This p2p lending statistic contains the loan originations of p2p lending companies for last month. Funding Circle leads ahead of Zopa and Ratesetter. The total volume for the reported marketplaces adds up to 539 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending services.

Thincats reached the milestone of 250 million GBP loans originated since launch.

Table: P2P Lending Volumes in October 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Assetz Capital is now the UK’s second-largest peer-to-peer business and property lender and also the second largest in Europe. Since 2014, we have been providing competitive loans to credit-worthy SMEs and attractive returns to investors. We provide fairer and more accessible business lending to small and medium sized businesses and property developers throughout the UK.

Since our launch, we have lent more than 350 million GBP to credit worthy businesses whilst providing returns of 30m GBP to our investors using a number of automated investment accounts that earn gross rates of return between 3.75% – 7% per annum and also permitting manual lending at rates often above that. Almost all funding to date has come from retail investors and maintaining support for retail investment is one of our business aims.

What are the three main advantages for investors?

Firstly, we only lend to businesses who we assess as credit worthy businesses with tangible assets. Tangible security is taken for each and every loan – which is unusual for peer-to-peer lenders – in order to reduce the risk of capital losses for investors, while also lowering the cost of borrowing for businesses. We also deploy traditional credit assessment techniques rather than rely solely computer-based borrower assessments, meaning our processes are fast, meticulous and human. As a result of our processes, Assetz Capital’s expected loss rates are amongst the lowest in the industry (currently standing at just 0.35% across our live loan book).

Secondly, we cater for all types of investors. In the past four years, we have experienced strong annual growth year on year, and have attracted a wide set of sophisticated and consumer retail investors, as well as attracting family office and institutional investment. We believe it is because we have demonstrated excellent credit skills and loan performance, while delivering strong net yields.

Thirdly, we are also the only major UK P2P platform to still offer a manual investment option. This allows investors to choose exactly which borrowers to lend to, allowing them to cultivate a bespoke investment portfolio and choose appropriate levels of risk in their investments. For those wanting automated accounts, we offer a wide selection ranging from our Access Accounts to a Green Energy Account, all of which cater to those with less time to invest. This combination of accounts offers the type of control that an individual investor may require, allowing people to pick and choose from a wide range of individual loan opportunities, and also the ability to automatically lend if they are time-poor.

What are the three main advantages for borrowers?

Assetz Capital has been providing small and mid-sized businesses with flexible and quick access to funding for future business and employment growth with competitive rates.

Rather than being just a website with automated credit assessments, Assetz Capital is run by finance, banking, credit and lending professionals with huge industry experience, alongside our large UK-wide network of employed Regional Relationship Directors who visit potential borrowers and help structure the loans. I believe that this is unique to the P2P industry, and is reassuring to both business borrowers and lenders that behind the technology and website there are actual, qualified humans with relevant experience to help structure good quality transactions. Borrowers really appreciate the ability to structure their loan requirements face to face with experienced professionals instead of encountering the “computer-says-no†problem of today’s banking industry.

We’re also a lean business, and as such we have lower overheads than traditional lending institutions. Coupled with the fact that we only lend to credit worthy businesses holding tangible assets, this means our cost of borrowing for businesses is kept low.

With the uncertainty that has come with Brexit, we have found that our platform is overcoming some of the issues which many UK businesses are currently facing. We believe that fixed rate loans offer businesses a stable way to predict part of their finances, regardless of external market conditions. Brexit may put pressure on banks to reduce loan availability or raise rates substantially, but alternative finance providers such as Assetz Capital are continuing to offer fixed rate loans.

What ROI have investors made on average on the platform in the past?

As a business, we are totally transparent with our top-line numbers, and these are updated live in a prominent position on our website. In just over four years, investors on Assetz Capital have collectively earned gross returns of around 30 million GBP on their investments, relating to more than 350 million GBP in loans to date. We have a big announcement at the beginning of November that further endorses these results.

Assetz Capital has succeeded in growing loan originations sharply in the past 12 months. How did you achieve that and were intermediaries like brokers a major factor?

While much of our loan origination is organic, brokers have also played a vital role in referring many small and medium sized businesses to us. To date, more than 350 successfully funded projects have come through brokers, and we predict that this will grow to approaching 1,000 by the end of the 2018 year. In fact, this has been so successful, we are actively working to increase our broker network significantly in the next two years, and have recently revealed a strategy to further support brokers through a number of methods.

For example, our network of nationwide Regional Relationship Directors is supporting more brokers locally. We are also offering new product and pricing improvements to further build our relationships with brokers. Our face to face approach is very much liked by brokers and their borrowers alike and this is also a factor in our success, as is the experience of our team.

