Compared to other European markets the Swiss p2p lendng market has been late in developing. Regulatory hurdles and an upper limit on interest rates for consumer loans of 10% (12% for card loans) have slowed development of the market. But it seems that real estate loans finally delivered a break through in 2019-2021.

The new study ‘Marketplace Lending Report Switzerland 2022‘ by Simon Amrein, Nadine Berchtold and Andreas Dietrich of Lucerne University delivers a detailed analysis of the market.

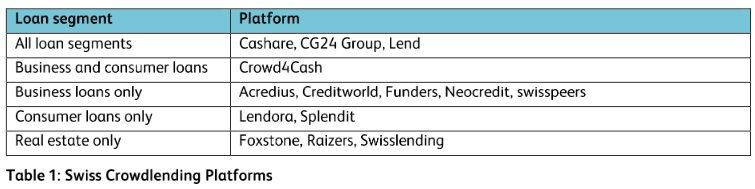

According to the report there are currently 14 platforms active in the market:

Source: Marketplace Lending Report Switzerland 2022, p. 7

Several banks and insurances have taken stakes in platforms:

Funders is operated by the Luzerner Kantonalbank and licensed to other cantonal banks

The Lendico platform was acquired from PostFinance by Lend (Switzerlend AG) in 2019. PostFinance has acquired a stake of Lend in a reciprocal move.

Neocredit was launched in 2019 by French platform credit.fr and the insurance company Vaudoise. Since 2022, the Vaudoise Group has been the sole shareholder of neocredit.ch

In December 2021 the Basellandschaftliche Kantonalbank bought a stake in swisspeers AG as a strategic investor.

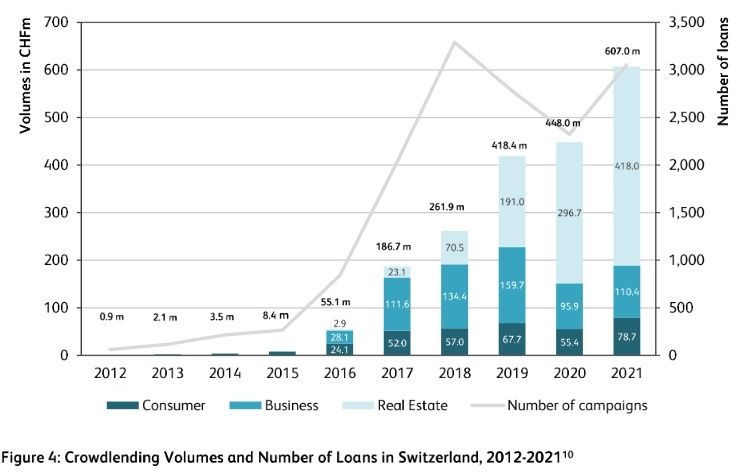

According to the report the p2p lending segment reached a record volume of 607 million CHF new loans in 2021 with a growth rate of 35.5% from 2020 to 2021. The largest share 418 million CHF went to real estate loans. The major driver were loans to companies in the real estate business. Many of these loans are issued as short-term credits to be later redeemed by banks.

