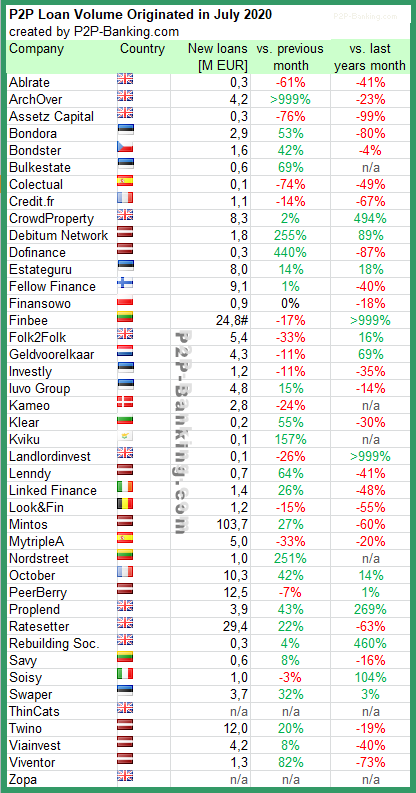

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Ratesetter* and Finbee*. The total volume for the reported marketplaces in the table adds up to 275 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Table: P2P Lending Volumes in July 2020. Source: own research #note: Finbee loans include SME support loans originated via the platform by the Lithuanian government

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations.

Metro Bank today announces that it has agreed to acquire Ratesetter* (Retail Money Market LTD) for initial consideration of 2.5 million GBP, with additional consideration of up to 0.5 GBP million payable 12 months after completion subject to the satisfaction of certain criteria and further consideration of up to 9 million GBP payable on the third anniversary of the completion of the transaction, subject to the satisfaction of certain key performance criteria.

The acquisition does not include Ratesetter’s holding in Ratesetter Australia which is being retained by Ratesetter shareholders.

Ratesetter will no longer use money for retail investors to fund new loans. All new loans will be funded by Metro Bank’s depositor base. Ratesetter will continue to manage the existing Ratesetter loan portfolio and Provision Fund on behalf of its existing peer-to-peer investors, with Metro Bank assuming no credit risk for these existing loans.

Ratesetter states “For investors, there is no change to your investment, with RateSetter continuing to manage the loan portfolio and the Provision Fund. Our Investor Services team remains available in the usual way to assist with any questions you may have and will continue to provide all administrative services. “. Retail Investor reactions on the announcement are mixed. While some welcome the development thinking that it will stabilze Ratesetter and reduce mid-/longterm risk for repayment of outstanding funds, others worry that the risks for their committed funds might increase as there will be no new loans and managed funds will thereby decrease.

Metro Bank will operate Ratesetter as an independent platform and originate loans under both the Ratesetter and Metro Bank brands.

Rhydian Lewis and Peter Behrens and CFO Harry Russell will join Metro Bank’s  team. The transaction will be funded from existing cash resources, whilst the final fair value and goodwill elements will be determined as part of the Company’s year-end accounting process. The acquisition is anticipated to reduce the Company’s CET1 ratio by circa 0.3% at 30 June 2020 on a pro forma basis.

The acquisition is conditional upon approval from the Financial Conduct Authority and shareholders holding at least 60 percent of Ratesetter’s shares acceding to the relevant transaction documents and is expected to close by the fourth quarter this year. The board of directors of Ratesetter unanimously recommends the transaction and that shareholders of Ratesetter accede to the relevant transaction documents. Shareholders holding 45.7 percent of Ratesetter’s shares have signed the relevant transaction documents at the date of this announcement. Once Ratesetter shareholders holding 60 percent of Ratesetter’s shares have signed or acceded to the relevant transaction documents, it is expected that Ratesetter shareholders who have not signed or acceded to the transaction documents will be dragged into the transaction, resulting in Metro Bank acquiring 100 percent of Ratesetter’s shares at completion.

I use Seedrs* to invest into the equity of British startups since 2013. I have written about several aspects and my experience in the past here on the blog. Overall my results are very satisfying. My annualized return (IRR) is currently 23.4%. As I am not a UK resident I forego the tax benefits of EIS/SEIS which according to the Seedrs*Â dashboard would have pushed my IRR to 28.1% The one caveat is that some of the profits are paper gains, yet to be realized. But I cashed out on some substantial gains already, especially Revolut and Landbay shares via the Seedrs*Â secondary market. I invested mostly (81%) in fintech startups – for those interested in the details here is a screenshot of my recent portfolio.

Since 2017 Seedrs* provides a secondary market allowing investors to sell shares to each other. Depending on how in demand the traded startups are, shares sell out within minutes/seconds or the market opening (e.g. Revolut shares in 2019). The secondary market opens only for one week a month, a measure Seedrs has taken to heighten liquidity by concentrating demand and supply.

Up to now prices for the traded part were fix and changed seldom determined by ‘fair value‘ settings. Simplified in most cases the value of shares was set based on the valuation the startup raised capital on its last round. The price changed only with a new round and that usually happend only once every 1-2 years (see the picture, the curves are in most cases straight lines as there are only two datapoints). Furthermore the valuation of the startup is set (controlled) by the startup itself (unless there is a large professional investor like a VC participating in the round). I don’t want to do an excursion into the possible methods of startup valuation as that would make a rather long article, but rather say that some valuations of Seedrs pitches seemed rather inflated to me.