What will the soon to be launched Assetz Capital IFISA offer? Will it offer the same range of investments and interest rates as currently? Will the IFISA be flexible?

Now that we have achieved full authorisation from the UK regulator, the Financial Conduct Authority (FCA), we are preparing to launch our Innovative Finance ISA (IFISA), which should be ready by the end of 2017. While I can’t reveal all the details at time of writing, it will be highly flexible as it is an extension of our very successful model.  There is no intention to have any ISA fees for normal transactions and we also intend for our main lending investment accounts to also be available at the same rates in the ISA. We also intend to release our next generation investment dashboard that we believe will keep it at the forefront of the industry.

Will you soft launch it to existing investors first or will it be open to all from day one?

We will open the account to all comers straight away, not just existing investors.

I heard Assetz Capital is profitable? Can you walk me through some of the key facts of the financial side of the company, please?

Very few FinTech businesses are even close to breaking even, so it was a momentous day this year when we proudly claimed we made a seven-figure profit (GBP) for the last financial year to March 31st 2017. I believe that this is a testimony to our business model where we refuse to believe fast growth should be at the cost of profit and cashflow. While several others built their loan books up quickly with a more lenient approach to credit and very substantial levels of outside investment to cover trading losses, we took a more cautious approach to credit risk and built our entire business on an initial seed funding round of 1m GBP and Series A equity raising of just 5m GBP more. We have now lent similar levels to the whole of 2016/17 year in the first six months of this year and also booked profits of around the same as last year in this period. We have a healthy balance sheet and have just announced a new Series B equity raise that will bolster it further.

We had a very successful raise of 3.2m GBP on Seedrs in 2015, and now we are looking to fund a number of short-term capital expenditure projects, which are aimed to help the company continue its substantial growth. We believe that this may well be the last one prior to an institutional investment round or IPO but we will keep this under review and are really pleased to have not just delivered thousands of people great levels of interest through our platform but also delivered hundreds of investors a strong equity growth also as a result of the Series B being priced at 250% approximately of Series A carried out two and a half years ago..

What are your views on Brexit, the impact on UK fintech in general and on p2p lending in particular?

With the many political, regulatory and economic twists and turns of 2017, uncertainty continues. While many of those involved in business and investment are nervous, there are others benefiting and seizing on opportunities. Since the Brexit vote, no one is really sure of what the longer-term impact will be on businesses, investors or the UK market in general, however from the P2P market perspective, this has been an important year to further solidify its stature and firmly place it as a viable alternative to banks for both investors and borrowers.

We see that Brexit has actually had a positive effect on P2P, and all indications signal that the industry will benefit further in 2018 as a result of banks seeming to entrench somewhat ahead of the outcome being more visible. The impact on wider Fintech is more varied and we see a disincentive to set up in London to some degree for some businesses but for those here I expect they will take a wait and see approach. The possible loss of the ability to ‘Passport’ UK regulatory permissions across Europe or vice versa could be the major loss for companies intending to operate both here and in Europe.

The main issue is that the result of the Brexit vote is still some way off and indeed it is entirely possible we could see a continuation of the recent economic strength if Brexit turns out well economically and some real challenges if it does not. It is too early to call but the former would be my expectation on balance.

Where do you see Assetz Capital in 3 years?

Assetz Capital will continue to grow, to offer new and innovative products to investors and borrowers, and to hold true to our founding principles of fairness to all our stakeholders including investors, borrowers, shareholders and staff. We have already seen growth of around 100 percent year on year since 2014, and we believe that this rate will continue. We have very ambitious plans for the business, and certainly we see ourselves in three years as becoming one of the leading secured lenders to creditworthy businesses looking for additional funding as well as one of the top few P2P platforms for investors looking for choice, flexibility and fair, risk-adjusted returns.

We want to be recognised as being a real contributor to the economic success of the country, on several levels including helping house building volumes increase to address the housing shortage, helping businesses grow and increase employment, helping private investors earn more from their hard-earned capital, helping institutions deploy capital on market-leading risk return ratios and finally helping incentivise and contribute to a greater quality and breadth of financial education in today’s society.