Source: Marketplace Lending Report Switzerland 2022, p. 8

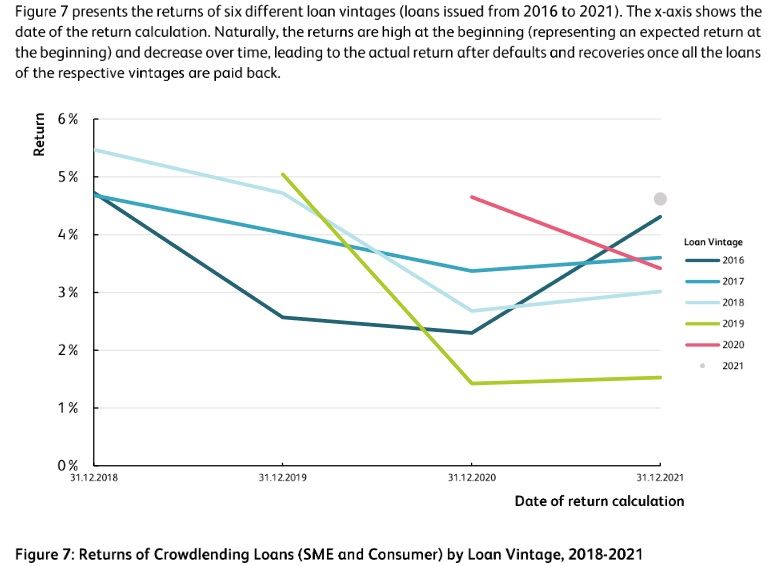

The study finds: ‘The COVID-19 crisis in 2020 has been one of the biggest crisis in Switzerland during the last decade. Despite increased default rates , the returns both in the consumer and the SME segment remained positive and recovered in 2021. The current situation remains challenging for the economy and financial markets, given the high inflation and rising interest rates’.

Source: Marketplace Lending Report Switzerland 2022, p. 11

The study has several conclusions, some of which are:

Rebound effect after COVID crisis: ‘Before the .. crisis returns … were high and risk – measured by default rates – low. The crisis was an important test, providing investors with a realistic risk and return profile of the asset class‘

Changing interest rate environment is a test for online business models

Sustainability is increasingly becoming a topic in the debt market

More transparency, more relevance: ‘… Increased relevance will require more transparency in the market … for institutional and private investors‘

Swiss invoice finance platform Advanon has to deal with a large fraud case. A client allegedly made up invoices for non-existing transactions and submitted forged invoices, bank records and emails. These invoices were then financed on the Advanon platform by 78 private investors. The fraud continued undiscovered for about a year racking up a total damage of 2.4 million CHF (approx 2.1M EUR).

2.4M CHF may not sound a very large absolute sum for a p2p lending company, but Advanon so far had financed invoices of only about 60M CHF in 2017, so the potential loss equals roughly 4% of the total yearly volume. And the exposure per investor is unusually high for a p2p lending marketplace as the affected investors could face a 30K CHF loss on average. Media speculation is that they might face a total loss. Advanon has about 3,000 registered investors, the majority from Switzerland with a few German investors. Advanon offers interest rates between 6-20%.

“We founded Advanon with the mission to help SMEs meet the ever-increasing payment deadlines and thus have a positive impact on the SME economy and its growth. It is frustrating and intolerable that this was being exploited by fraudsters with great criminal energy. We are mobilising all our efforts to fight for our investors and to recover the money they have invested.†Several lawyers and the entire management are working on the case. “We will adjust our strategic direction,†said Advanon CEO Lojacono. As a consequence, only institutional investors will soon be admitted to the platform. Advanon has always emphasized that investing in a high-risk asset class like factoring should only be considered as part of a diversified portfolio.

The case is now investigated by the public prosecution body.

Last November Advanon announced a pilot project for an invoice financing cooperation with insurance company AXA Wintherthur.

Finnest.com is the only platform successfully providing modern corporate finance for well-established Mittelstand companies (no start-ups). Borrowers are mostly AAA-like rated brands and industry leaders that have been on the market for years (often decades) and are able to demonstrate a sustainable and profitable growth path.

These top-companies are actively seeking alternatives to their traditional bank loans and want to diversify their finance mix. For the first time, Finnest.com gives these Mittelstand champions access to the capital market. The platform is a 21century version of a classic corporate bond bookbuilding process and provides end-to-end financing solutions.

Currently, Finnest.com is licensed and active in Germany, Austria, Switzerland and Slovakia.

What are the three main advantages for investors?

1.) Investors get access to a completely new class of investments, previously reserved for a handful of professional investors. 2.) On Finnest.com, investors select the interest rate of their choice! Only if the company agrees to pay this annual rate (or more), will a deal be closed. 3.) Investors can invest in local and regional companies that create jobs and income in their area.

