P2P Lending marketplace Lendy is in administration according to a statement by the British regulator FCA: “On 24 May 2019, following action taken by the FCA, Lendy Ltd, a regulated Peer-to Peer (P2P) firm, appointed Damian Webb, Phillip Rodney Sykes and Mark John Wilson of RSM Restructuring Advisory LLP as administrators. The same administrators have been appointed for two further related, but unregulated, firms: Lendy Provision Reserve Ltd; and Saving Stream Security Holding Limited. These appointments have been made by the firms, in respect of Lendy Ltd, with the consent of the FCA.”

There is an ongoing FCA investigation into the circumstances that have led to this action.

Lendy was in growing troubles over the past weeks. Lendy was put on a FCA watchlist in January. In April the FCA restricted the actions the company could take ‘[the firm must not] in any way dispose of, deal with or diminish the value of any of its assets and must not in any way release client money without in either case the prior written consent of the authority’. The interest payments for April, due on May 1st, were delayed for 2 weeks, which Lendy blamed on technical problems with the banking partner. Early today trading on the secondary market was suspended, when the ability to trade was removed. However the trading had nearly stopped anyway as there was little buyer demand.

Lendy finally succumbed the unsustainable level of defaults of the development loans and the unsatisfactory level of recoveries from these. Members of the management were furthermore already engaged in roles in other companies.

There is an outstanding loan portfolio of about 155 million GBP, of which about 90 million GBP are in default.

These events come a year after another property lending marketplace, Collateral entered administration.

Other European p2p lending companies that failed include Boober, Comunitae and Trustbuddy.

I covered my p2p lending portfolio periodically over the past 12 years in this blog. The following report is a snapshot on how it is composed right now (May 2019) and which strategy I will take for the next months. As you can see below I aim for a widespread diversification (over different platforms as well as geographically) of my p2p lending investments.

