As reported earlier today, new p2p marketplace Crosslend (Spanish site) (German site) offers unsecured p2p loans to consumers. There was a soft launch phase last week, which enabled me to register early and gain first insights into the marketplace interface. After registration I awaited verification of the newly opened lender account at biw Bank and then deposited money there (if you are outside the Eurozone, you may consider using Transferwise or Currencyfair instead of doing a direct transfer).

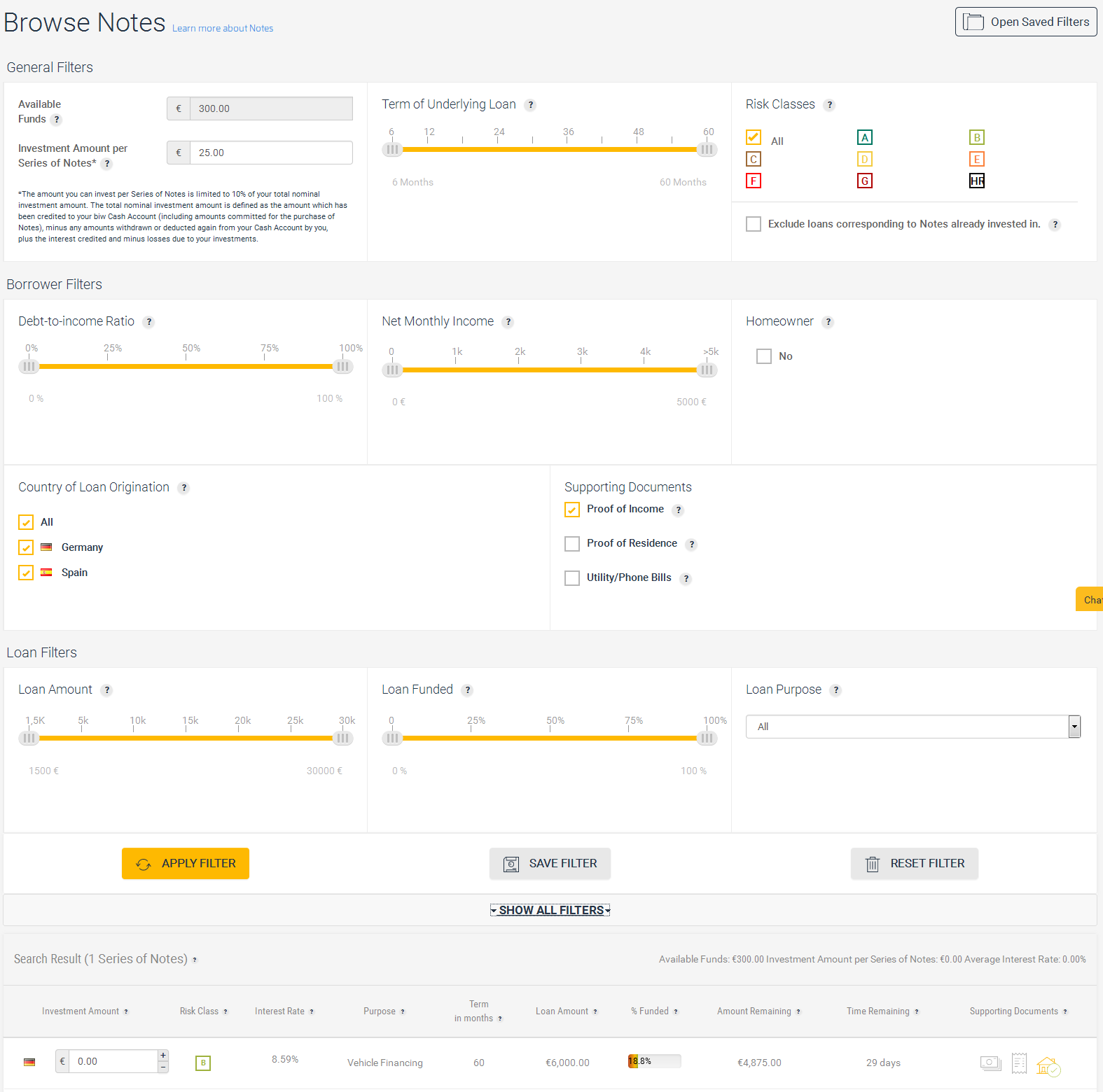

In the dashboard I selected ‘Browse Notes‘ which led me to an overview of all available note. Since my test was conducted during soft launch, there was only one available not.

Screenshot Browse Notes (click for larger view): at the bottom there is the listed loan (risk grade B) for 6,000 EUR vehicle financing at 8.59% interest

Crosslend Filters

Initially only the general filters (loan term, risk classes) for selecting loans are displayed. By clicking on ‘show all filters’ I expanded further loan selection filters: Borrower filters are DTI, monthly net income, home owner, country and supporting documents (proof of income, proof of residence and utility/phone bills). Loan filters include loan amount, funding percentage and loan purpose. It is possible to save filters to reapply them again in future. Continue reading →

Today, new p2p lending marketplace Crosslend launched offering unsecured loans to consumers. Opening to borrowers and investors in Germany and Spain as well as investors in the UK, Crosslend aims for further European expansion and creating a unified European marketplace.