What are the three main advantages for borrowers?

1.) For the first time, Finnest.com provides this segment of well-to-do Mittelstand borrowers with access to the capital market previously reserved for large corporations. 2.) Mezzanine financing as provided via Finnest.com strengthens these companies’ balance sheets. 3.) An enormous PR & loyalty effect – when customers invest into “their†brand, the term “brand messenger†gets a rich new meaning.

What ROI can investors expect?

On Finnest.com, investors select their interest rate of choice. On average, companies have paid out 5.5% annually fixed interest rates. The concept works: a Finnest investor invests about 7.000 Euro per transaction, that is roughly 20 times higher than on other online platforms.

Finnest charges investors a fee of 1% (minimum 25 Euro). Doesn’t a high fee hinder diversification?

We are one of the few (the only?) platform that charges an investor fee. It’s 1% of the invested amount. That means if an investor invests 7.000 Euros, she/he is charged 70 Euros once. That’s it. We haven’t learned of any investor who would not invest because of this small fee.

Finnest.com uses subordinated loans (‘qualifiziertes Nachrangdarlehen’). An Austrian court recently ruled that this structure severely disadvantages investors. Why did you choose this structure rather than standard loans?

Headquartered in Austria, Finnest.com is licensed by the Austrian AlternativfinanzierungsGesetz (alternative financing law). This law (just like its German counterpart, the Schwarmfinanzierungsprivileg) actually requires us to use subordinated loans. It’s the tool the law selected. The court ruling you refer to, addressed one specific contract by one single issuer who did not use any legally checked platform, but decided to do this financing on his own. Apparently, that was not such a smart idea – that contract must have been quite bad and the court ruled accordingly. Our contracts are thoroughly checked by leading law firms in each jurisdiction and have been presented to the financial authorities, of course.

How did you start Finnest.com?

For many years, Günther Lindenlaub, my co-founder, had been in charge of capital market transactions for one of Europe’s leading banks. While he saw, that large corporates keep using tools like corporate bonds to diversify their finance mix, the banks we not able (or willing) to offer something similar to the Mittelstand. But bonds are too complex and costly for the Manners and Almdudlers of this world. So, he decided to create his own platform – Finnest.com.

Is the technical platform self-developed?

Yes. It was built by a team that had previously built part of ING-Diba and AustroControl, the Austrian flight control agency. These guys know everything about stability, security and usability. We like to joke that we did not build a Tesla but one of those 80s’ Volvos with the iron bars in the doors. Very safe, very stable, drives, and drives, and drives.

Was the company funded with venture capital? Is the company profitable now?

We were lucky to attract Speedinvest, the largest Austrian VC, as our seed investor. And we have added a carefully selected group of international angels and VCs since. As we are still growing fast, we are not profitable, yet. But we are doing very good business.

Are there any new features for the platform your team is working on? What about a secondary market?

We are expanding: As we are speaking, our team is in the last phases of building a new, second platform. It will provide a similar service as Finnest.com does, but it will address a different market segment: large corporations on the one hand and professional as well as institutional investors on the other hand. Modern corporate finance XL, so to say.

Which country are you most successfully attracting investors in?

Even though we originate in Austria, Germany is our prime market. Already today, the majority of our investors comes from Germany and we have just hired new team members focusing mainly on the German market.

You plan an expansion beyond Germany, Austria and Switzerland. What can you tell us about your next market(s)?

Our industry is a highly regulated one, governed by national rules and regulations. But with the new platform, we will be able to provide a pan-European service. That will open a completely new scale of opportunities for us.

Do you plan to cooperate with institutional investors? In which way?

Yes, definitely. The new platform will be customized for their interests and needs.

What is the current state of the market in Austria?

With the passing of the AlternativfinanzierungsGesetz, (alternative financing law), the online financing market grew at a rapid pace. We have now more than a dozen platforms and high 2-digit number growth rates. But of course, business in Austria is always only a fraction of that in Germany. Germany is the main market we are focusing on.