Mintos

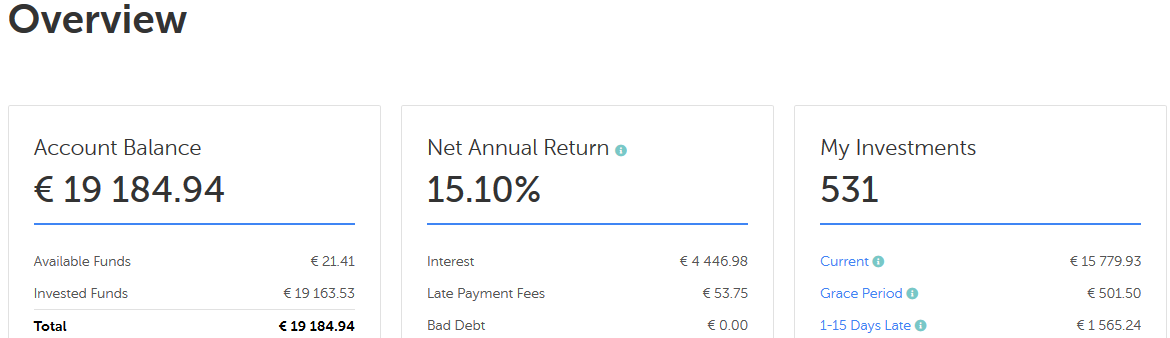

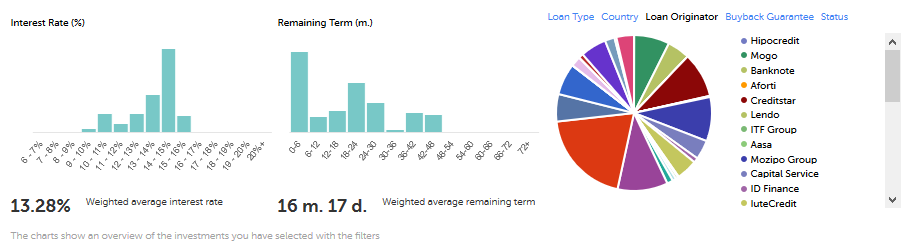

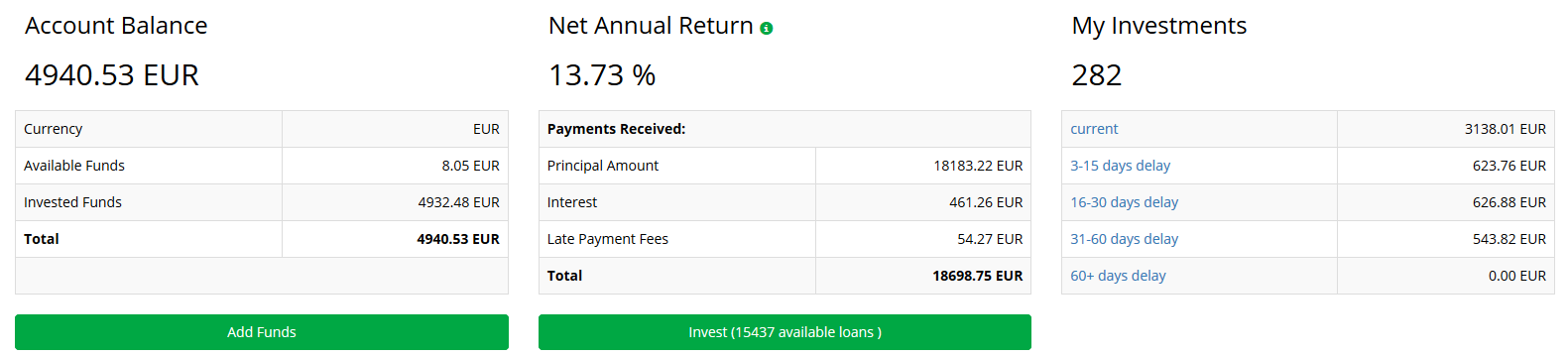

Mintos* is my biggest position. I run a trading strategy on Mintos. Mintos gives my net annual return as 15.1%. Calculating it myself based on the deposits and withdrawals I get a XIRR value of 24.8%. The cause for the huge discrepancy is that Mintos does not account correctly for the cashback of the campaigns. I heavily traded, when Mogo ran a campaign. For example I invested in new Mogo loans that were offered with a 2% cashback on the primary market, nearly instantly sold them with 1.8% discount on the secondary market and pocketed the cashback. Rinse and repeat.

I am satisfied with the current degree of diversification over loan originators in my Mintos portfolio. The bulk of my investments is in loan terms between 3 and 30 months at interest rates ranging from 13% to 15%. The lower interest rate loans are usually only held temporary as part of my trading strategy.

For the coming month I plan to keep my Mintos* investment at roughly that amount, reinvesting the paid principal and interest. New investors registering via this link at Mintos, get 1% cashback on amounts invested in the first 90 days. Mintos is currently not accepting UK investors.

