The table lists the loan originations of p2p lending marketplaces for last month. Funding Circle leads ahead of Zopa and Ratesetter. The total volume for the reported platforms adds up to 391 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Milestones reached this month are:

Bondora reaches 100 million Euro in financed loans since launch

Want to meet representatives of many of the listed companies? Attend Lendit London in October -use discount code WiseclerkVip to get a 15% rebate on registration.

Table: P2P Lending Volumes in August 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

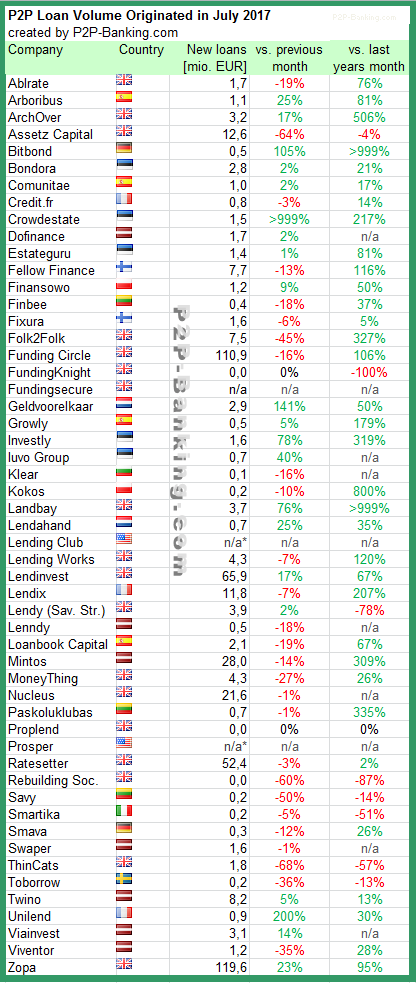

The table lists the loan originations of p2p lending marketplaces in June. Zopa leads ahead of Funding Circle and Lendinvest. The total volume for the reported platforms adds up to 491 million Euro. I added Iuvo Group and Dofinance to the table. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Milestones reached this month are:

Zopa crosses 2.5 billion GBP originated since launch

Ratesetter crosses 2 billion GBP originated since launch

Mintos loan volume since launch now over 250 million Euro

Lendix reaches 100 million Euro in financed loans since launch

Table: P2P Lending Volumes in July 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Finnest.com is the only platform successfully providing modern corporate finance for well-established Mittelstand companies (no start-ups). Borrowers are mostly AAA-like rated brands and industry leaders that have been on the market for years (often decades) and are able to demonstrate a sustainable and profitable growth path.

These top-companies are actively seeking alternatives to their traditional bank loans and want to diversify their finance mix. For the first time, Finnest.com gives these Mittelstand champions access to the capital market. The platform is a 21century version of a classic corporate bond bookbuilding process and provides end-to-end financing solutions.

Currently, Finnest.com is licensed and active in Germany, Austria, Switzerland and Slovakia.

What are the three main advantages for investors?

1.) Investors get access to a completely new class of investments, previously reserved for a handful of professional investors. 2.) On Finnest.com, investors select the interest rate of their choice! Only if the company agrees to pay this annual rate (or more), will a deal be closed. 3.) Investors can invest in local and regional companies that create jobs and income in their area.

What are the three main advantages for borrowers?

1.) For the first time, Finnest.com provides this segment of well-to-do Mittelstand borrowers with access to the capital market previously reserved for large corporations. 2.) Mezzanine financing as provided via Finnest.com strengthens these companies’ balance sheets. 3.) An enormous PR & loyalty effect – when customers invest into “their†brand, the term “brand messenger†gets a rich new meaning.

What ROI can investors expect?

On Finnest.com, investors select their interest rate of choice. On average, companies have paid out 5.5% annually fixed interest rates. The concept works: a Finnest investor invests about 7.000 Euro per transaction, that is roughly 20 times higher than on other online platforms.

Finnest charges investors a fee of 1% (minimum 25 Euro). Doesn’t a high fee hinder diversification?

We are one of the few (the only?) platform that charges an investor fee. It’s 1% of the invested amount. That means if an investor invests 7.000 Euros, she/he is charged 70 Euros once. That’s it. We haven’t learned of any investor who would not invest because of this small fee.

Finnest.com uses subordinated loans (‘qualifiziertes Nachrangdarlehen’). An Austrian court recently ruled that this structure severely disadvantages investors. Why did you choose this structure rather than standard loans?

