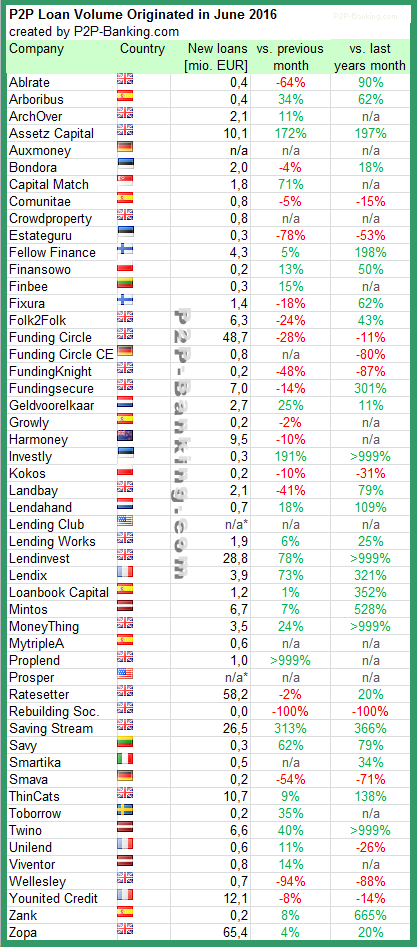

The following table lists the loan originations of p2p lending platforms in June. Zopa leads ahead of Ratesetter and Funding Circle. This month I added MytripleA. The total volume for the reported marketplaces adds up to 334 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Table: P2P Lending Volumes in June 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

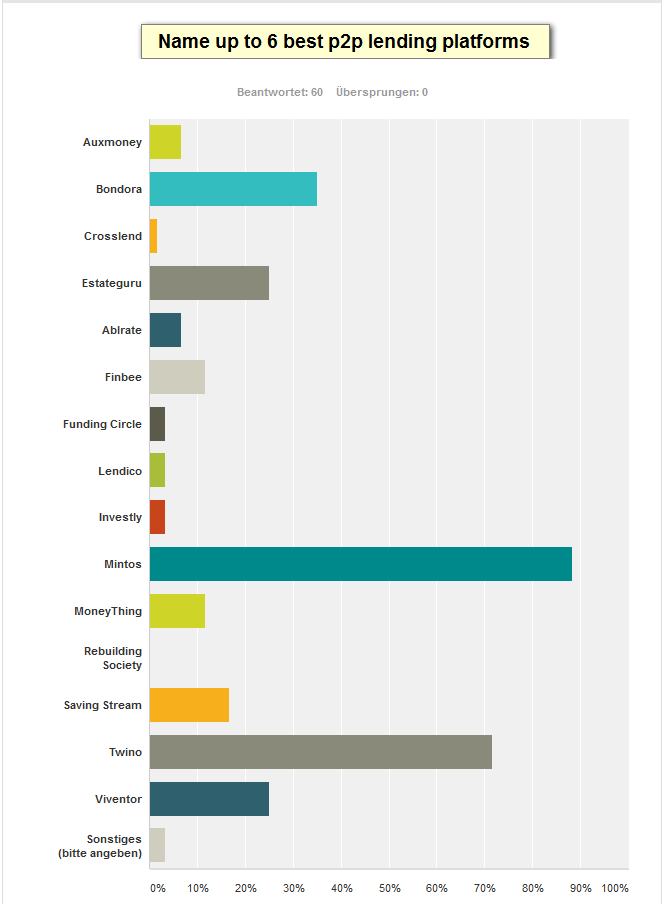

A poll conducted by P2P-Kredite.com among seasoned German speaking investors found, that many prefer p2p lending platforms outside the country they live in. After getting accustomed to the p2p lending concept and liking it, they are on a hunt for higher yields. Further supporting factors are the offered English language interface (a language most understand well), the easy transfer of funds within the Eurozone by SEPA payments and more features offered, e.g. most foreign platforms offer a secondary market, while currently none of the German marketplaces do.

Poll by P2P-Kredite.com, conducted in June 2016. 60 respondents. Each respondent could name up to 6 platforms. Note that Funding Circle refers to the German platform of Funding Circle, not Funding Circle UK.

Mintos (53 votes) and Twino (43 votes) lead by a wide margin in preference of the respondents, followed then by Bondora (21), Estateguru (15), Viventor (15), Saving Stream (10), Moneything (7) and Finbee (7). Exclusively baltic and british platforms rank best among the respondents. The choice of british platforms for German investors is limited though as some like Zopa or Ratesetter are open only to UK residents or require a UK bank account to sign up. Nearly all votes were cast before the Brexit decision. It remains to be seen how the UK platforms will rank in German investor preference in the future, given the more volatile GBP/EUR rates and the increased uncertainty for the UK economy.