Linked Finance

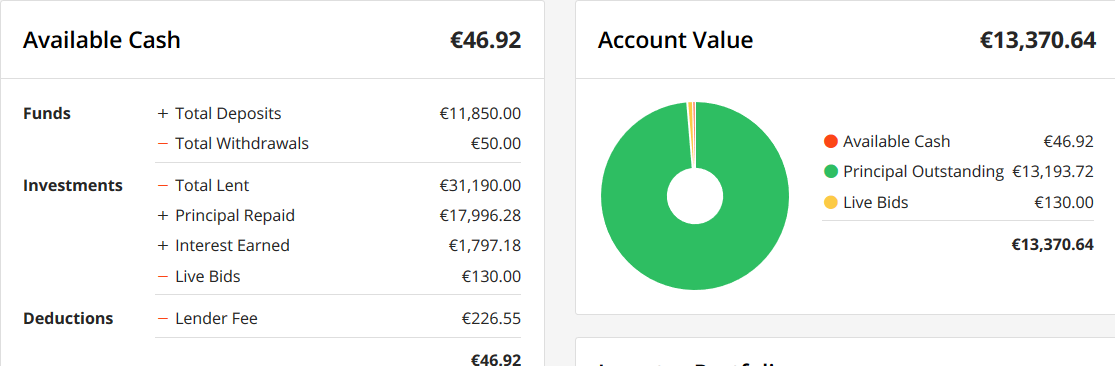

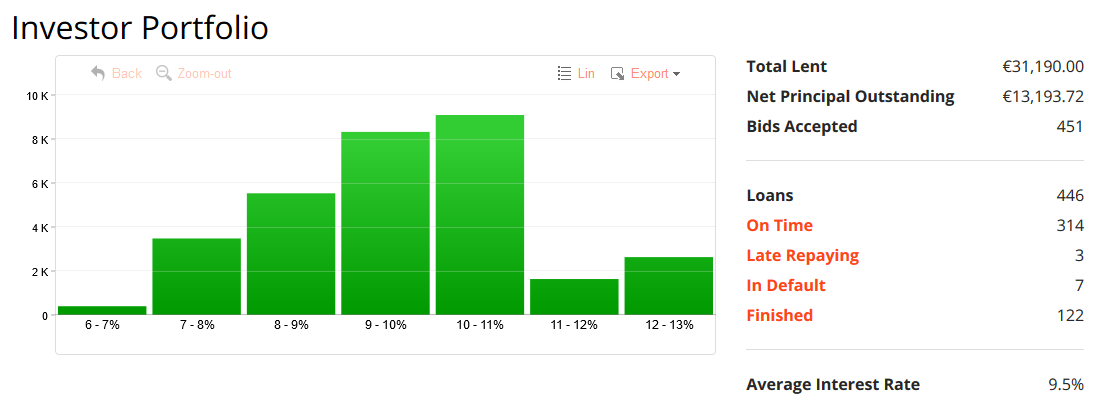

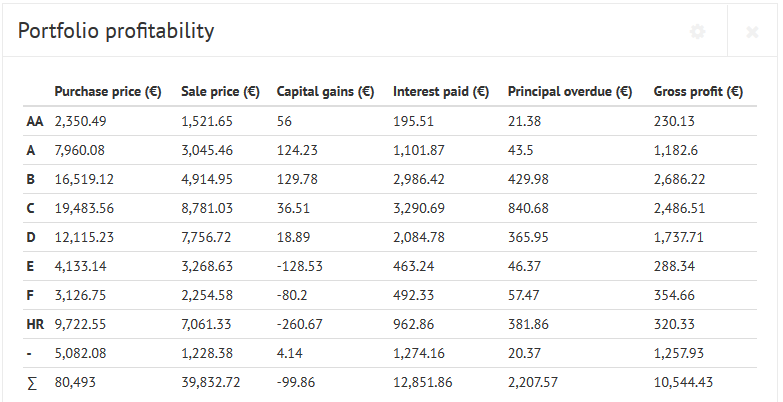

My second largest p2p investment is on Irish SME loan platform Linked Finance.

Diversification achieved is good. The majority of my loans have interest rates between 8% and 11%. Most loan terms are 2 or 3 years.

I “collected” 7 loans in default (double dip on the golf loan). But 5 of these had repaid more than half the principal before they want into the default state so the principal in default sums up to only 270 Euro. My self-calulated XIRR value is 6.4% if I totally write off the amounts in default and 7.1% if I assume that half the amount in default will be recovered. I plan to slightly increase my Linked Finance* portfolio in the next months. Linked Finance is not offering any cashback or bonus rewards for new investors.

Bondora

Bondora is my third largest and oldest (still running) p2p lending portfolio. I started in 2012. My self calculated XIRR value is 16.6%. A yield that high is not achievable nowadays anymore. My portfolio profited heavily from the first years when interest rates were typically 28% to 34%.

I am currently investing into Estonian A and B loans using these autoinvest settings. I have used these settings unchanged for 11 months now and it is running totally hands-off with no maintenance required.

On Bondora* I reinvest the bulk of my repayments and occasionaly withdraw some funds. New investors registering on Bondora using this link get a 5 Euro sign-up bonus.

Ratesetter Australia

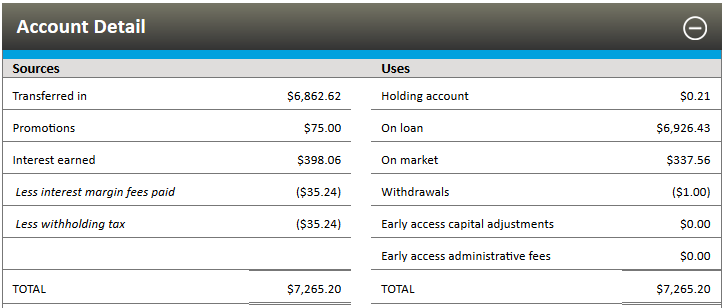

Ratesetter Australia* is my fourth largest p2p investment and also one of my youngest. I started in August 2018. My XIRR value self calculated in AUD is 9,1% if I include the 75 AUD sign-up bonus and 7.4% if I do not include that.