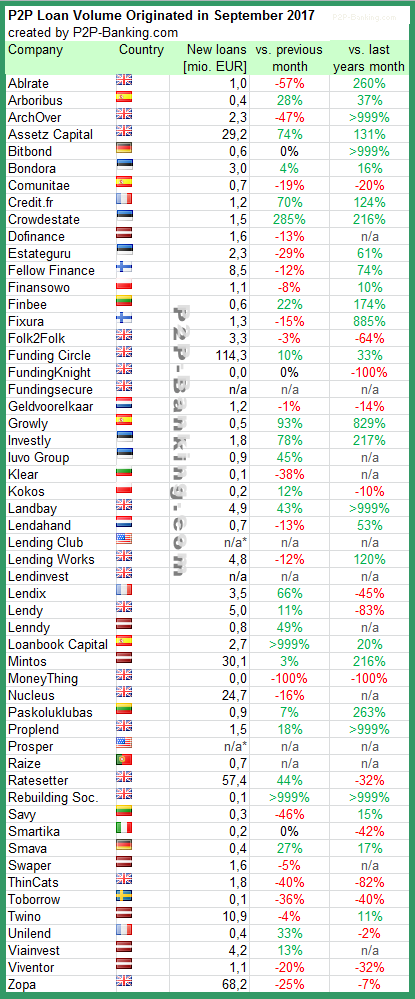

This p2p lending statistic table contains the loan originations of p2p lending companies for last month. Funding Circle leads ahead of Zopa and Ratesetter. The total volume for the reported marketplaces adds up to 404 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending services.

This month I added Raize, a marketplace in Portugal.

Want to meet representatives of many of the listed companies? Attend Lendit London in October – use discount code WiseclerkVip to get a 15% rebate on registration.

Table: P2P Lending Volumes in September 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Last year in September I signed up at UK platform Bondmason in order to test first-hand how an investment of 1,000 GBP would develop. As described in the review article, I wrote when I started, Bondmason is an aggregator that automates the investment across many p2p lending platforms for the investor and takes a fee for that. Bondmason projected a target return of 7% after fees and bad debt.

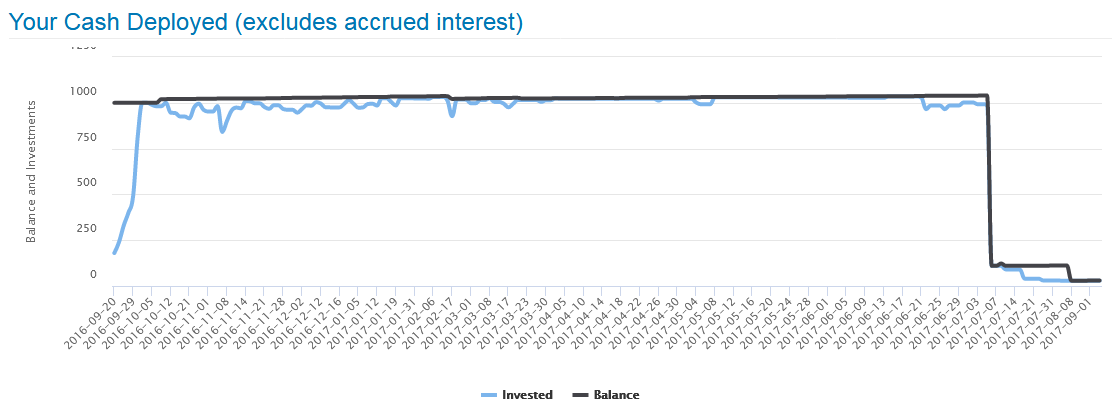

Allocation of my deposited funds into loans went okay. There was some cash drag, but not as much as other investors have experienced.

Deployment speed of my investment on Bondmason – click for larger image

What was bad, was that it became clear to me, that the interest level in combination with the non-performing loans would make it very unlikely for Bondmason to reach the projected return – at least for my portfolio. Especially with the Invoice Discounting loans there were issues.

In April 2017 Bondmason announced it would require a larger minimum investment amount of 5K (previously 1K) and raise fees for small portfolios to 1.5% (previously 1%). Dang. I was in no way interested to deposit more money. So my portfolio did not even get to celebrate 1st anniversary. In July I gave them notice to liquidate my portfolio/account. Since then I withdrew 1,013.94 GBP – only slightly more than I deposited. My account still exists as there is 20 GBP stuck in two property loans in default and also 1.41 GBP in cash.