Well that was a surprise. When I went to bed last midnight the news reported more indications for a remain vote than for a leave. Even with psephologists cautioning that the referendum is very hard to predict due to the lack of comparision data from earlier votes, it seemed to me that the outcome was likely pro EU.

While I had personally wished the Brits to stay in the Union they took a democratic decision and now the politicans have to act upon it to execute divorce.

Awakening to the new reality I now have to assess what this means for my personal p2p investment strategy – as a foreign investor. Only a small portion of my p2p investment portfolio is invested in UK platforms (a substantial amount at Saving Stream, small amounts with Ablrate, MoneyThing and Rebuilding Society). The markets are in turmoil, and I have already taken the hit by the pound dropping sharply compared to the Euro this night.

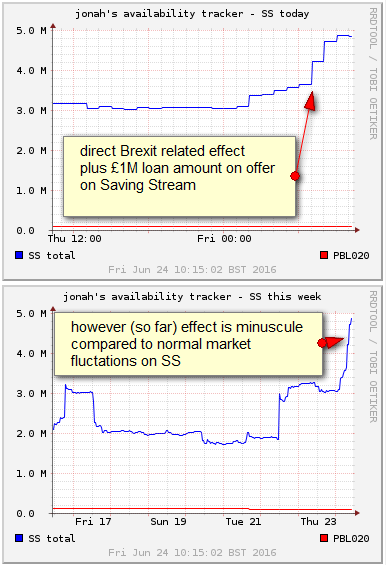

Another effect is that the uncertainty is causing more investors to put up loan parts for sale – the effect is measureable on Saving Stream and currently accounts for a plus of approx. 1M GBP loans on offer there. Still this amount is very small compared to fluctations of liquidity levels due to other factors. For most loans this now means that there is a considerable delay in selling loans, due to queue size. However this could be cleared up quickly by one or two large loans repaying and the interest payout on July 1st.

(Source: jonah; own edits)

With Saving Stream and Moneything loans will depend highly on the development of the property prices. Some expect a drop in property prices. I think it is to early to tell if that will happen, but I think it is very likely that there will be slow down in new development activity while everbody waits to see what the outcome will be. This will affect the demand for bridging loans and thereby Saving Stream and Moneything to a cetain degree.

And then totally unpredictable there is the question how this new direction will effect the European economy as a whole and whether it might trigger a recession. While I am optimistic that it will not, there is an extreme amount of uncertainty and I have to consider that this might impact my p2p investments on continental European platforms.

For now I have decided that I will not deposit new funds on UK platforms (which I was planning to do) but will not withdraw funds either at the moment and will just keep reinvesting the proceeds. I see little point in selling off loans (would be hard right now anyhow as liquidity seems to dry off temporarily), and exchange the amounts back to Euro. That would guard me from further drops of the pound exchange rate, but I think it is not sure that the pound will fall into a continuing decline (even so that seems more likely than any rise in the pound rate vs the Euro).

For the continental platforms my strategy remains unchanged by the event, even though I think that the risks on some platforms have risen somewhat too in the mid-term outlook.

The following table lists the loan originations of p2p lending marketplaces in May. Funding Circle leads ahead of Zopa and Ratesetter. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Table: P2P Lending Volumes in May 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

P2P lending platform Zopa will finance loans for customers of newly launched online mobiler retailer Unshackled.

Customers can fund the purchase of handsets by taking out a finance deal with Zopa. The APRs on launch will range from 9.7 per cent to 24.9 per cent. Customers will also be able to pay off early at no extra cost or make additional payments.

The partnership is Zopa’s first online retail agreement, with its service integrated in to Unshackled.com sales platform using the Zopa API.

Jaidev Janardana, Zopa CEO added: ‘With the majority of consumers getting a bad deal on their mobile phone, partnering with Unshackled means we can offer consumers better, fairer and more transparent deal in financing their phone.’

Today UK p2p lending service Zopa announced it will extend its product range to offer ‘Zopa Car ReFi‘, a refinancing product for car loans. It is positioned to allow consumers to refinance existing car loans at a better rate. Zopa’s credit risk algorithms, combined with in-depth vehicle information, act together to provide customers with a free and instant personalised savings estimate, prior to those customers taking out the product.

Ownership of the vehicle remains with Zopa’s Lenders until the final payment, when it will be transferred to the borrower.

Jaidev Janardana, Zopa CEO said, ‘We are thrilled to launch the UK’s first seamless car refinancing service, helping thousands of consumers drive down the cost of car ownership. This is a market worth £12bn per year with plenty of space for customer-first innovation – something we have specialised in at Zopa for over 11 years. Buying a car is by far the most common reason for a customer to take a personal loan from Zopa, so we are proud to now also offer a product that can help customers that already have a car on a finance agreement. …’