The Berlin headquartered startup was founded by Oliver Schimek and Daniel Schlotter (both had previous FinTech experience at Kreditech) and Marie Louise Seelig (formerly Skrill). Crosslend already raised a funding round prelaunch from Lakestar, Atlantic Internet and others.

Markets targeted by Crosslend

When a loan is granted it is purchased and acquired by Luxembourg based Crosslend Securities SA and securitized by a series of ‘notes’. Notes are debt securities which can be purchased by investors. A series of notes is made up of a number of notes, each with a denomination of 25 EUR. The total nominal value of a series of notes is equivalent to the amount of the loan. When a borrower makes their loan repayments, CrossLend Securities SA makes the corresponding payments of interest and principal pro rata to the holders of the notes. This will enable Crosslend to offer a secondary market, which is due to be launched in a few months.

Borrowers can apply for loans from 1,500 to 30,000 Euro for loan terms from 6 to 60. Crosslend will grade loans in risk classes A to G, HR. Interest rates (APRs range from about 3.5% to about 17%) and borrower fees are dependent on the assigned risk classes. Crosslend checks submitted proofs of income for all loan applications.

To invest lenders first open an account with biw Bank, the partner bank of Crosslend, this involves a short video verification process of the investor’s identity (webcam required). Video verification is an innovative account opening process which several German online banks started to use to replace the identification via postal communication. Investors then deposit money into their account (250 Euro minimum). Then investors can choose which loans they want to invest into (25 EUR minimum bid per loan). Crosslend charges investors a 1% fee at origination.

UK investors should consider using Transferwise or Currencyfair to exchange money into Euro to avoid possible bank fees and a bad exchange rate applied by the bank. Continue reading →

German p2p lending service Lendico announced yesterday that an unnamed international hedge fund and 2 german banks will invest over 100 million Euro in loans on the Lendico marketplaces. The management sees that as a mark of confidence. Lendico is committed to increase activities in its growing core markets and plans to expand the product into SME loans. Continue reading →

Today p2p lending service Lendico made the first loans from Spanish borrowers available to German investors on the German marketplace. German lenders can now bid on these loans provided they fulfill a few prerequisites. To prepare for this, Lendico had in the past weeks informed interested investors of the necessary steps to enable bidding on these cross-border loans on the German marketplace:

Lenders need to upgrade to a (free) premium account, if they don’t already have one.

Lenders need to send a form via postal mail to the tax authorities that certifies the status of residency. Lendico advices that it will usually take the tax authorities 5-21 days to process this confirmation.

The returned postal form can then be submitted via post, fax or email (scan) to Lendico.

The origin of the listed loans is now marked by a flag symbol on the German marketplace (see below).

Excerpt of a screenshot of Lendico.de showing listed German and Spanish p2p loans

This does not work (yet?) for loans from the other Lendico markets.

LoanBook Capital is a Spanish peer-to-business (P2B) finance platform, providing an alternative to traditional savings and fixed income products to investors of all types via direct participation in loans, and other forms of credit finance, to mature, good quality Spanish SMEs.

LoanBook provides credit origination and management services to clients. These services are supported by an online platform, which gives investors access to credit opportunities through an auction marketplace, as well as a soon to be launched secondary market for trading loan participations.

What are the three main advantages for investors?

As with other P2B platforms, the main attractions for investors of this model are typically greater risk adjusted returns, control and transparency over investments and lower fees. LoanBook is no different in these characteristics: we provide access to an asset class that offers a return that exceeds that available from traditional fixed income investments with comparable characteristics (e.g. risk and liquidity), we allow investors to manage the risk and return profile of their portfolio online in a transparent way, and we do not charge fees to investors, other than for providing liquidity through our secondary market.

As with advantages to investors, LoanBook offers the borrower the typical advantages that you would expect from a P2B platform; competitive and transparent cost of capital (interest rates & fees), access to an alternative channel of finance and a quick and easy application process.

How did you start Loanbook Capital? Is the company funded with venture capital?

LoanBook was started at the end of 2012 by two founding partners with their own capital and initiative. The company’s shareholder base has moved on somewhat since then, with each of the three-man management team, and a number of the employees, having an ownership stake in the company. Continue reading →

Even though February was a short month, several p2p lending services topped their January loan volume. Even more impressive is the continued year on year growth. 3 more services were added to the table. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in February 2014. Source: own research Note that volumes have been converted from local currency to US$ for the sake of comparison. Some figures are estimates/approximations.

Notice to p2p lending services not listed: If you want to be included in this chart in future, please email the following figures on the first working day of a month: total loan volume originated since inception, loan volume originated in previous month, number of loans originated in previous month, average nominal interest rate of loans originated in previous month.