Lending Works CEO Matthew Powells reported an influx of more than 500K GBP deposits within 3 hours after launching the Lending Works Innovative Finance ISA (IFISA). Lending Works’ IFISA product offers 4% (up to 3 years) or 4.7% (up to 5 years term) tax-free for investments on the p2p lending marketplace. However Lending Works, anticipating the huge demand, has launched the offer with an upper ceiling: ‘We’re anticipating a significant spike in lending volumes as a result of the new ISA. Because we want to match your money swiftly at all times, we will only be accepting ISA monies from lenders in fixed, periodic tranches totalling £1 million at a time. Once this limit is reached, we will then temporarily be closing this window of opportunity until further notice.’ as stated on the company website. It is expected that Lending Works might lower rates after this threshold is met.

Investors can draw down either interest, or interest and capital over the term of the loan, or reinvest the interest. A recent survey of Lending Works’ existing investors found that 88% plan to open an IFISA, with around a third expecting to invest between 10,000 GBP and the maximum threshold of 15,240 GBP of their annual ISA allowance into the IFISA before the end of the tax year in April. In the next tax year the allowance will rise to 20,000 GBP. Continue reading →

The following table lists the loan originations of p2p lending marketplaces in January. Funding Circle leads ahead of Zopa and Ratesetter. The total volume for the reported marketplaces adds up to 476 million Euro. I track the development of p2p lending volumes for many countries. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Zopa celebrated passing 2 billion pounds in loans lent since launch. That figure means 300,000 loans to 246,000 borrowers funded by around 75,000 lenders. Jaidev Janardana, Zopa’s CEO, commented: “We’re excited to be the first UK peer-to-peer lender to pass the 2 billion GBP milestone. Over the last 12 years, we’re proud to say we’ve helped a third of a million people get better interest rates for both borrowing and lending. The 2 billion GBP milestone demonstrates how far we have come, but our journey is only just getting started. Our decision to launch a next generation bank reflects our mission to create better options for consumers and to shape the future of finance.â€

Further milestones reached this month were:

Harmoney passes 500 million NZD since inception

Assetz Capital passes 200 million GBP since inception

Table: P2P Lending Volumes in January 2017. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Funding Circle raised 100 million US$ of equity capital in a round led by Accel Partners. The round also included other existing investors Baillie Gifford, DST Global, Index Ventures, Ribbit Capital, Rocket Internet, Sands Capital Ventures, Temasek and Union Square Ventures.

The company will use the funding to continue to consolidate its position, as well as to continue to invest in technology and talent.

Measured by new origination volume during the last months Funding Circle is the largest p2p lending marketplace in the UK. The company is also present in the US and in continental Europe. Last week the British Business Bank committed to lend 40 million GBP to British SMEs through Funding Circle.

Funding Circle has now raised 373 million US$ in equity capital. The previous round was a 150M US$ in 2015 round led by DST Capital.

For decades buying houses, refurbishing them and selling them at a higher price and moving on to the next property seemed like a popular sport to Brits. Many of them see properties as investments and with house prices mostly moving up lots of them aimed to finance a property while they were young and then build a portfolio. With limited supply of new land with planning permissions this strategy worked well most of the times in the past, except when the market overheated and a real estate bubble popped.

There are downsides to this do-it-yourself approach:

Concentration of risk in one or few properties: if they underperperformed for what ever reason, the yield was sub-average

A lot of money, time and work required. The investor had to do everything itself as a landlord

Selection of new properties usually limited to a small region the investor lives in

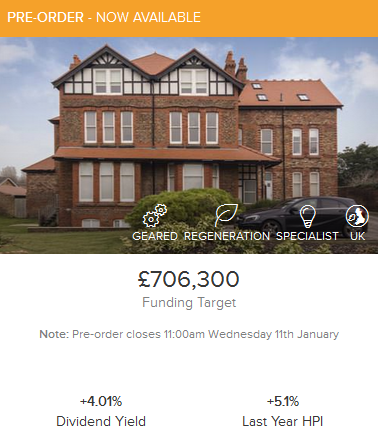

British platform Property Partner allows everyone to invest in British properties from a minimum of 50 GBP. Investors select a listing, invest into a SPV (special purpose vehicle company) that pools the investment in the property. The SPV collects rental income and pays dividends to investors monthly. A useful table of the past achieved rental income can be seen here. In the green marked cases the actual rents are higher than the original forecsts. Potentially investors can also gain, if the value of the property rises.

The time span of an investment is 5 years, however investors can try to sell their parts on the secondary market, which allows discounts and premiums any time.

The platform allows the investor to diversify across multiple properties easily. The fee is 2% for investment (in new listings or buying through the secondary market). For management, advertising and letting Property Partner charges 12.6% of gross rent.

So far Property Partner has funded 311 properties for 43.9 million GBP with 9.100 investors participating.

For new listing there is a pre-order period, where bids are collected. If the listing is oversubscribed then each investor is allocated a lower proportionate amount of shares.

Each listing contains an investment case desctiption, property details, a floor plan, financials, a solicitor’s report and a surveyor’s report as well as the house price index (HPI) information for the area.

For the secondary market there is a ‘data view’ section which lists key indicators for the parts listed for sale.

