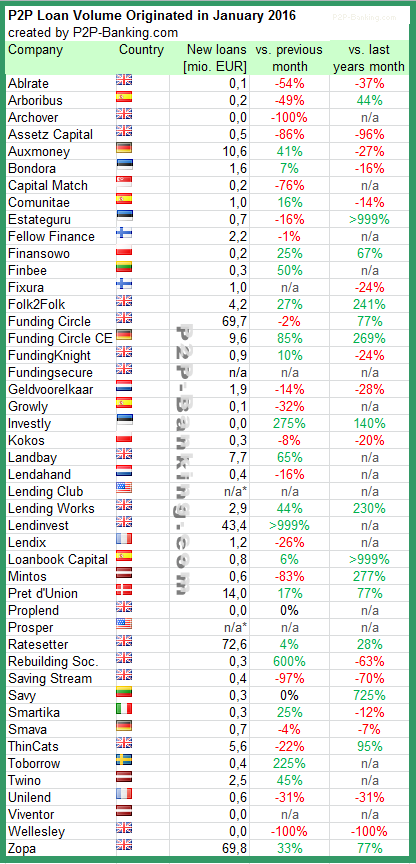

The audience of this blog is highly interested in p2p lending. Can you please explain how your company ties into this industry and what role Ratesetter and potentially Zopa play for your financing?

CommuterClub works with RateSetter to fund all loans. As a business P2P was the key building block enabling us to deliver a low cost and flexible product to consumers, something that we would have found exceedingly difficult if we worked with incumbent banks.

We expect to continue to work with p2p going forward and to maintain our close relationship with RateSetter.

The pitch video

The timing of this round is a bit of a surprise to me since you indicated to shareholders recently ‘at our current trajectory we expect to be [able to] sustain growth from retained earnings’. Why did you decide to raise further capital now?

CommuterClub has made tremendous progress in diversifying the business expanding nationally in the UK, launching a B2B solution and also looking to cover other verticals like parking.

This expansion of our product set has also expanded our target market and we are now raising capital to fund our continued expansion and growth.

Name one fact that makes your pitch a better investment than any other pitch on Seedrs.

Real, proven traction backed by millions in loans and thousands of happy customers.

P2P-Banking.com thanks Petko Plachkov for the interview.

This article is not an investment advice. Investing in startups bears significant risks, including total loss of investment.