The table lists the loan originations of p2p lending marketplaces in May. Funding Circle leads ahead of Zopa and Ratesetter. The total volume for the reported marketplaces adds up to 500 million Euro. This is over 10% higher than the previous month and that despite the adverse effect of the pound taking a dive. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms. This month I added Paskoluklubas.

Milestones reached this month are:

Assetz Capital crosses 250 million GBP lent sinch launch

Lendinvest reaches 1 billion GBP in origination since launch

Table: P2P Lending Volumes in May 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

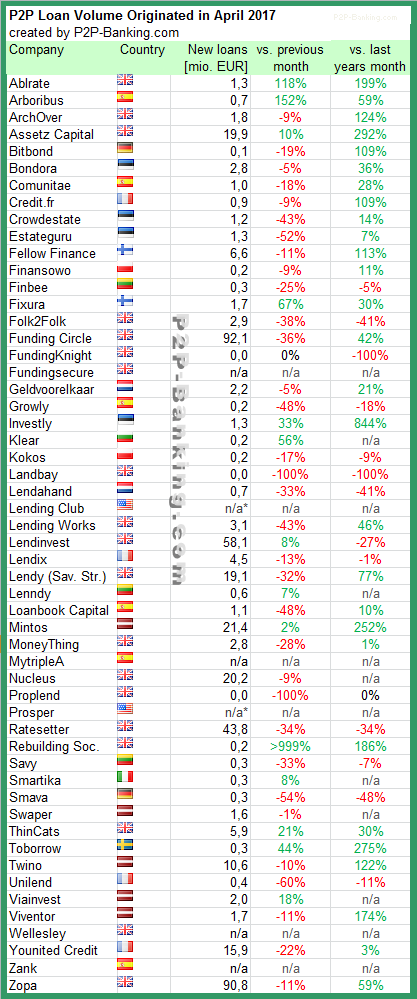

The table lists the loan originations of p2p lending platforms in April. Funding Circle leads ahead of Zopa and Lendinvest. The total volume for the reported marketplaces adds up to 445 million Euro. I track the development of p2p lending volumes for many countries. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms. This month I added Nucleus.

Milestones reached this month are:

Younited Credit crossed 500 million Euro loan volume since launch

Table: P2P Lending Volumes in April 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

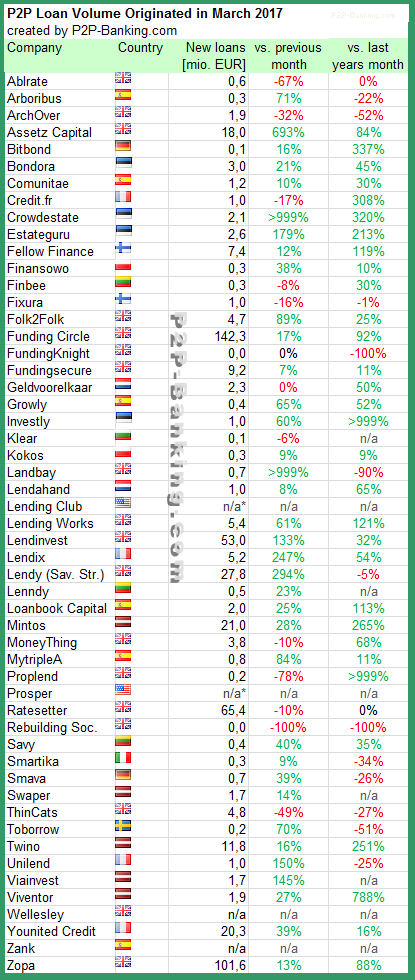

The table lists the loan originations of p2p lending marketplaces in March. Volumes picked up considerably compared to February. Funding Circle continues to lead ahead of Zopa and Ratesetter. The total volume for the reported marketplaces adds up to 532 million Euro. I track the development of p2p lending volumes for many countries. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms. This month I added Lenndy and Credit.fr.

Milestones reached this month are:

Mintos crossed 150 million EUR in originations since launch

Table: P2P Lending Volumes in March 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

The European online alternative finance market, including crowdfunding and peer-to-peer lending, grew by 92 per cent in 2015 to €5.431 billion, according to the results of the 2nd Annual European Alternative Finance Industry Survey conducted by the Cambridge Centre for Alternative Finance at University of Cambridge Judge Business School, in partnership with KPMG and supported by CME Group Foundation.

The report released today, titled “Sustaining Momentumâ€, had the support of 17 major European industry associations and research partners, and was based on data from 367 crowdfunding, peer-to-peer lending and other alternative finance intermediaries from 32 European countries – capturing an estimated 90 per cent of the visible market. P2P-Banking.com is one of the research partners.