Investors that do not want to pick listings can set up the auto-invest option which will automatically invest an amount the investor sets each month in 5 properties.

Investing from abroad

Property Partner allows foreigners (except for US residents) and corporations to invest. If you do not live in the UK but see the UK housing market as an investment opportunity Property Partner is a hassle free possibility to invest in british real estate. Non resident investors should consider using Transferwise or Currencyfair to avoid high bank fees and get a better currency exchange rate.

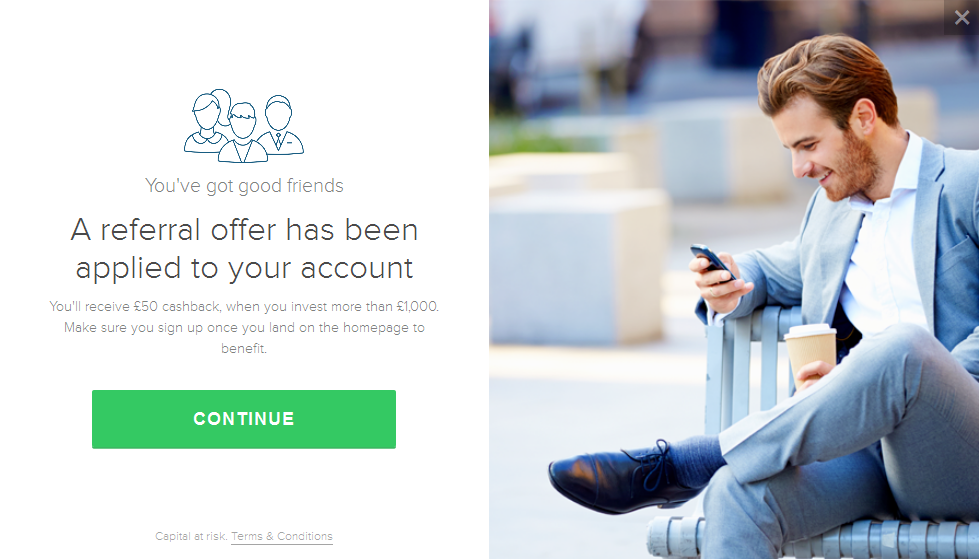

How to get 50 GBP cashback at sign-up

To get 50 GBP referral cashback, when you invest more than 1000 GBP sign up now via this link . To see available promotions by other platforms visit our cashback offer page.

Property Partner cashback confirmation at sign-up. To see it follow this link and sign up.

The following table lists the loan originations of p2p lending marketplaces in December. Funding Circle leads ahead of Ratesetter and Zopa. Lendix reports an all time record month. Saving Stream and Assetz Capital had a good month, too. Mintos crossed the milestone of 100 million EUR originated since inception. The total volume for the reported marketplaces adds up to 414 million Euro. I track the development of p2p lending volumes for many countries. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Table: P2P Lending Volumes in December 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

In August the FCA posted a call for input preceeding a planned review of the current regulation of p2p lending and crowdfunding for equity. Today the FCA publishes interim feedback. The feedback statement provides a first response to the feedback received and sets out next steps.

Based on a review of the feedback received, issues seen during the supervision of crowdfunding platforms currently trading and consideration of applications from firms seeking full authorisation, the FCA believes it is appropriate to modify a number of rules for the market.

Initial findings

Loan-based and investment-based crowdfunding

For both loan-based and investment-based crowdfunding platforms the FCA has found that, for example:

it is difficult for investors to compare platforms with each other or to compare crowdfunding with other asset classes due to complex and often unclear product offerings

it is difficult for investors to assess the risks and returns of investing on a platform

financial promotions do not always meet our requirement to be ‘clear, fair and not misleading’ and

the complex structures of some firms introduce operational risks and/or conflicts of interest that are not being managed sufficiently

Loan-based crowdfunding

In the loan-based crowdfunding market in particular the FCA is concerned that, for example:

certain features, such as some of the provision funds used by platforms, introduce risks to investors that are not adequately disclosed and may not be sufficiently understood by investors

the plans some firms have for wind-down in the event of their failure are inadequate to successfully run-off loan books to maturity

the FCA has challenged some firms to improve their client money handling standards

Proposals for new rules to be considered in Q1 2017

The FCA plans to consult on additional rules in a number of areas. These include more prescriptive requirements on the content and timing of disclosures by both loan-based and investment-based crowdfunding platforms.

For loan-based crowdfunding the FCA also intends to consult on:

strengthening rules on wind-down plans

additional requirements or restrictions on cross-platform investment

extending mortgage-lending standards to loan-based platforms

The FCA’s current rules on loan-based and investment-based crowdfunding platforms came into force in April 2014. They aimed to create a proportionate regulatory framework that provided adequate investor protection whilst allowing for innovation and growth in the market.

The call for input in July 2016 launched a post-implementation review of these rules. The paper summarised market developments since 2014 and some of the FCA’s emerging concerns.

Andrew Bailey, Chief Executive of the FCA, said:

“Our focus is ensuring that investor protections are appropriate for the risks in the crowdfunding sector while continuing to promote effective competition in the interests of consumers. Based on our findings to date, we believe it is necessary to strengthen investor protection in a number of areas. We plan to consult next year on new rules to address the issues we have identified.†Continue reading →