The following table lists the loan originations of p2p lending marketplaces in May. Funding Circle leads ahead of Zopa and Ratesetter. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Table: P2P Lending Volumes in May 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

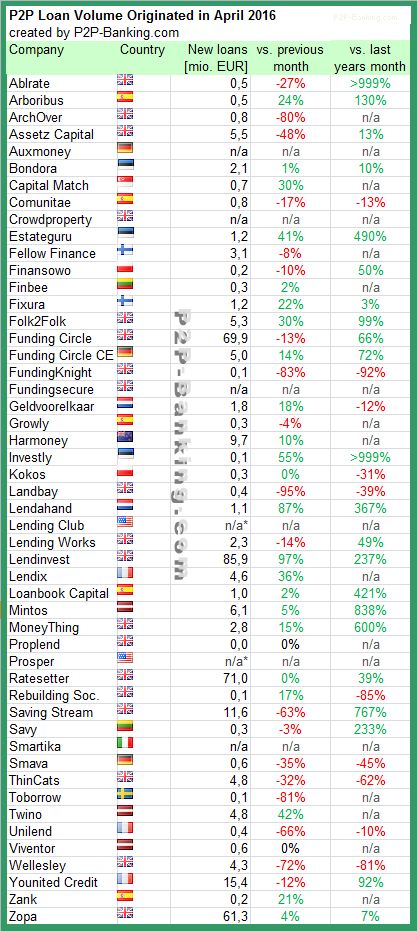

The following table lists the loan originations of p2p lending marketplaces in April. Lendinvest leads ahead of Ratesetter and Funding Circle UK. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Last month Younited Credit (formerly Prêt d’Union) originated first loans in Italy. Geoffroy Guigou told P2P-Banking.com, Younited Credit had a great start, with 416,500 Euro loans originated.

Table: P2P Lending Volumes in April 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

In Germany Kapilendo and Venturate announced they will merge. Kapilendo is a p2p lending marketplace offering loans between 30,000 and 2.5M Euro to SMEs for loan terms of 1 to 5 years. The minimum amount for investors is 100 Euro. Investors are not charged any fees. Kapilendo was launched in 2015 and recently gained some publicity, when it succeeded to fund a 1M Euro, 3 year loan to first division soccer club Hertha BSC in 10 minutes. This loan has an interest rate of 4.5%. So far loans listed at Kapilendo were in the range of 3.1% to 6.5% interest. Kapilendo uses Fidor as transaction bank to originate loans.

Venturate is a small equity-based crowdfunding site, launched in summer 2015.

FinLab, owner of Venturate will also invest an additional amount to foster further growth of Kapilendo. After the transaction FinLab now owns 25.1% of Kapilendo.

Informed sources told P2P-Banking.com that German Commerzbank plans to launch an own p2p lending marketplace called ‘Main Funders’ in the first half of 2016. The marketplace aims to connect SMEs seeking funding with investors. The name ‘Main Funders’ is a wordplay as ‘Main’ is the name of the river passing through Frankfurt, where the bank has its headquarter. The service is developed together with Main Incubator, the fintech incubator of Commerzbank. Currently all relevant domain names for Main Funders just redirect to the frontpage of Main Incubator. Commerzbank registered a trademark for ‘Main Funders’ in January 2016.

It remains to be seen whether this will be a full fledged marketplace, that also handles all transactions, or more a business initiation facilitator. A short mention in the 2015 annual report of Commerzbank uses the term ‘peer-to-peer-lending-plattform’ to describe Main Funders.

Under German regulation only banks can fund loans. To comply with this all existing p2p lending companies in Germany partner with a transaction bank which originates the loan and then sells the proceeds (repayments and interest) to the investors. So far a handful of small specialised banks were involved in these transaction. Commerzbank would be the first large German bank to enter the space and also the first bank to build an own platform.

Giromatch promises its customers “Better Banking Together”. We are a Direct Lending platform and offer our prime retail borrowers a complete digitized loan process at top rates. For investors we offer in this low yield environment a complete new asset class, namely the Deutschlandportfolio. What previously has only been accessible by banks, is now available to everyone – investing into a diversified prime loan portfolio and achieving an attractive return while keeping risks at a manageable level.

What are the three main advantages for investors?

The first great advantage for investors is that they get access to this new asset class at no costs. Secondly, the investment into the Deutschlandportfolio is automatically diversified. This is being achieved by a matching algorithm that optimizes each investment. The third advantage is the security-pool. Giromatch deposits a certain amount of each earned euro into the security pool in order to build up a security cushion for investors.

What are the three main advantages for borrowers?

The advantages for our borrowers result from the digitized loan application process. The loan application can be finished online in less than 10 minutes, no matter if you access Giromatch from home or mobile. A second advantage is the instant loan term confirmation without registration. After one enters all credit relevant facts, we show a customized rate, which we try to stick to as long as the input data was correct. A registration is not necessary in order to get a customized quote. A third advantage is our technology driven approach during the data verification process. A borrower does not need to send us documents proving the credit history. All we need from the borrower is a temporarily login into his/her current account, such that we can instantly confirm the credibility. Nevertheless, we think the most important advantage are the low rates we offer, which is only possible due to our digitized and cost-saving structure.

What ROI can investors expect?

The ROI depends on the portfolio the investor chooses. We provide two different maturities. The shorter-term Deutschlandportfolio runs for three years and has an estimated gross return of 3.60 % p.a. Investors who choose the portfolio with the investment period of five years can expect a gross return of 4.00 % p.a. Due to our strong credit checks we anticipate no more than approximately 1% losses p.a. post recovery due to expected defaults.

How is your company funded?

We were able to inspire several business angels from the financial industry for our seed funding round. Hence, we were able to not only fund the company but also to win many important contacts in the financial industry. Prior to the seed round we invested our own money and money from friends and family. And we were granted an EXIST scholarship by the Bundesministerium für Wirtschaft und Energie (BMWi).Continue reading →

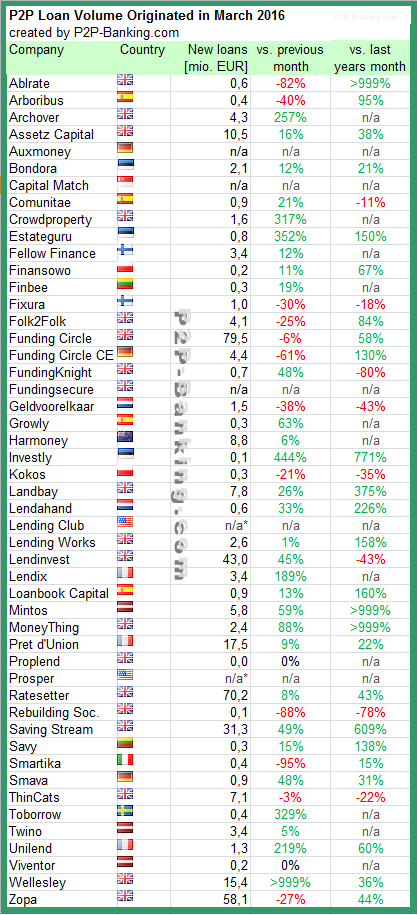

The following table lists the loan originations of p2p lending marketplaces in March. Funding Circle leads ahead of Ratesetter and Zopa. I added MoneyThing to the list. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Table: P2P Lending Volumes in March 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.