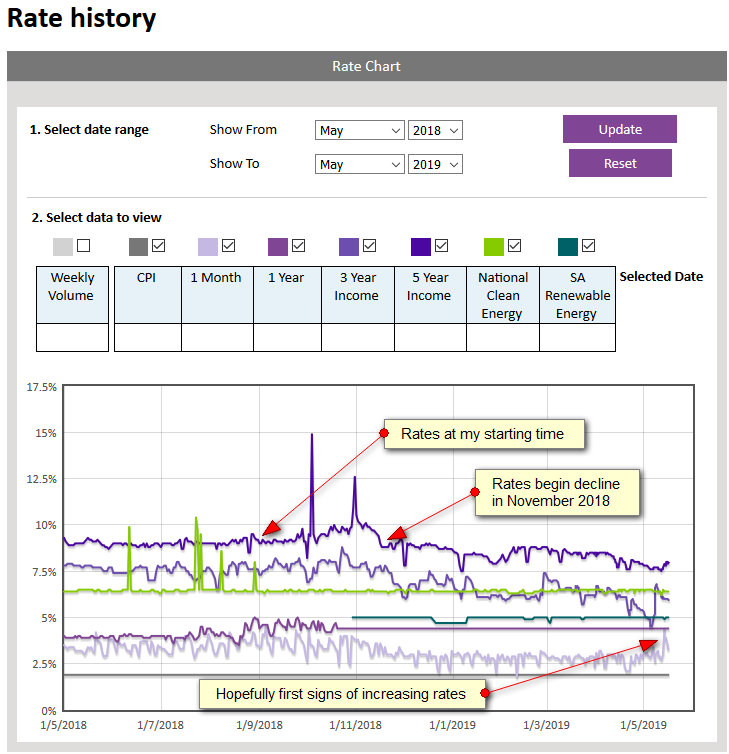

My money is mostly invested on the Ratesetter 5 year market at an average rate of 9.2% (that is after fees but before withholding tax).

In the past months the interest rates have dropped considerably therefore I am parking some funds on the 1 month market or invest them on the 3 year market.

I am reinvesting all repayments at Ratesetter Australia. If rates go up again I plan to do that on the 5 year market, otherwise I’ll settle for the 3 year market. It is a little complicated to register as a non-resident, but I have described how I managed to sign up as a European here. New investors can earn a 75 AUD promotion bonus by investing 2,000 AUD or more in our 3 year Income or 5 year Income lending markets before 31st May 2019. Achieving that requirement in time will not be easy, even if you start directly.

Iuvo Group

The fifth largest position of my p2p portfolio is invested at Iuvo. It is running hands-off and does not require any maintenance.

I continue to reinvest all repayments. Iuvo pays new investors a very generous cashback of up to 90 EUR. For more details and how to get it see the cashback overview page.

Estateguru

After I completely exited Lendy in last autumn, baltic Estateguru* is now my largest platform for property secured loans. I don’t use the autoinvest. Instead I periodically login and manually invest into a new Estonian loan secured by a first rank mortgage.

I mostly reinvest all repayments. New investors get 0.5% cashback for all investments in the first 90 days, if they sign up using this link.

Fellow Finance

I used to have a larger portfolio at finnish Fellow Finance but I did not want to go below 12% for 4 star Finnish consumer loans therefore I started withdrawing funds last year. In January the sale price collections paid tor Finnish loans dropped from 70% to 53% which reinforced my decision to exit.