Headquartered in Austria, Finnest.com is licensed by the Austrian AlternativfinanzierungsGesetz (alternative financing law). This law (just like its German counterpart, the Schwarmfinanzierungsprivileg) actually requires us to use subordinated loans. It’s the tool the law selected. The court ruling you refer to, addressed one specific contract by one single issuer who did not use any legally checked platform, but decided to do this financing on his own. Apparently, that was not such a smart idea – that contract must have been quite bad and the court ruled accordingly. Our contracts are thoroughly checked by leading law firms in each jurisdiction and have been presented to the financial authorities, of course.

How did you start Finnest.com?

For many years, Günther Lindenlaub, my co-founder, had been in charge of capital market transactions for one of Europe’s leading banks. While he saw, that large corporates keep using tools like corporate bonds to diversify their finance mix, the banks we not able (or willing) to offer something similar to the Mittelstand. But bonds are too complex and costly for the Manners and Almdudlers of this world. So, he decided to create his own platform – Finnest.com.

Is the technical platform self-developed?

Yes. It was built by a team that had previously built part of ING-Diba and AustroControl, the Austrian flight control agency. These guys know everything about stability, security and usability. We like to joke that we did not build a Tesla but one of those 80s’ Volvos with the iron bars in the doors. Very safe, very stable, drives, and drives, and drives.

Was the company funded with venture capital? Is the company profitable now?

We were lucky to attract Speedinvest, the largest Austrian VC, as our seed investor. And we have added a carefully selected group of international angels and VCs since. As we are still growing fast, we are not profitable, yet. But we are doing very good business.

Are there any new features for the platform your team is working on? What about a secondary market?

We are expanding: As we are speaking, our team is in the last phases of building a new, second platform. It will provide a similar service as Finnest.com does, but it will address a different market segment: large corporations on the one hand and professional as well as institutional investors on the other hand. Modern corporate finance XL, so to say.

Which country are you most successfully attracting investors in?

Even though we originate in Austria, Germany is our prime market. Already today, the majority of our investors comes from Germany and we have just hired new team members focusing mainly on the German market.

You plan an expansion beyond Germany, Austria and Switzerland. What can you tell us about your next market(s)?

Our industry is a highly regulated one, governed by national rules and regulations. But with the new platform, we will be able to provide a pan-European service. That will open a completely new scale of opportunities for us.

Do you plan to cooperate with institutional investors? In which way?

Yes, definitely. The new platform will be customized for their interests and needs.

What is the current state of the market in Austria?

With the passing of the AlternativfinanzierungsGesetz, (alternative financing law), the online financing market grew at a rapid pace. We have now more than a dozen platforms and high 2-digit number growth rates. But of course, business in Austria is always only a fraction of that in Germany. Germany is the main market we are focusing on.

Where do you see Finnest in 3 years?

We believe, that in 2020 there will be three main platforms financing larger, successful companies across Europe. Finnest.com should be one of them.

The German market is a tough market for p2p lending services to succeed. Few companies run a p2p lending marketplace model. One of the earliest players, Smava pivoted already in 2012 and now brokers bank loans.

After months and years of announcements and waiting Funding Circle Germany yesterday published loan book performance figures. Data reported is on all loans since launch on March 30th, 2014 (at that time Zencap) and as of June 30th, 2017. In total there were 920 loans.

Figures:

Total loan origination volume 66,560,800 EURÂ 100% Repaid loan volume 26,859,284 EUR 40.35% Loan volume in default (more than 90 days overdue): 3,988,632 EUR 5.99% Outstanding principal: 35,712,885 EUR 53.65% Total interest paid to investors: 4,578,552 EUR

The outstanding principal of 35,712,885 EUR (100%) is further categorized: Current: 33,293,583 EUR 93.23% Loans that are less than 30 days overdue: 1,664,005 EUR 4,66% Loans that are 30 to 60 days overdue: 421,902 EUR 1.18% Loans that are 60 to 90 days overdue: 333,394 EUR 0.93%

Average weighted interest rate: 8.41%

I would have linked to the source here, but Funding Circle pulled the figures within hours after publication and the page now returns a 404 error (I did save a screen shot before they were pulled). I reached out via email to Funding Circle asking for the reasons, but have not received a reply up to the point of publication of this article. Update: I received a reply from Funding Circle stating that the figures were not correct and did not match Funding Circle’s global reporting format. An example given was that payments made by defaulted loans were omitted. Funding Circle strives to publish the corrected figures asap. 2nd update July 13th: Funding Circle has now published updated figures in changes format. They are online here.