As early as Dec. 2018 Seedrs announced that it intended to enable variable pricing on the secondary market trading.

Since yesterday evening variable pricing is now live on the Seedrs* secondary market. Sellers can list their shares with discounts of up to -30% and premiums of up to 30%. Unfortunately Seedrs only allows steps of 10% and not granular 1% prices increases.

This will allow me some interesting experiments with the pricing feature

So far I mainly used the Seedrs secondary market to

a) buy to increase my stake in promising stakes in promising startups I already held and where I saw potential for further strong growth

b) sell shares to realize profits

The investment time frame for this has been multiple years. With flexible pricing there might be chances for some trading opportunities on shorter time spans.

In the early times of the secondary markets on Bondora* and Mintos* I did a lot of active trading. My learning was that there was a time span of several months when I could trade very profitable due to the fact that these secondary markets where very new, everbody had to learn which trading strategies worked best and there was a big mismatch between supply and demand. After a few month the opportunity vanished as traders got more professional and margins diminished. And the effort had to be worth my time invested. But those first months in a new market taught me a lot about market dynamics and market psychology, brought good profits and I had a lot of fun.

Repeating that on the Seedrs secondary market will not be easy. First of all the transaction fees on Seedrs secondary market are high. Second trading is not real time (it takes days for transactions to settle). And third the demand concentrates on a few startups that investors deem attractive while there is little buyer demand for all the other startups. On the other hand demand for startup shares is much more driven by expectations and emotions than on the p2p lending markets, where there are hard figures like YTM (yield to maturity) to gauge available parts on offer against each other.

Simply wishing to buy a share at -30% and then resell it at +30% obviously won’t work. But maybe buying at -30% and later reselling at -10%?

I sold more than 95% of the Revolut shares I held in May 2020 at the fixed fair value. There were a lot (about 2M GBP) of Revolut shares on offer in June and July trading cycles which went unsold. I will watch closely whether any offers at -30% will show up next trading cycle. At that price point I might be tempted to buy them again. At the time of this writing there is one lot on offer at -30%, three at -20% and multiple at -10%.

What’s your take on the introduction of variable pricing on the Seedrs secondary market. Share your opinion in the comments.

This article is not an investment advice. Investing in startups bears significant risks, including total loss of investment.

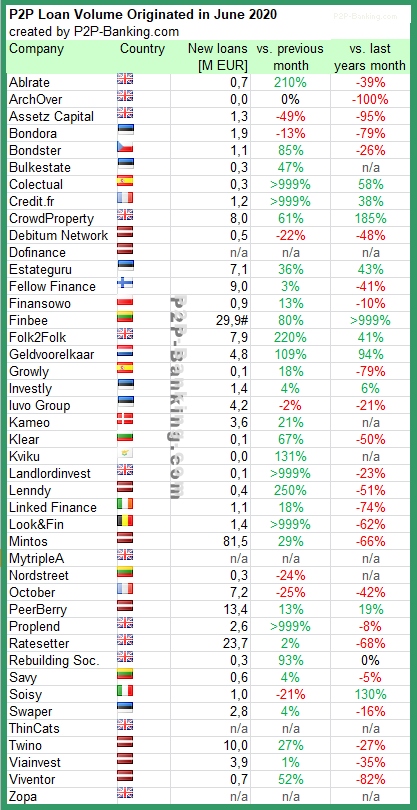

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Finbee* and Ratesetter*. The total volume for the reported marketplaces in the table adds up to 236 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms. This month I added Kviku*. I delisted Smartika as it does not seem to have originated any new loans for 5 month now.

Table: P2P Lending Volumes in June 2020. Source: own research #note: Finbee loans include SME support loans originated via the platform by the Lithuanian government

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations.

Detailed investigations have been undertaken into the Company’s affairs during the period covered by this report, with the assistance of the Joint Administrators’ instructed solicitors Pinsent Masons LLP. The investigations have included carrying out reviews of the Company’s books and records, performing detailed analysis of the Company’s bank statements and reviewing the results of key word searches of the c480,000 Company emails held by the Joint Administrators.

The Joint Administrators have now also carried out interviews with both Liam B.. and Tim G.., the former directors of Lendy. The investigations have been concerned with a number of transactions, most significantly payments of approximately £6.8million that were paid to entities registered in the Marshall Islands for apparent marketing services carried out for Lendy. It is the Administrators’ position, however, that these payments were ultimately for the benefit of Liam B.. and Tim G…

As a result of these investigations, on 1st June 2020 the Joint Administrators made an application to Court for a worldwide freezing injunction to be granted over the assets of Liam B.. and Tim G.., as well as proprietary injunctions on the properties owned by companies linked to the directors, RFP Holdings Limited and LP Alhambra Limited. The Order was granted on the 4 June 2020. Proceedings have now been commenced against Liam B.., Tim G.., RFP Holdings Limited and LP Alhambra Limited. Owing to the nature of these claims, the Joint Administrators are unable to provide further information at this time.

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Ratesetter* and Finbee*. The total volume for the reported marketplaces in the table adds up to 188 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms. This month I added Nordstreet*.

Milestones achieved:

Finbee* crossed 50 million EUR loan volume since launch