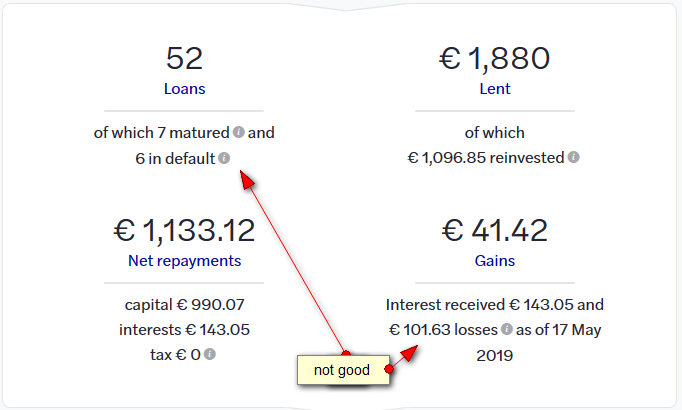

October

I am running down my portfolio on French SME loan marketplace October. With the low interest rates and rising defaults (6 out of 52 loans) in my portfolio the risk reward ratio is not for my taste anymore.

New investors signing up on October using this link* can get 20 EUR bonus (200 Euro minimum investment)

More p2p lending marketplaces

Due to professional interest (want to gain first hand experience) and curiosity I have more p2p lending portfolios at Ablrate* (small, reinvesting), Assetz Capital* (tiny, reinvesting, possibly increasing), Bulkestate* (tiny, testing), Crowdestate* (small, reinvesting), Finbee* (tiny, nearly exited), Investly (small, reinvesting), Lenndy* (tiny, watching), Monestro, (tiny, exiting), Moneything* (small, exiting), Neofinance* (small, testing, probably running down), Reinvest24* (small, testing), Robocash* (small, reinvesting), Zlty Melon* (tiny, exiting next month when terms are up).

Crowdinvesting

Not p2p lending but investing in startups. I am a huge fan of Seedrs*. Investing in startups is of course even higher risk than investing in p2p lending. Nevertheless I went ahead and built a big Seedrs portfolio over the last years. Snapshot:

P2P Conference Riga

I am looking forward to be at the P2P Conference in Riga* which is less than 4 weeks away. The conference is reasonably priced (enter promotional code P2PEARLYBIRD40 for 40% rebate) and Riga can be reached with cheap flights from many European cities. BTW, Riga is an interesting town, if you have not been there yet you could combine the conference with some sightseeing.

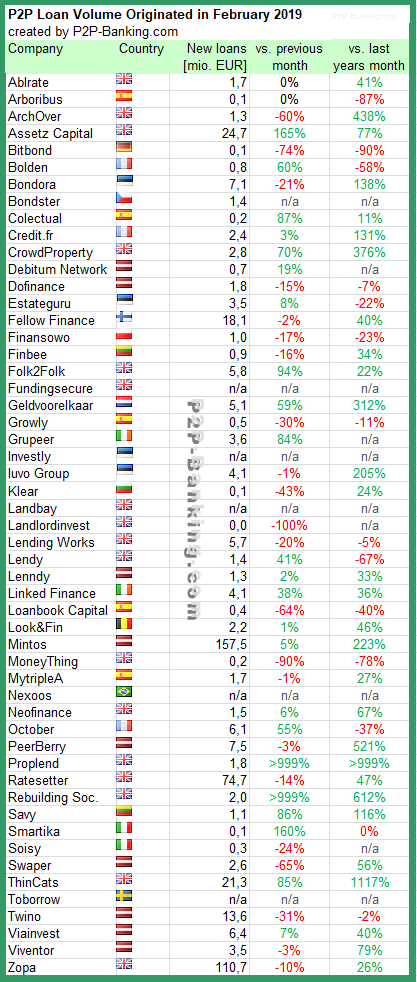

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Zopa and Ratesetter*. The total volume for the reported marketplaces in the table adds up to 571 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Milestones achieved this month (total volume since launch):

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Zopa and Ratesetter*. The total volume for the reported marketplaces in the table adds up to 582 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Milestones achieved this month (total volume since launch):

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Zopa and Ratesetter+. The total volume for the reported marketplaces in the table adds up to 531 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

This month I added Bondster* (use Bondster Promotion Code 5506 to get 1% cashback).

The FCA, the Financial Conduct Authority, is the supervising regulatory body for p2p lending platforms in the UK. In Dec. 2018 it refused the application of Mintos* or more precise of a separate legal entity within the Mintos group, established for operations within the UK.

The full notice of the FCA decision can be read here. Below I outline some of the aspects. I also reached out to the Mintos CEO, who kindly answered my questions on this matter.