The United Kingdom was by far the largest in Europe at €4.4 billion, followed by France at €319 million, Germany at €249 million and the Netherlands, €111 million. Other large European markets include Finland with €64 million, Spain at €50 million, Belgium at €37 million and Italy at €32 million. The Nordic countries collectively accounted for €104 million, while Central and Eastern European countries registered a total of €89 million.

Excluding the UK, the European alternative finance market grew by 72 per cent from €594 million in 2014 to €1.019 billion in 2015.

“Although the absolute year-on-year growth rate slowed by 10 per cent†(from the 82 per cent growth excluding the UK between 2013 and 2014) the industry is still sustaining momentum with substantive expansion in transaction volumes recorded across almost all online alternative finance models,†the report said.

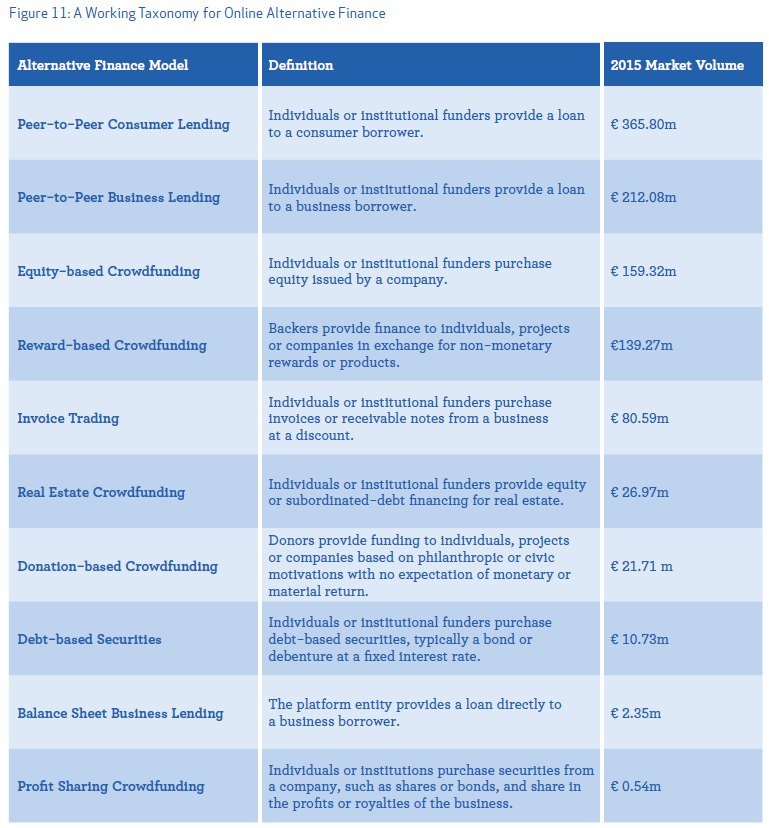

Peer-to-peer consumer lending is the largest market segment of alternative finance, with €366 million in Europe in 2015. Peer-to-peer business lending is the second largest segment with €212 million, with equity-based crowdfunding in third with €159 million and reward-based crowdfunding fourth at €139 million.

Table: Figure 11, page 31 of ‘Sustaining Momentum’, volumes by market segment in Europe 2015 (outside UK)

Among other findings:

Estonia ranked first in Europe in alternative finance volume per capita at €24, followed by Finland at €12 and Monaco at €10 outside of the UK.

Online alternative business funding increased by 167 per cent year-on-year to €536 million raised for over 9,400 start-ups and SMEs across Europe.

Institutionalisation took off in mainland Europe in 2015, with 26 per cent of peer-to-peer consumer lending and 24 per cent of peer-to-peer business lending funded by institutions such as pension funds, mutual funds, asset management firms and banks.

Across Europe, perceptions of existing national regulations in alternative finance are divided. About 38 per cent of surveyed platforms felt their national regulations for crowdfunding and peer-to-peer lending were adequate and appropriate, 28 per cent perceived their national regulations to be excessive, and a further 10 per cent said current regulations were too relaxed.