Where do you see Finnest in 3 years?

We believe, that in 2020 there will be three main platforms financing larger, successful companies across Europe. Finnest.com should be one of them.

PostFinance one of the largest five retail banking institutions in Switzerland will partner with Lendico to launch joint venture Lendico Schweiz, which will facilitate loans to SMEs in Switzerland.

From the last quarter of 2016 onwards, the company will facilitate crowdfunding for small and medium-sized enterprises (SMEs) in Switzerland. It is entering the market in close collaboration with PostFinance, a subsidiary of postal carrier Schweizerische Post.

Together the partners would like to establish a new form of SME financing in Switzerland. The aim of the joint venture is to provide the numerous Swiss SMEs with a modern alternative to traditional bank financing. The two partners are contributing their complementary expertise in customer contact and the entire lending and repayment process to the joint venture.

Sources say PostFinance was barred by regulation to directly lend to SMEs and had to find a third party partner to enter this market.

‘With 110 years of experience in Swiss banking services and around three million customers, we can think of no better partner than PostFinance for our entry into the Swiss market. As part of the continued expansion of an international credit marketplace, this joint venture represents a significant step in our business development,’ says Dr Dominik Steinkühler, co-founder and managing director of Lendico.

Hansruedi Köng, CEO of PostFinance, is delighted to be able to join forces with Lendico, a partner which has established itself and enjoyed success internationally in a rapidly expanding industry. ‘Our vision for this cooperation is to take crowdlending in Switzerland from niche status to the mass market. The combination of Lendico’s innovative capacity and our structures in Switzerland offers the best conditions for Lendico Schweiz AG to become a market leader in the future.’

Deutsche Börse Venture Network adds Swiss p2p lending marketplace Cashare to its program. The program by the German stock exchange is designed to aid innovatice companies to get better access to financing from investors.

Cashare was established in 2008 and facilitates loans to consumers and SMEs in Switzerland on its marketplace. According to the website 1,111 loans have been financed. Due to regulatory reasons each loan can be financed by a maximum number of 20 different investors.

Prof. Dr. Andreas Dietrich of the Lucerne University of Applied Sciences and Arts, Simon Amrein, Reto Wernli and Dr. Falk Kohlmann have published the study ‘Crowdfunding Monitoring Switzerland 2015‘. It analyses the development of crowdfunding in Switzerland giving special attention to the development of p2p lending.