Before we go into the details, I want to make it clear, that the FCA decision has no direct impact on the current operation of Mintos platform, which is headquartered in Latvia.

Mintos Marketplace Limited applied for permission to conduct a specific regulated activity (“permission to operate an electronic system in relation to lending (Article 36H RAO)”).

Reading the FCA decision there are several points that led to the refusal:

a) the applying company does not currently meet the minimal funding requirements of 50K GBP as specified by the rules (paragraphs 49-50 of the notice)

b) the head office of the applying company is not currently in the UK (51-53)

c) the FCA has doubts that the Mintos business model will be adapted adaquately to comply with the UK regulation rules (paragraphs 29-33, 35-38, 40)

d) the FCA find Mintos wind-down plans are not specific enough (41-44)

e) the FCA is not satisfied with Mintos’ understanding of the UK rules (46-48)

The decision is interesting to read. Naturally it judges Mintos solely by the formal compliance regarding the UK rulebook. Any other non-UK marketplaces seeking FCA approval can certainly learn some things from this declined application. As I stated above, it does not have any consequences for the current operation of the Mintos marketplace. It only affects any potential plans Mintos had for the UK market.

That gets us to the more interesting point: why did Mintos strive to get FCA approval still in 2018 despite Brexit? I asked Martins Sulte, CEO of Mintos, and here are his answers:

1) What was the intention of Mintos to set up the seperate UK entity and apply for permission at the FCA. Was this related to offering IFISA products and possible tax advantages for UK investors?

The intention is to connect to our marketplace loan originators originating loans in GBP in the UK and offering those loans to investors from the UK. We believe that the UK can become a self-sustaining marketplace where local investors are able to fund loans originated locally in the UK.

2) Considering that the application was pursued still as recent as July 2018 (point 29), this is an interesting move in light of Brexit, with several UK fintechs going the other direction to secure a continued presence in the EU. Any comment?

We view the UK market as a separate market that has the UK specific regulatory environment when it comes to crowdlending. Our intention is to create a largely self-sustaining UK marketplace that serves both UK loan originators and UK investors. In that light uncertainty caused by Brexit plays less of a role. It is important to note that each and every country has their own approach to regulating crowdlending, which means that for instance having the FCA permissions for working in the UK would not really affect our operations in other countries, even in EU. Only when the European Commission’s proposal for a regulation on European crowdfunding services providers come into place we might see that licenses are passportable across the EU and then in that light, the Brexit certainly would more of a consideration. For now, we have to look at each country separately.

3) Is the announcement of the application for an e-money license a reaction to the upcoming decision by the FCA?

No. E-money licence and UK permissions are very different licenses.

4) Do you think that any of the assessments the FCA made, will be relevant for the Latvian regulator once the Latvian regulation is finalized?

I don’t think so. Each country has its own approach. The UK has a rather specific approach. When we talk about Latvian regulation we also have to take into account that it will cover only investors and loan originators in Latvia. Once the Latvian regulation is finalized we will still have to look at each country separately. Us having a necessary license in Latvia will play a little role when considering our operations in, for example, Mexico, South East Asia or Russia, or even in other countries of EU.

Martins added: ‘This was a formal Financial Conduct Authority (FCA) decision on Mintos’ application for operating in the United Kingdom submitted by the Mintos Marketplace Ltd (a separate legal entity within Mintos group that was established for operations in the UK). The application was submitted almost two years ago. In these two years, our business model has evolved, our team has expanded significantly and we have gained major business results on a European and global level that defined our position as a leader in the market of investments in loans. The application for necessary permissions to operate in the UK doesn’t affect our daily business and the future development of Mintos, and the rejection of the application is nothing that can, nor will, affect our business operations in other countries.

The UK has different and specific legislation, and the FCA notice serves us as valuable feedback for adjusting our processes and procedures to fit the UK specificities. At the moment, we are in no rush when it comes to entering the UK market, as we are all aware of the many uncertainties regarding the Brexit issue. Anyway, our growth and expansion goals are unwavering, and entering the UK market will remain in the scope of our interest. We will continue working with our legal and regulatory advisors and will take into account the FCA’s feedback when considering our next steps with respect to the UK.’