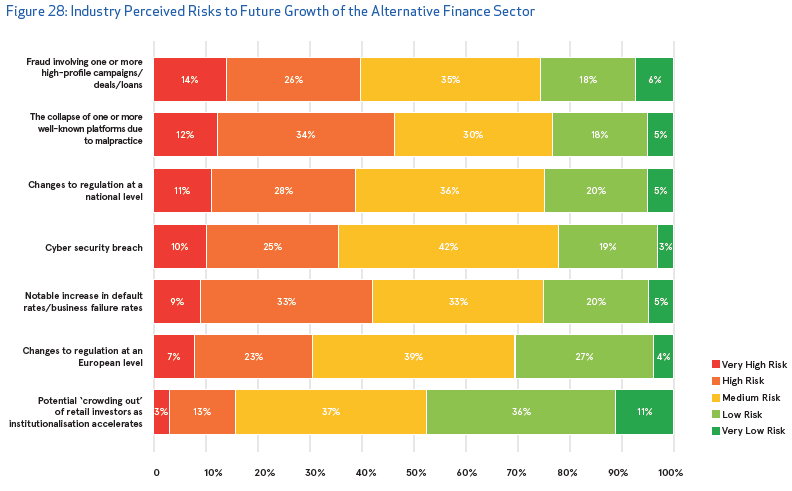

The biggest risks perceived by the alternative finance industry are increasing loan defaults or business failure rates, fraudulent activities or the collapse of platforms due to malpractice.

Chart: Figure 28, page 47 of ‘Sustaining Momentum’, risks to the industry as perceived by the polled platforms

Robert Wardrop, Executive Director of the Cambridge Centre for Alternative Finance, said: “European alternative finance transaction volume increased to more than €5 billion in 2015, with volume outside of the UK market exceeding €1 billion for the first time. The European alternative finance industry is still small, however, and the slowing rate of growth during the year is a reminder of the risks the industry must contend with in order to transition from a start-up to a sustainable funding channel within the European financial services ecosystem.â€

Irene Pitter, Global Executive, Banking & Capital Markets and member of the FinTech Leadership Team at KPMG, said: “This report shows that the alternative finance sector is set to continue to grow and mature. 2016 marks a significant year for ‘alternative finance’ in Europe as the market demonstrates clear signs of continued strong growth and increased maturation in the sector as a whole. European activity, excluding the UK, showed solid growth of 72 percent last year and demonstrated client demand for alternative finance solutions even in the smaller EU countries.â€

Rumi Morales, Executive Director, CME Ventures, said: “The prominent feature of financial technology is that it is truly borderless. No one country is harnessing alternative financial markets or business models to the exclusion of any other. Rather, from the UK to Estonia and from Finland to Monaco, the entire European continent is experimenting and expanding upon innovations that can provide greater access to capital and financial services to more people than ever before.â€

The Spanish Securities Exchange Commission (CNMV, Spain’s financial regulator) has authorized MytripleA as a Platform for Participatory Financing, the formal name for a p2p lending platform. This is one of the first actions to implement Law 5/2015 Promotion of Corporate Financing. MytripleA already benefits from a Payment Institution license (which can be passported within the EU) granted by the Bank of Spain, which authorizes MytripleA to make loan disbursements and receive loan instalments within the regulatory environment for banking payments. This is an additional regulatory requirement in Spain, which is not required by other European countries.

With this new authorization, MyTripleA becomes the first crowdlending platform to have both of the required authorizations in Spain. Competitors entering Spain, will not be able to use the the so-called passporting provisions from a financial regulator outside of Spain and will need to apply for a Platform for Participatory Financing license before being able to operate in compliance with Spanish regulations Law 5/2015 Promotion of Corporate Finance provided a unified legal framework for crowdlending platforms and securitized funds, and made CNMV responsible for their creation, authorization and supervision. Crowdlending has experienced rapid growth across Europe. The Spanish market last year grew 266% according to the website P2P-Banking.com. Within the new regulatory framework and with the supervision of CNMV, a greater degree of awareness of the alternative financial services market is expected.

French Lendix announced that it received its formal CNMV accreditation to operate as a P2P lending platform in Spain. The Spanish entity will be the first Lendix international market to open. It will target financing of credits to SME, for amounts ranging from 30,000 to 2,000,000 Euro, duration of 18 to 60 months and at interestrates comprises between 5.5% et 12%. Companies presented on the platform will be selected and analyzed by Lendix credit analysis team and will need to generate a turnover of at least €400’000. Non accredited private investors* will be able to lend up to 3,000 Euro per project with a total maximum yearly amount of 10,000 Euro, while no limit will apply to accredited private investors nor institutional investors. The launch of Lendix’s spanish platform is scheduled for Q4 2016.

Equity crowdfunding platform Crowdcube also received authorization.

Spanish p2p lending marketplace Arboribus completed a study among 1,500 investors on its platform. Arboribus facilitates loans to SMEs in Spain.

Some of the main findings:

50% of the participants in the survey reinvest their profits

43% intend to increase their investment

30% of investors see the opportunity to assist SMEs to get the funding to go ahead with their projects

29% like that it is an alternative to invest independent from banking. The transparency of the p2p lending and control over where the money of this new model is invested directly collides with the opacity of the banks and the distrust in the management of their savings

in 60% of cases the investor selects the company depending on the sector to which belongs

only 12% analyze the balance sheet and income statement before investing

27% connect via mobile phones, smartphones and tablets