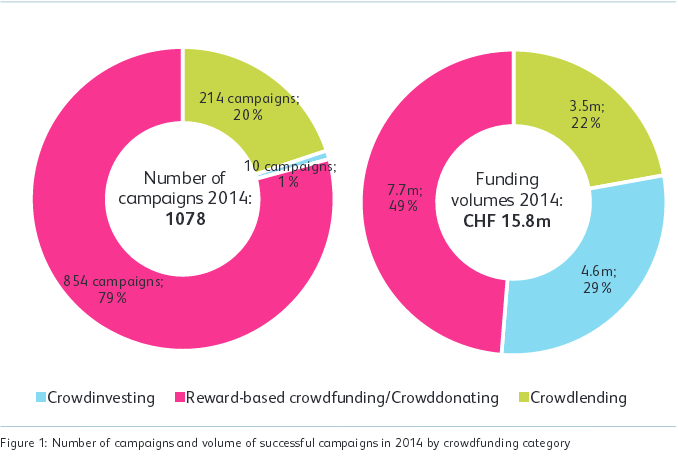

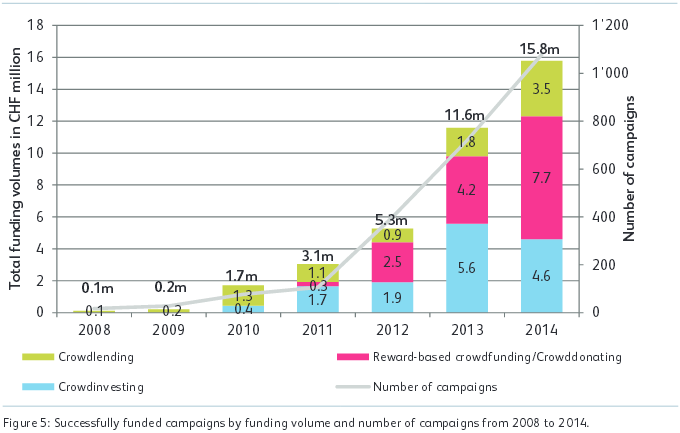

The Swiss market is growing fast; albeit on low absolute numbers compared to other European countries. The market is in a very early development stage. As the following chart shows the volume is mainly generated by crowdsupporting/crowddonating.

Source: Crowdfunding Monitoring Switzerland 2015 study

The total market for new loans to consumers in Switzerland in 2014 was 3.9 billion CHF. Via p2p lending 3.5 million CHF were originated in 2014, so that equals a market share of only 0.1%. But the p2p lending volume has nearly doubled compared to 2013 (1.8 million CHF). The authors state:

The crowdlending market has experienced the strongest year-on-year growth of all crowdfunding segments. … The number of campaigns rose from 116 to 214, and all of them were successfully funded. The current challenge of crowdlending platforms is not finding funders. On the contrary, it is (more) difficult to get borrowers on the platforms. Crowdlending campaign funders invested an average of CHF 1,100, which is substantially different from the figures in reward-based crowdfunding & crowddonating as well as in crowdinvesting. The average campaign amount was CHF 16,200, which was slightly higher than in the past year (CHF 15,000). The average loan amount in crowdlending is very similar to the average consumer loan as of the end of 2014. The crowdlending market is, however, still niche market.

Source: Crowdfunding Monitoring Switzerland 2015 study

Regulation limits that a private consumer loan cannot be financed by more than 20 different individual lenders.

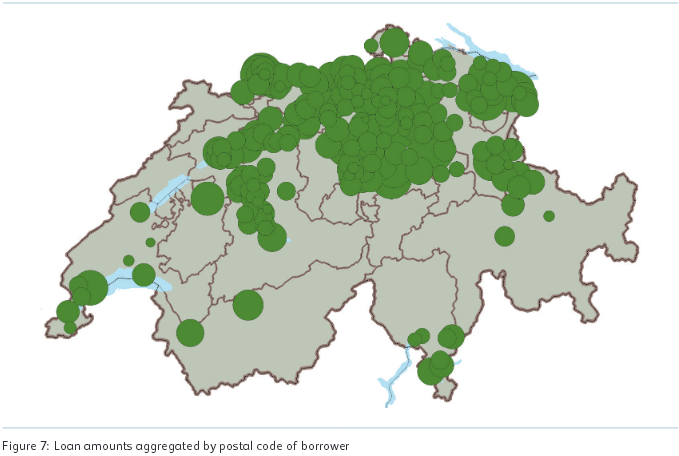

The authors analysed loan data of the Cashare marketplace. Examining who uses p2p lending as a borrower the study finds:

The average borrower age is 38. One fifth had at least one child under the age of 16 at the time the loan was raised. At 37 percent, married people were proportionally under-represented, although they make up 54 percent of the permanent resident population. 19 Homeowners (19 percent) and women (24 percent) are also under-represented. The distribution of nationalities is slightly more representative of the Swiss population. 71 percent of the borrowers were Swiss, while 29 percent of the borrowers were not in possession of a Swiss passport. The average proportion of the foreign-born resident population in Switzerland was 22 percent between 2008 and 2013. The age distribution of the borrowers leads to the conclusion that crowdlending is currently still primarily used by the tech-savvy Generation Y. 60 percent of all loans raised since 2008 went to people under the age of 40. Only 4 percent of the borrowers for successful projects were over 60 years of age.

Also the borrowers regional distribution shows that use is much more common in the German speaking areas of Switzerland.

Source: Crowdfunding Monitoring Switzerland 2015 study