Phrasing it differently one could say that 9.6% (6,4M/66,6) of all issued loans are currently overdue or in default.

In my view the figures give a very bleak – but correct picture of the state of Funding Circle Germany’s loan book. Overdue and default figures are high. With nearly 6% of the loan amount in default and more than another 6% of the remaining loans overdue, there is a very high probability that many investors will incur (after tax) losses. Usually German investors cannot offset default losses against interest earned.

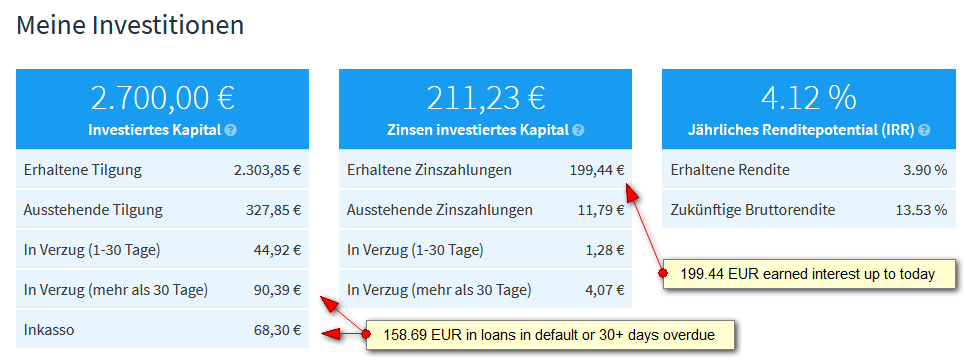

My portfolio

I invested into 27 loans with 100 EUR each (the minimum bid). I stopped investing already in February 2015, after only 10 month, when it became clear to me that Funding Circle Germany had higher overdue figures than expected. However as there is no secondary market at Funding Circle Germany I was stuck with the loans until maturity.

Of my 27 loans the status today is: – 22 repaid – 4 overdue (2 of them for 256 days !) – 1 default (in collection)

I already received back 2,303 EUR of the principal, so there is only about 15% of my investment amount still outstanding. I might get away with a return around zero, as my defaults + overdues are still lower than the interest paid, but it will be close as I have to pay taxes on the full interest earned regardless of defaults. My dashboard still claims 4.12% yield for my portfolio, which does not reflect reality as I see it. The only chance for that to happen would be full recovery of defaults and overdues, which is an unlikely scenario.

My own portfolio at Funding Circle Germany

Investor sentiment towards Funding Circle Germany seems to have turned mostly negative to sarcastic in the past two years if you look at the massive critic on the Funding Circle forum at P2P-Kredite.com. Funding Circle Germany no longer publishes statistics regularly on new monthly loan volumes.

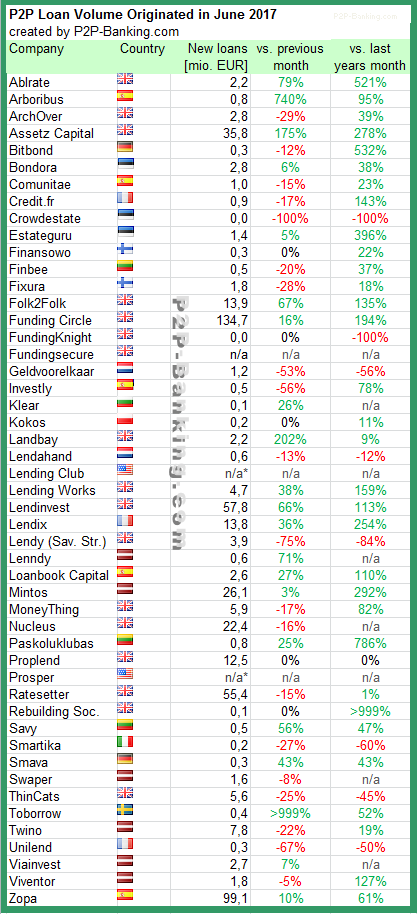

The table lists the loan originations of p2p lending marketplaces in June. Funding Circle leads ahead of Zopa and Lendinvest. Assetz Capital makes a huge leap forward. The total volume for the reported platforms adds up to 530 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Milestones reached this month are:

Twino reaches 150 million EUR in origination since launch

Table: P2P Lending Volumes in June 2017. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.