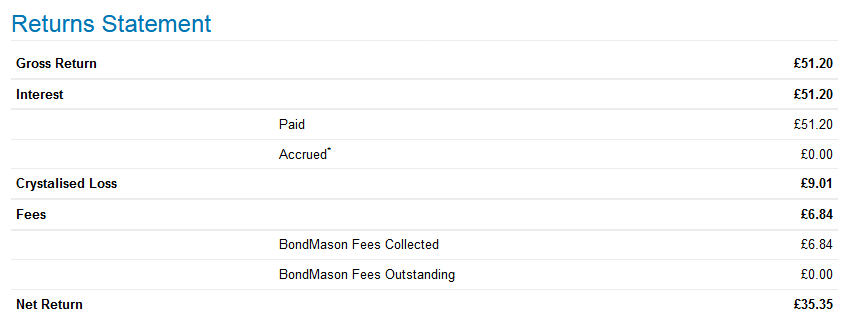

My Bondmason result (1) – click for larger image

My Bondmason result (2) – click to enlarge

Regardless of which way I look at it, the result is clearly bad. Obviously Bondmason by far missed the targeted return of 7% in my case. If I take an optimistic view and just assume, my 2 defaulted loans would recover today and the outstanding amount is paid to me, then my self-calculated yield (XIRR function) would be 4.3%. If I need to write off the 2 loans in default then my self-calculated yield is 1.9%. And that is before tax – as a German resident I cannot offset bad debt against interest earned for tax purposes. And on top of that the pound has been detoriating against the Euro value in the past 12 months (not Bondmason’s fault).

So to sum up: I liked the idea of an aggregator and the Bondmason setup allows passive investing in a diversified mix of p2p loans. But my returns are among the worst I ever experienced on p2p lending platforms and I am certainly happy I conducted this test with 1,000 GBP only and did not risk more.

If you want more details about the development of my portfolio throughout the past year there are more snapshots with screenshots over time in this thread.

The table lists the loan originations of p2p lending marketplaces for last month. Funding Circle leads ahead of Zopa and Ratesetter. The total volume for the reported platforms adds up to 391 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Milestones reached this month are:

Bondora reaches 100 million Euro in financed loans since launch

Want to meet representatives of many of the listed companies? Attend Lendit London in October -use discount code WiseclerkVip to get a 15% rebate on registration.

Table: P2P Lending Volumes in August 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

UK p2p lending Marketplace Funding Circle announced today that from September 18th, there will be an important change to how investors can invest on the marketplace. From that date Funding Circle will withdraw the option to manually choose which businesses to lend to and which loan parts to sell. Instead Funding Circle says it will launch a significantly improved and upgraded version of existing Autobid and Autosell lending tools.

Investors will be able to choose one of two new lending options based on their personal preference. Both options will be available as a Funding Circle ISA, which Funding Circle intends to launch later this tax year.

Balanced: you will automatically lend to the full range of creditworthy businesses (A+ to E), aiming to achieve an attractive, stable return. This will allow you to build a balanced portfolio similar to the makeup of small businesses in the UK today. The projected return is estimated to be 7.5% per year after fees and bad debt.

Conservative: you will focus on lending to businesses that have been assessed as lower risk (initially A+/A) but with a lower projected return. The projected return is estimated to be 4.8% per year after fees and bad debt.

Funding Circle gives the following reasons for stopping manual lending:

We launched Funding Circle in 2010 with the option for investors to either manually choose which businesses to lend to, or use our Autobid tool to build a portfolio based on their lending preferences. While many investors have enjoyed manually choosing loans, there are some drawbacks to it:

Many investors do not currently benefit from lending to all types of businesses: currently some investors can find it difficult to access D and E loans, which are some of the most popular. We want to ensure investors lending through Funding Circle have an equal chance of accessing all loans, and earn the best possible return.

It can mean your lending is not spread evenly across lots of businesses: currently many investors who manually choose loans are not fully diversified and are at risk of having a negative lending experience. We want to ensure investors spread their lending across lots of different businesses as this is the best way to earn a stable return.

It can be confusing for investors: many investors tell us they prefer a simpler, easy-to-use lending experience: 73% of new investors who join Funding Circle choose Autobid, and 80% of Funding Circle investors* say simplicity of lending is important to them.

* Independently surveyed by Cambridge University

Funding Circle will also make changes to the interest rates effective August 30th. Funding Circle says ‘When reviewing rates we take a number of factors into account, including macroeconomic trends, the expected mix of risk bands of borrowers, expected bad debt rates and wider competition in the market, which continues to be increasingly competitive for lower risk businesses. The new rates will allow you to continue to lend to established, creditworthy small businesses while earning an attractive, stable return.’.

Furthermore Funding Circle has removes sales fees for selling loans, effective today. There will be no more premiums and discounts possible on the secondary market.

Several p2p lending services have made similar moves discontinuing self-selection of loans to invest into and asking investors to use autoinvest options instead usually citing simplicity and ease of use. While this may be true for part of investors it certainly is not true for all of the investors. Especially among most active and vocal investors there are some that like to select loans manually and dislike if that choice is removed (Funding Circle says 73% of new investors use autobid).

Possible as a result of sentiments like that Bondora reintroduced more selection options with their Portfoloio Pro feature, after removing them earlier.